That is a good article. Here’s a good money quote from it

There is also the impact of capital gains taxes to consider. Say you purchased an asset for $100 last year, and today it is $108.10. While you made $8.10 in nominal terms, in real terms, your investment is still worth exactly the same as it was when you purchased it. However, when you go and dump the investment, you owe the government another $1.08 in taxes at Ontario’s highest marginal rate, so you’re actually sitting in the hole. You needed a 11.1% nominal return to ‘break even’! Compounded annually, inflation is a gigantic tax vacuum for the government – and whether you like it or not, we are all paying for it.

The latest plot from the guys ru(i)nning the Strategic Re-election Reserve.

Aside from bragging about gas prices falling recently and blaming Putin for Biden’s self inflicted economic woes, the key takeaway is they want to give themselves the new right to buy future oil contracts to refill the Reserve at guaranteed/fixed future prices, rather than market prices.

Currently they can say something like “we’d like 1M barrels of oil on 11/5/22 and we’ll pay the market price; sign up if you’re interested”. If they approve themselves for this new tactic, they can say “sign up to give us 100M barrels of oil on 2/1/25 and we’ll pay you $125/barrel even tho the market price is only $95-100 and expected to stay there”.

Why would they do that? The first clue is they don’t intend to use this until 2024.

the actual delivery of these volumes back to the Reserve will not take place until well into the future, likely after FY 2023.

and the second clue was that they’re dumping all the oil they can now, and at unprecedented and previously thought impossible speeds, until right before the 2022 midterm elections.

one major bank estimated in March that the maximum drawdown capacity of the SPR was only 500,000 barrels per day. Nonetheless, the SPR is executing at a speed that is about twice that level.

So knowing Biden is a lame duck and with poor prospects for any 2024 Democratic presidential candidates, the political architects managing the Reserve are setting up a way to raise future oil prices on the next President in retaliation. By being able to waste taxpayer money paying a premium to market for future 2024 or 2025 delivery, you can suck up the supply that would have been produced and sold around and immediately after the 2024 election and take it off the market en mass at high prices, leading to a price spike in oil and gasoline just in time for the next guy to take the fall for it. Pass the buck!

That’s one meal per month, or quarter, right? Not only is the brown paper bag more financially responsible, it is also probably safer and healthier. My wife has a pretty good paying job, making more than, probably 80+ percent of the employees at her location. She is one of only three people who bring their own lunches every day.

The makers of Coca-Cola beverages, Dove shampoo, Huggies diapers and Big Macs have been raising prices as their costs increase on everything from wood pulp to wages. The executives behind these global brands on Tuesday said they would keep passing along those costs to shoppers, for now. Consumers are continuing to buy even as inflation takes a toll on households, these executives said.

The central bank is likely to raise its federal-funds rate Wednesday by 0.75 percentage point, to a range between 2.25% and 2.5%. While further rate rises are likely this year, Mr. Powell might provide less specific clues about their sizes, according to several analysts. That’s because such reticence would give officials more flexibility in planning their next few moves. They have raised rates at a historically rapid pace this year and the outlook for inflation and growth is highly uncertain. They will have several more reports on hiring and inflation before their Sept. 20-21 meeting.

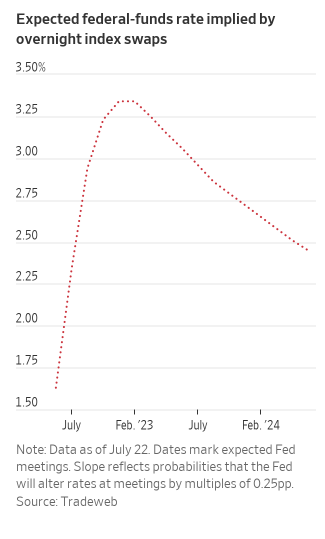

And farther out,

Investors bet Fed will need to cut interest rates next year to bolster the economy . As the Federal Reserve prepares to meet this week, Wall Street investors are betting that officials will raise interest rates aggressively through the end of the year—and then turn around and start cutting them in six months.

FED’S POWELL: LABOR MARKET IS EXTREMELY TIGHT, INFLATION MUCH TOO HIGH

FED’S POWELL: WE ARE CONTINUING PROCESS OF SIGNIFICANTLY REDUCING OUR BALANCE SHEET

FED’S POWELL: THE FOMC HAS THE TOOLS TO RESTORE PRICE STABILITY

FED’S POWELL: ALTHOUGH PRICES FOR SOME COMMODITIES HAVE TURNED DOWN, EARLIER SURGE HAS BOOSTED PRICES, INFLATION PRESSURE

FED’S POWELL SAYS OVERALL LABOR MARKET SUGGESTS UNDERLYING AGGREGATE DEMAND REMAINS SOLID; SAYS ALTHOUGH PRICES FOR SOME COMMODITIES HAVE EASED, THERE IS STILL ADDITIONAL UPWARD PRESSURE ON INFLATION

POWELL: WE ARE LOOKING FOR COMPELLING EVIDENCE INFLATION COMING DOWN OVER NEXT FEW MONTHS

POWELL: PACE OF RATE INCREASES WILL DEPEND ON DATA

FED’S POWELL: ANOTHER UNUSUALLY LARGE INCREASE COULD BE APPROPRIATE AT NEXT MEETING

FED’S POWELL: LIKELY WILL BE APPROPRIATE TO SLOW PACE OF INCREASES AS RATES GET MORE RESTRICTIVE

POWELL: ANOTHER UNUSUALLY LARGE INCREASE TO DEPEND ON DATA

POWELL: WOULD NOT HESITATE ON LARGER MOVE IF NEEDED

FED’S POWELL SAYS 75 BPS WAS RIGHT CALL IN LIGHT OF THE DATA; SAYS JUDGE 75 BPS WAS RIGHT MAGNITUDE IN LIGHT OF DATA, CONTEXT OF ONGOING RATE INCREASES

POWELL: WE ARE WATCHING FOR SLOW DOWN IN ECONOMIC ACTIVITY

POWELL: LIKELY FULL EFFECT OF RATE INCREASES HAS NOT BEEN FELT YET

POWELL: OUR THINKING IS THAT WE WANT TO GET TO MODERATELY RESTRICTIVE LEVEL BY END OF THIS YEAR; THAT MEANS 3% TO 3.5%

POWELL: LAST INFLATION REPORT WAS WORSE THAN EXPECTED

POWELL: IT’S NECESSARY TO HAVE GROWTH SLOW DOWN

POWELL: WE DON’T THINK WE HAVE TO HAVE A RECESSION

already discussed here but worth repeating, the amount of reduction is really trivial, ramping up to $95 billion per month by September. They have about $9 trillion in inventory so if they hold to plan, it will take about 100 months to reduce to zero.

So if inflation continues apace we will enter into

STAGFLATION

In economics, stagflation or recession-inflation is a situation in which the inflation rate is high, the economic growth rate slows, and unemployment remains steadily high. It presents a dilemma for economic policy, since actions intended to lower inflation may exacerbate unemployment.

They’ll need a new word, since while we have had relatively low “labor force participation” going back to the Great Recession, our “unemployment” is not “steadily high”.