Been managing my mother’s IRA account for the past year. For the low risk portion of her fund I’ve had it split between 2 bond funds VCLT and BND. This has been a losing play over the past year as bond funds got punished with rate hikes by the Fed. Plus these funds seem to be quite correlated with the overall stock market these days, so I’m not sure if they offer any meaningful diversification. It is truly a one asset (Fed money printing) world. With more rate hikes likely incoming, it seems this will continue to be a losing play.

I’m looking at this allocation and wishing it had just been in a 2% checking fund over the past year! (Not sure how to do this in a IRA though …) What are some options out there I could consider that would offer a steady return + uncorrelated with stock market? I’m using Fidelity and Merrill for this portfolio currently.

I’m sure there will be better suggestions, but if bonds and stocks are out, why not just get CDs? Both of the houses you mentioned sell them. They may not be available in her 401k, but you can probably convert the non-current 401k into an IRA, where you can certainly buy CDs.

Disclaimer: I’m not a lawyer, baker, accountant or candlestick maker, so please consult them before following any of my advice.

The Fed hikes are mostly over for the near term. If you want something low risk, just buy BND or whatever. Everything was a losing investment last year except cash, pretty much. That hopefully won’t happen too frequently.

Not so convinced of this. They might take a break for a bit but otherwise barring a crash imo they’re pretty much locked in to keep hiking until there is a crash. (That’s just how the Fed operates.) Locking in a 9-12 mo CD at 2.45% is looking mighty attractive.

Didn’t know I could buy CDs in an IRA - now I do! Any other ideas?

You can buy CDs in an IRA, but usually you have to open the account at a bank rather than a broker. The brokerage CDs options are often either not available or quite mediocre. 401ks often do not have this option at all, although I see you updated your OP that this is an IRA, so it may be possible for you if you want to move it to a good bank or CU that offers competitive CD rates.

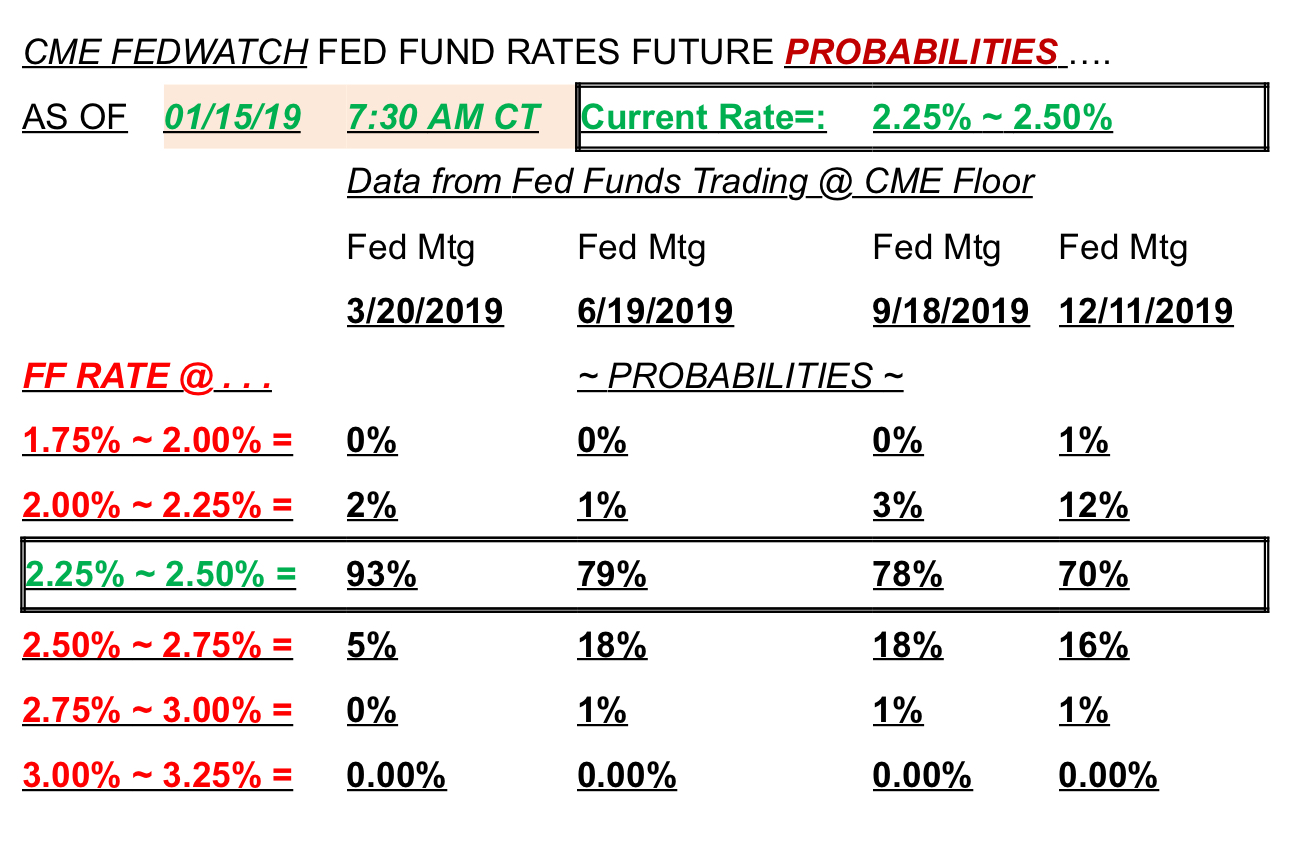

As for the Fed, I invite you to check out the Fed funds futures markets where people bet real money on these upcoming events. I will note that your view, several more hikes for 2019, was common and predicted by the futures markets until the big downturn at the end of last year and then it switched to the one hike in Dec and quite possibly nothing for this year or maybe one at most.

Fidelity & E*trade both have CDs in their IRAs. They sell 'brokerage CD’s or CDs on the ‘secondary market’ Rates seem ok starting in the 2% range for short term. I used to have a Scottrade account and their CD offerings were never impressive.

If you just want CDs you can also setup an IRA direct with a typical bank and just buy CDs in it. That would keep it simple but limit your options.

Well, these kind of “prediction markets” can move rapidly. Either way, any other ideas of something that would offer consistent income and be a good hedge against future rate hikes by the fed?

I caution you though, just because you took a hit once because of a bad market doesn’t mean markets are only out to hurt you. Looking at longer time horizon will eliminate a lot of the risk that you perceive from looking at returns over a short time span.

Also, I still suggest laddering Treasuries as you can have it so you are always buying new bills every week to make sure you are getting the current rates.

Sure, but that doesn’t mean they’ll move against you. Bonds will benefit in a recession especially if they start cutting rates again. And I do think they’re the best current prediction for the future, and presumably you don’t know better or you’d be asking about tips on 20x leverage for treasury futures rather than bonds vs cash. I am not worried about rates rising much, but you can if you’d like.

I’m not sure you really know what you want for an investment, honestly, so it’s hard to make suggestions. I would just buy something safe like cash/money market, CDs, or bond funds. If you can’t make up your mind, buy some of each -they’re not that different.

This statement struck a chord with me. My mom often asked me for advice on where she should invest. I’d often reply with a question: “What do you want to do with this money?” – meaning, how long do you want it invested? Can you tolerate a 10% drop between now and then? 20%? 30%?

She’d often reply that she was old and couldn’t afford to lose anything. (Yes, she said this for 30+ years of retirement!).

She wanted something safe, something that would get some decent amount of return and, down in her heart of hearts, she wanted something SEXY! She wanted to be able to chat over the coffee table about how she invested in X. In those 30 years, I made one solid suggestion that hit home: Buy windmills. (Vestas). Mom had a high-old time talking about how she was going to make it rich while saving the world.

That made it all worthwhile for the rest of the thirty years when I’d ask if the money was for her (CDs, money market) or her kids / grand-kids (S&P 500 index fund). She’d get mad and go back to her broker and pay a 5%+ fee for the “Next big thing” mutual fund. Oh well, brokers gotta pay rent too…

Dad got me interested in money, Jack Bogle and Lou Roukeyser kept me interested… it was Mom that got me started in FWF-type shenanigans WAAAAY before FWF existed. She helped me out with a CD play in the early '80s high interest era that paid a substantial part of my college education. Here’s to you, Mom. Rest in peace.

Motu – Think about the Chipotle Burrito factor – how large is the IRA? Is the difference between the various suggestions above on a par with the price of a delicious Chipotle burrito? (relatively speaking). If so, then take the easy path. It’s not worth extra effort. If you are talking big money, then some small differences in interest rate / return can add up and it is worth the extra effort.

It is one thing to pay a high fee for a fund but I fear the OP isn’t understanding time horizons and risk tolerance. This can lead to saying that you want zero risk when the market is low and then changing your mind when the market is high and going in at that point. This is otherwise known as selling low and buying high which I don’t recommend even more than paying a 5% fee (sometimes it might be worth it, I don’t know).

Overall I think FWF and even more so, FDF (if I can be so bold, I don’t think I’ve seen us refer to ourselves as such) is a finance deal site and feel like the OP may be better served on https://www.bogleheads.org even though I feel like FDF (and I) would benefit from having more participants here. But it sounds like your mom is closer to the audience for FDF than the OP from the exchange so far. I am sorry she isn’t around to post.

I don’t want to discourage the OP but I think there is more to the question as given so I don’t feel I can help here.

Bond funds could lose money when fed keeps increasing interest rate. That being said … fed is slowing down int rate hikes, so this year you may be just fine with bond funds.

The problem for you is that VCLT is long term bond, and it is corp bond. Bit on the risker side of the bond, when interest rate is going up. You need to switch to short or medium term bond funds to make them less risky.

Look at the “short duration” section on Fidelity … something like Flidelity Floating Point - which is a short term fund, and you make if interest keeps going up, they do fine - as the loans are short term, and they get turned back and they reinvest in higher rate loans. Last year, this was flat (like .07% return) … but did not lose any money.