I recently got my wife a Platinum VISA at NFCU that had a 0% for 12 months offer (new accounts only). Stuck that in a 2% CD and will just pay it all back once the 0% is up in a year.

Also, PSECU offers a perpetual $0/2.9% BT on their VISA. I’ve used it many times as a bridge loan, of sorts. That’s how I just did the NFCU CD/BT deal. I “BTed” $20k from PSECU to my NFCU checking account (which has a LOC tied to it with the same account number, in case PSECU starts asking), then I BTed from the new NFCU Platinum to my PSECU account. I think I paid something like $10 in interest for the interim few days that the NFCU money was moving.

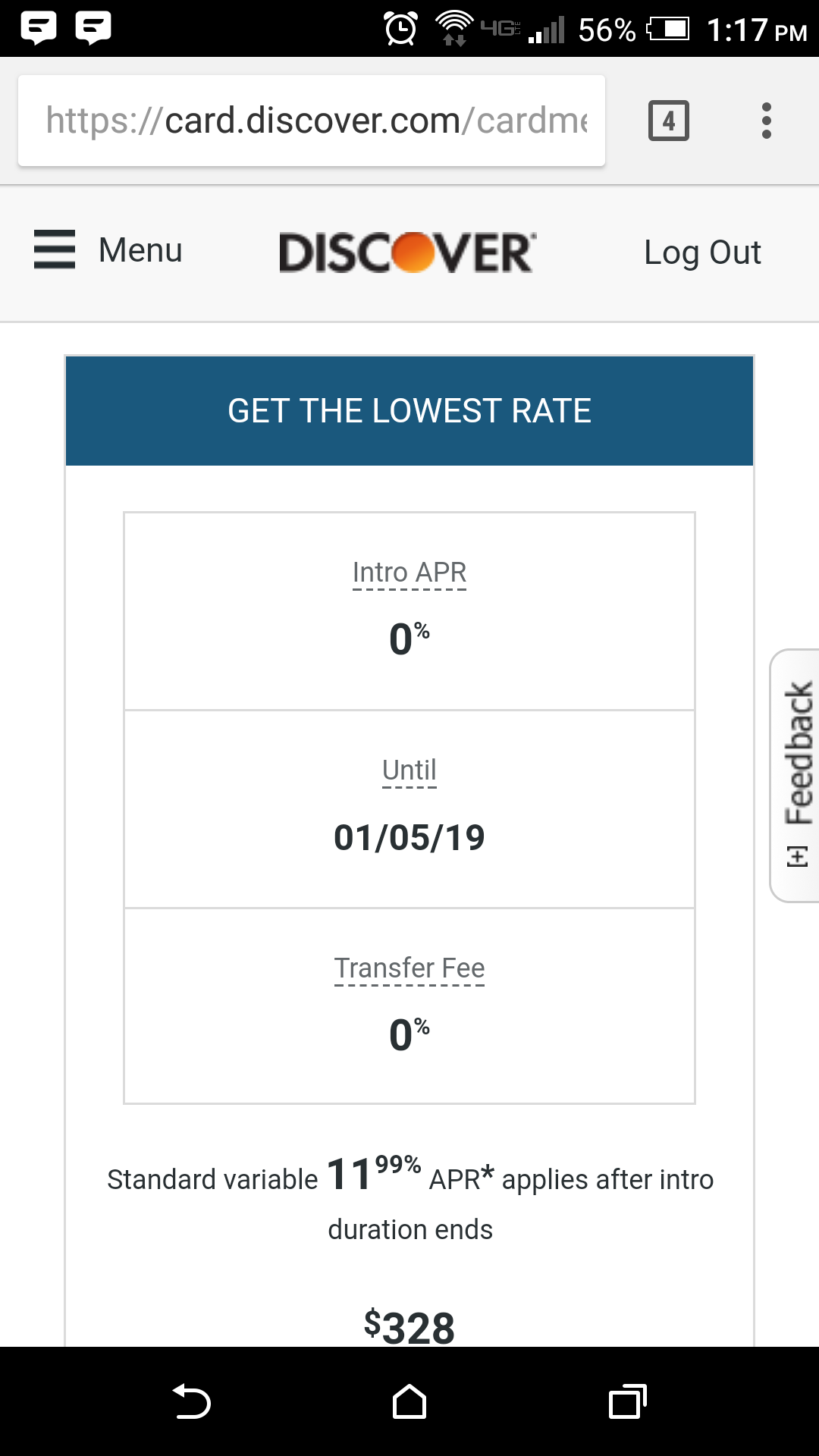

New card, received the offer in the mail (along with an offer code). $0 transfer shows up as an option in the balance transfer section of the Discover website after activating the card (see screenshot).

Does anyone knows what happens when the BT term expire and you still have balance on the card for few more days.

Originally, I did a BT on Alliant card which expires in 3 days. I already requested BT to Barclaycard Ring few days ago but it is still processing. Should I be worried if BT does not go through in next day or two?

Thanks.

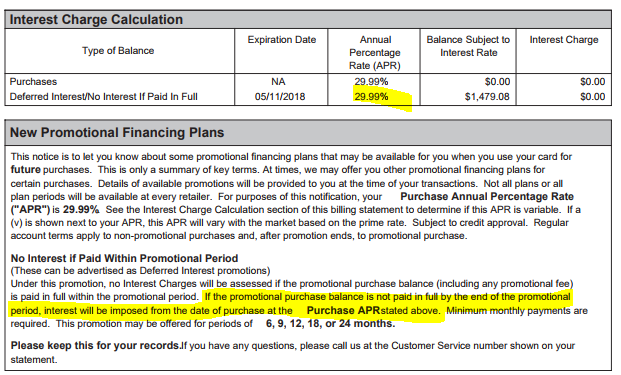

Depends. The issuers like Synchrony typically accrue the interest and if the balance isn’t paid by the end date of the promotion, all of that accrued interest posts to the account. But it seems most credit unions just start charging on the remaining balance.

My 0% BofA offers have an end date explicitly on the statement, and presumably they switch to my regular rate on a daily basis after that. You would have to be more careful if it was one of those that somehow charges interest retractively back to the start if you don’t pay it off when the promo period ends.

Also, BTs can take longer than you expect, so be cautious planning anything with them on a tight schedule. Give yourself two weeks to be safe I think.

Thanks Guys.

I spoke to Alliant CSR and was told that there will be no retrospective interest charges.

Also, they charge interest on a monthly basis and as long as there is no balance when the next statement cuts I will not be paying any interest.

First part is also confirmed by MagnifyMoney:

What happens if I don’t pay off the balance transfer at the end of the promo period?

Once the introductory period is over, interest will start to accrue at the standard purchase interest rate on a go-forward basis. Interest during the introductory period is waived — so you do not need to worry about a retroactive interest charge.

Ah, that wasn’t clear to me. Sorry, I thought that was intended to be generic. I knew your case was Alliant, but unsure what the MagnifyMoney thing was about.