Although I consider myself quite knowledgeable about federal income tax preparation, there is one area that I’ve never quite been able to figure out. I hope someone can explain.

Is there a way to estimate what the 1099-DIV from a particular payer will look like based on transactions reported throughout the year, and year-end distribution estimates? The transactions are always labelled fairly generically such as “Dividend” but don’t tell me qualified or not, and it seems the numbers never quite line up with the boxes on 1099-DIV either.

I’m trying to do some very specific tax estimating for 2018 before taking some year-end actions, and I’d like to be able to estimate this accurately. I’m aware that many dividends are paid late in the year, so I’ll have to rely on their estimates. That’s OK.

If the answer is “You can’t possibly know until you get the 1099-DIV” then I can at least stop trying to figure it out.

For reference, I’ve cut and pasted definitions of terms used on 1099-DIV.

Ordinary Dividends . Dividends paid out from a company’s earnings and profits are referred to as ordinary dividends. They are taxed at normal income tax rates. Many real estate investment trusts (REITs), for example, pay out ordinary dividends, which can raise your overall tax burden. These are sometimes referred to as “non-qualified dividends” and are reported in box 1a of the 1099-DIV.

Qualified Dividends . Dividends may be considered qualified if they’re paid by a U.S. corporation or qualified foreign corporation and you’ve met the holding period requirement for the underlying stock. Qualified dividends are subject to long-term capital gains tax rates and are reported in box 1b on your 1099-DIV.

Capital Gains Distributions . You may also receive payments from your dividend-paying stock in the form of capital gains distributions. These are generally received from mutual funds and are reported in box 2a on your 1099-DIV and are subject to long-term capital gains rates (regardless of how long you owned the shares).

Go through all dividends received during the year, look at the underlying security which paid those dividends, and check to see if you’ve held that security long enough (you should have looked for the definition of “holding period” for qualified dividends): “Common stock investors must hold the shares for more than 60 days during the 121-day period that starts 60 days before the ex-dividend date. For preferred stock, the holding period is more than 90 days during a 181-day period that starts 90 days before the ex-dividend date.”

The Total Cap Gain on the 1099-DIV matches the LT Gain actually paid. So it doesn’t make sense to me that it is called Total Cap Gain if it includes only LT.

As for Total Ordinary Dividends and the Qualified Dividends shown on the 1099-DIV, I’m not seeing how those relate to what was actually paid. [Note: No other box on the 1099-DIV has numbers, except foreign tax paid].

Also, if it is possible to calculate what the 1099-DIV will look like based on actual transactions shown in the account during a tax year, then why do 1099-DIVs take so long to be produced? Most are sent in mid-February, while some such as real estate and small value funds may not come out until mid-March. I can’t get over the notion that there is more to it than you can glean from looking at the actual transactions showing during the year.

I’ve still been trying to find the answer to the question, and admit to still not knowing. However, I think what makes it complicated is that qualified ordinary dividends aren’t a function of how long you’ve held the fund, but how long the fund has held the stock that makes it up. If you own mutual fund XYZ that holds 500 different stocks, the fund holder cannot practically calculate based on the individual holdings. The best you can get is the fund manager’s estimate of QDI.

Of course, how long you have held XYZ fund comes into play when you sell XYZ and are calculating your capital gains on the fund.

Still unsure why funds can’t provide a best guess 1099-DIV -like report, except they might be concerned that idiots will file returns based on that information.

BTW, here’s the dividend estimates for Vanguard: http://vanguard.com/pdf/RET891511_122018_final.pdf. If anyone can describe the algorithm for turning these columns into a guess version of 1099-DIV, I’ll buy you a beer.

it really depends what you invest in. if it is just simple stock, then you already know what will be on your 1099-div.

if you invest in fund, you will have to wait until end of feb because your dividend will needs to be income reallocated. let say you invest in a bond fund and get sh1tload of dividends from it, it will most likely break down to interst and return of capital, which shouldn’t be on 1099-div, but 1099-int instead.

if you want to avoid this, do not invest in any funds.

oh, each fund will post their income reallocation after year end on their website. you can calculate the break down yourself, that’s if you are going to check for each one.

if you really want to do estimate, use last year break down.

I used to do tax reporting for a living making these statements.

The STCG and LTCG amounts should be self explanatory, although the final amount may differ a little from the estimate. Stil, before EOY you’ll actually get paid the capital gain distributions and you should be able to see the breakdown at your brokerage (these are reported separately). For cumulative dividends paid during the year, use their QDI% to split that total between ordinary and qualified dividend categories.

In general, especially for more complicated funds, the breakdown of their distributions throughout the year can be lots of different things - return of capital, short or long term capital gains, qualified or not qualified dividends, maybe some weirder stuff too. The best guess is usually last year’s breakdown if you can find it, perhaps from your last year’s taxes or someone who held that invest previously. Sometimes the IR section of the fund or companies website may have the tax info from prior years generically presented.

I am continuing to research this but still don’t have answers sufficient to make estimates. Let’s put aside estimates. Let’s assume we are past the declaration and payment dates, so all distributions for the tax year have been made and posted to the account. Since you are being taxed on what distributions were actually made to the account, the amount of the distributions are known by December 31. What isn’t final is the characterization of dividends as qualified or not, although a reasonable estimate is available (the QDI). Right so far?

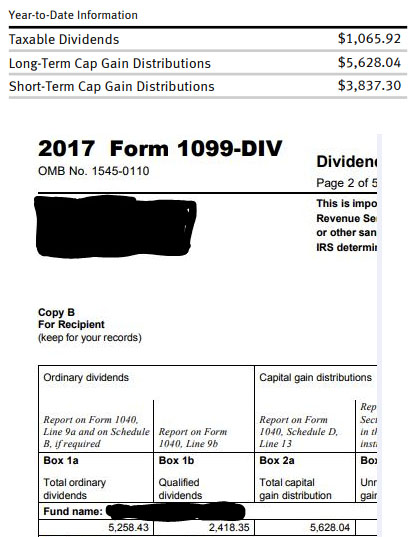

So let’s take actual numbers from a mutual fund from 2017. No changes/corrections made between year-end statement and 1099-DIV. In 2017, this fund paid only the following distributions on 12/18/17:

Dividend 0.25 per share

ST Cp Gn 0.90 per share

LT Cp Gn 1.32 per share

I held 4263.665 shares on record date, so

Div 1065.92

ST Cp Gn 3837.30

LT Cp Gain 5628.04

These were the amounts I actually received in 2017 as income.

Now, on the 1099-DIV, the Qualified Dividends was 2418.35, so the non-qualified dividends was 2840.08.

I see that the Total Cap Gain on 1099-DIV was 5628.04, which is the amount of LT Gain. This raises the question … why does Total Cap Gain not include ST Cp Gain?

And the second question is where the amount in 1a - total ordinary dividends comes from. Total ordinary dividends is the total of qualified and nonqualified dividends. It seems like ST Cp Gn is unaccounted for, and therefore must play a part in the ordinary dividends. But I haven’t found any permutation of the numbers to produce what was on the 1099-DIV.

For those scoring at home, I’ve finally figured out two reasons why dividend and capital gains transactions actually paid to the account differ from what’s reported on 1099-DIV.

Certain transactions are posted/dated in early tax year + 1, but are taxable in tax year. You may not see these if you look for all tax event transactions for tax year.

Foreign tax paid is included in Box 1a since it is income you realized and was then paid out (of course, that amount can be taken as a deduction or credit). As far as I know, there’s no place to see an accounting of what dates the income was realized.

So there you have it … bottom line is that it is simply not possible to make exact calculations of 1099-DIV income, even early in tax year + 1.

[Side note: Of course the purpose of the exercise is not to file prematurely. The purpose is that certain year-end actions require good estimates to avoid exceeding certain thresholds.]