2018 limit is $6,900. Since 2017 is almost over, my guess is that @ritholtz signed up to make contributions starting next year.

A quick reminder - if you’re going to be turning 55 at some point next year, you’re eligible for the $1000 catch-up contribution.

Yes. My elections are for 2018.

Thanks

I have questions for you all. I am enrolling in High Deductible Health plan for 2018. Am I allowed to contribute anything for 2017 although my health plan was regular (non HSA qualified) account? I was hoping to capitalize for 2017. The plan I had for 2017 is/was for $2500 individual and $5000 Family deductible. What do you guys suggest?

ETA: This is what it says in my insurance card:

Deductible (Ind/Family): $2500/$5000

OOP Max: $6800/$13600

HDHP in 2018 won’t make you eligible to contribute to HSA for 2017 - it’s a monthly test (except for the December/13 month rule which wouldn’t apply if you’re starting your new coverage in January).

As for your current health insurance - that looks like an HDHP plan. Any particular reason you don’t think it’s an eligible HDHP for HSA purposes? Do you have an FSA?

Those numbers seem to be within the range that could be an HSA eligible plan, but it’s not possible to tell based on just deductible and OOP max. There are many plans with high deductibles that are nonetheless not considered HDHPs.

The main reason for this is that a plan may also offer things like office visits that are not subject to deductible but only a copay (beyond the one annual preventive visit allowed and required with no copay under ACA plans). This may be a desirable feature to have the plan pay for something other than just preventive care before meeting deductible, but it breaks HSA eligibility.

I have a HDHP currently. However, my employer pays the deductible and copays. I think this makes the plan ineligible for HSA. Does anyone have a good handle on these rules?

TIA

@gremln007 I’m not an expert but I have read IRS Publication 969 pretty carefully and it sounds to me as well like this would make it HSA ineligible. Depending how they’re paying your deductible and copays it sounds like it could be some form of health reimbursement arrangement, and outside of exceptions for limited purpose accounts (only paying things like dental and vision) those would be disqualifying.

Employers are allowed to contribute to their employees HSAs though, allowing the employee to then use that money to pay for deductible and copays. If that’s the only thing disqualifying your plan it would seem a better arrangement for you. I believe there may be some benefits of HRAs to the employer though, such as retaining unused funds whereas HSA funds remain with the employee even after the end of employment.

2 Likes

Thought I would point out a promising newer HSA provider for investments: Lively

Like some other providers they offer a linked TD Ameritrade for investing at $2.50/month. What seems to be better than some others is the fee for investment is relatively low and and they have no minimum cash balance. Evidently the monthly fee can even be taken from a linked bank account rather than the HSA balance.

My only hesitation is they seem to be a pretty new startup with a very small staff. Hard to say how they will do longer term. They are not a bank, but appear to be partnered with Choice Financial for the banking side of it. Hopefully even if they fail Choice Financial/TD Ameritrade could unwind things without too much trouble.

Further discussion over at Bogleheads Lively HSA offers first dollar investing - Bogleheads.org

3 Likes

Just got hit with a nearly $10 monthly fee (.0333%/month) for my investments on whevever Alliant sent my HSA. Obviously pissed at the huge fee. Anyone else have suggestions at free/cheap places to invest?

Thanks for this topic OP. After reading, I am intrigued by maybe an opportunity we are not taking advantage of. My family (spouse and children) HDHP is offered thru my employer. Our HSA is funded after tax privately to HSA Bank contributing the maximum family amount per year and we plan to defer reimbursement until retirement. My wife is an individual business owner, her company and has normal business income and expense. Is it possible to pay a portion of our after tax HSA contribution as an expense to her company? Whereby reducing the self-employment tax she pays? (The answer appears to be NO because it would only be for herself.)

http://www.insuranceisboring.com/individual/health-savings-account/hsas-for-small-business-owners/

If employees were involved (Then Yes)

Edit (this explains some of it, but can I take it as a business expense?):

https://www.zanebenefits.com/blog/how-hsa-contribution-limits-work-for-spouses

Edit (this seems to explain it can be a business expense but how about for an individual (sole) business)?

The article above states that we MUST have our our HSA accounts (one for each spouse) and that by agreement her business can fund 100% of the HSA. I am looking to see how that is reported.

Edit: (This seems to indicate the an HSA contribution can be a self employed business expense.)

Have used a Health Savings Account in my Credit Union (Michigan State University Credit Union) for years without any fees. Good CD rates but as far as investing I don’t know. I use my IRA funds for investing.

The fees at HSA Adminstrators (https://healthsavings.com/) are consistent with others. I would use it for investment HSA’s only. They have Vanguard funds. https://healthsavings.com/vanguard/fees/

If your HSA is used every year consider looking into local credit unions if you have any. The returns will be crappy but the fees may be minimal.

What kinds of investments are you looking for? From my research, I couldn’t find any brokerages offering HSAs that didn’t charge a monthly/quarterly/annual fee. But there are plenty of banks which do offer free HSAs.

Optum Bank has a wide array of investment options and charges $3 a month.

Sorry, I guess for me I should have been clearer. My HSA has about $34K in it and we aren’t putting more in it at this time (we are funding my wifes). Looking to invest 65/15/20 (Dom Stock/Intl Stock/Bond). In the HSA Alliant sent my money to that is currently VVIAX, VTPSX and VTABX.

I’m not looking for anything fancy. Just a place to put and invest the money in low ER mutual funds (for me that has always been Vanguard funds).

I think it is $3.25/month for the admin (banking side) and then there are costs for the investment fund you choose. If not let me know I would love to escape the fees.

I don’t think anyone mentioned this yet…

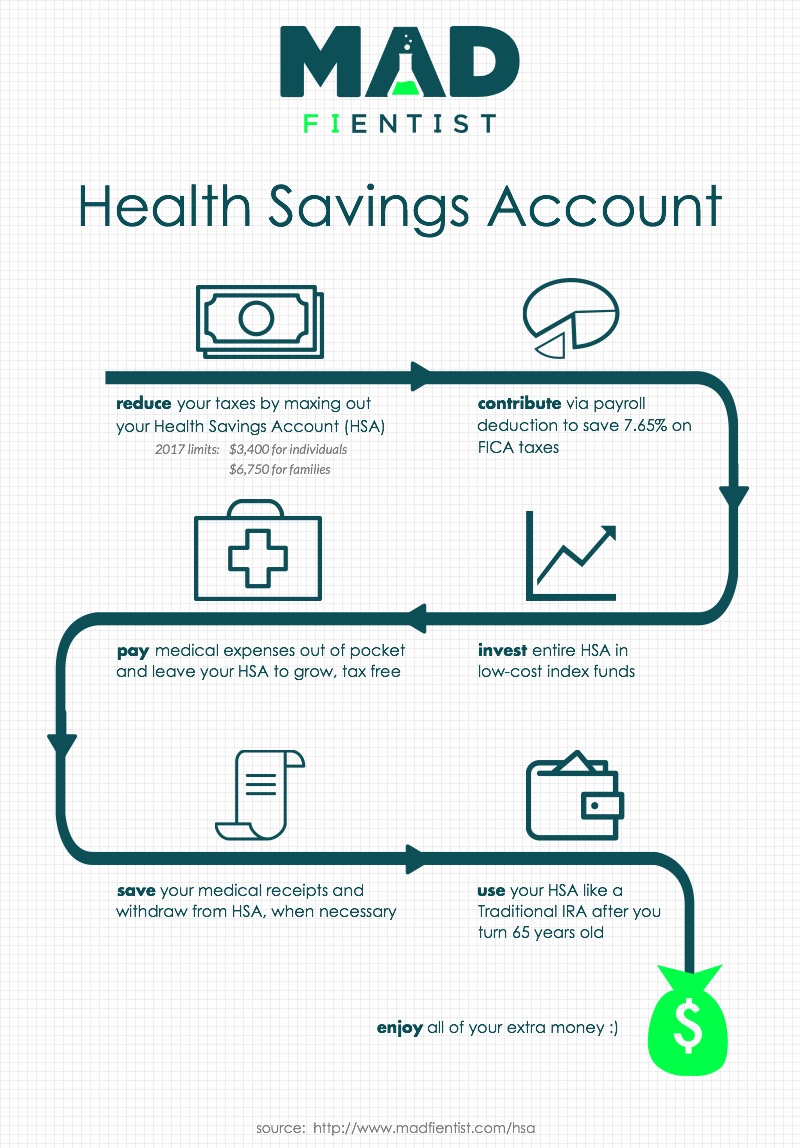

Great write-up here: HSA - The Ultimate Retirement Account

And for visual learners: https://www.madfientist.com/wp-content/uploads/2016/10/health-savings-account.jpg

{kind=link}

3 Likes

I just signed up for this yesterday. Seems like a no-brainer. My wife and I are in our reproduction years ![]() Medical expenses are flowing. My goal is to do the long play and document the heck out of every medical expense (screenshots, CC statements saved, etc), and let the HSA grow and grow.

Medical expenses are flowing. My goal is to do the long play and document the heck out of every medical expense (screenshots, CC statements saved, etc), and let the HSA grow and grow.

Will report back with more info as I experience more with Lively.

The “Great Write-up” posted by @gremln007 just above my comment is what motivated me to pull the trigger on an HSA. With a family plan, we can sock away almost $7k per year into this “retirement” vehicle.

And, I’m self-employed (LLC S-Corp), and intend on making the deduction from payroll to save on FICA. Lots to be happy about here. Edit I think I’m wrong about this working in my favor. Here’s a couple write-ups (1 and 2) discussing the limitation.

1 Like

Question about keeping receipts to claim much later. What length of time do you need to keep receipts? After say 20 years, who’s gonna be able to confirm or disprove whatever you have as receipts?

As long as it’s not something really way off (like claiming expenses for procedures not appearing on your medical history), I’m guessing neither the IRS nor the service providers will be able to provide any info on those receipt.

Is there some guidance from the IRS on this?