MYGAs, which is an abbreviation for multi-year guaranteed annuities, are CD-like investments. They are also known as fixed annuities. The following is a comparison between MYGAs and CDs:

Those terms arent terms like with a CD, right? They’re rate-lock periods, after which you get the market rate - and chosing to instead withdraw your money may trigger a 10% penalty.

These products are intended to be held until you are 60.

Not sure what you mean by “Those terms arent terms like with a CD”.

A 3-yr 4.4% MYGA earns you the same amount as a 3-yr 4.4% CD on maturity. Some of the differences are

o All earnings on the MYGA are tax-deferred until maturity. And you can continue to defer taxes by doing a 1035 exchange into a new MYGA when the old one matures. On the other hand, for CDs, you have to pay taxes on the interest every year. (We are talking about non-qualified or taxable account).

o There is an additional 10% federal tax penalty on the earnings if you withdraw the money before age 59.5.

o MYGAs usually have punitive early withdrawal penalties. So don’t buy these if there is a chance that you will surrender early. But, many MYGAs do allow you to withdraw 10% each year without early withdrawal penalties.

o There is no FDIC insurance, instead you have the state insurance guaranty fund. More risky for sure. See the following for each state’s insurance limits:

Because it’s essentially like making a taxable IRA contribution. Yes it pays interest the same as a CD, but the underlying mechanics behind it are pretty significantly different.

Yes, it is like a taxable IRA contribution in a sense in that earnings are tax-deferred until withdrawal, with the associated tax penalty if withdrawn before 59.5.

The difference is that you need earned income to contribute to an IRA and the contributions are dollar limited. Not so with MYGAs.

It’s an intriguing option. Especially for right now, rather than hoping 4% CDs materialize in the next couple months (as someone here has assured us will happen ).

Have you reached maturity on any of your purchases yet?

My first MYGA was a 3-yr 3% bought during the CD drought in 6/2020. It will mature next Jun. I plan to do a 1035 exchange into another MYGA and continue to defer taxes.

Yeah, I know the reference to the 4% CD.

But as I posted in the CD thread, I think getting there is not a sure thing. My crystal ball is hazy whether we can even get there.

I am seeing a 3-yr MYGA at 4.10%. The company, Guggenheim Life Insurance, is rated A-

Where do you see 4.4%? Is that for lower-rated companies? How low are you willing to go rating-wise?

You get the better terms if you apply directly to them at https://www.gainbridge.life rather than through Blueprint Income (Gainbridge save on commissions paid to Blueprint to give you a better deal).

In fact I just applied for their 3-yr 4.4% MYGA today.

Is there any advantage to having used the broker when the annuity matures and you need to do a 1035 exchange to avoid the tax penalty? Or is the account held no different than one purchased directly, once the purchase has been made?

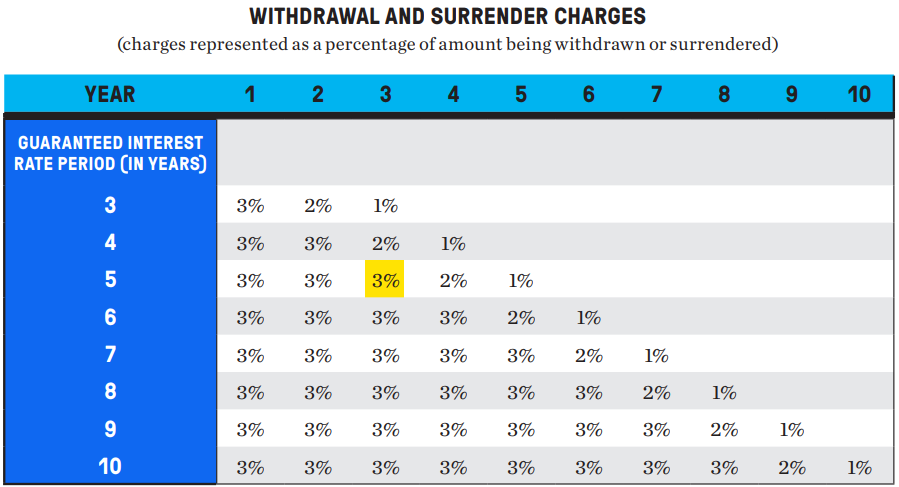

Thanks. I can’t find the surrender charges for the first three years. It does say that you can withdraw 10% of the MYGA penalty-free in the second year, but it doesn’t say what the penalty is if you go over that threshold. Do you know what it is?

I have not done any 1035 exchange yet so I can’t speak from personal experience. But for all the MYGAs I owned, I was able to setup online accounts with each of the insurer, and you service the policies from there yourself. I don’t go through Blueprint anymore after the policy is purchased, so I’m not sure of Blueprint’s role, if any, when I do the 1035 exchange.

What I have heard though is that when the time comes for the 1035 exchange, you apply to the new insurer, give them the information of the old insurer and the new insurer will request the funds from the old insurer. And maybe you might have to contact the old insurer to ask them to release the funds … I’m not sure.

There are two parts to the withdrawal penalty if you exceed the penalty free threshold. The first part is a yearly decreasing percentage and the second part is the MVA (market value adjustment). Both of these apply only to the portion that exceeds the penalty free threshold.

For the percentage penalty, most MYGAs start off with 9% and then reduce by 1% each year. E.g. for a 3-yr MYGA, the penalties would be 9%, 8%, 7%. For a 5-yr, it would be 9%, 8%, 7%, 6%, 5%.

But here comes the interesting part: if you get the MYGA directly from Gainbridge, the surrender penalties start with 3% instead of 9%. The following is a table from Gainbridge

Is there any actual “insurance” happening with these things? From the last link,

Here’s how a typical MVA works: When you purchase a MYGA or FIA annuity, your premium earns a fixed rate of interest. This rate is guaranteed by your insurance company. The insurance company, in turn, invests your premium in interest-bearing investments, like bonds or mortgages, with durations that match the rate guarantee period of your annuity.

I just don’t understand why you’d lock up your money to invest in this MYGA with high surrender charges and such if you could just buy the same bonds, mortgages, or whatever for the yield target you’re looking for? Or are they buying some stocks and some bonds and hoping to beat the market and pay you less, and they just tell you this line about a fixed income backed portfolio? Because i’m sure that whatever it costs to buy an ETF or mutual fund to own that type of stuff, an insurance company would charge way more in fees.

Isn’t it a lot like the concept of health insurance? Sure, you could invest in the same bond paying 5%, but there’s risk. So you take 4.5%, in a pool with 9 other people, with the assumption one of those 10 bonds will go bust, eliminating the risk that it is your bond that goes bust. Not exactly what happens, of course, but conceptually. You’ve eliminated the direct risk by pooling funds and letting the insurance company backstop potential losses by guaranteeing a certain return. Leaving you only with the risk the insurance company is bad at managing their investment portfolio to the extent of going bankrupt. And the high surrender charges are no different than the risk you face should you end up needing to sell a bond you own before maturity.

Isn’t your question a lot like asking why you’d put money in a CD, when you could direct loan your money to the same customers who take out mortgages and car loans from the bank funded by your CD deposit?

An ETF or mutual fund is perpetual, without a defined timeframe, leaving you exposed to interest rate risk (which affects your total investment value) no matter what length you want to invest. That ETF may pay 4.5% interest for 3 years, but after 3 years the fund value may also have declined 10%. The MYGA ensures not only you earn the fixed APY, but also that your principle will be 100% at the end of the fixed 3, 5, or whatever term.

So the life insurance company actually issuing the 4.4% MYGA is Guggenheim Life Insurance. It’s a relatively new company (less than 10years?) and fairly small with a few billion in assets. Group 1001 recently acquired the insurance company from Guggenheim Partners, a giant mutual fund company. Although they have a A- rating, they do not have a long history nor have they been in existence through a financial crisis, like the one we had in 2008-9.

I live in California and our state insurance fund will only guarantee 80% of your annuity. The fund is not like the FDIC, which is underwritten by the federal government. If the fund becomes financially distressed, it can delay or prohibit payments to annuity owners.

This is not a risk-free investment. I am going to look at the financial statement of Guggenheim to see if I am comfortable with their balance sheet and income statements.

I mean, there are fixed term ETFs and such too that avoid the “perpetual fund” reinvestment risk you may not want. For example, there’s a “Bulletshares” line of investment grade portfolios, high yield portfolios, etc, that terminate each EOY so you can pick whatever term you want and their holdings all mature (or are sold I guess) at that point. Here’s a generic 2026 Corp one -

It matures 12/15/2026 for about 4.5 years, yields almost 4.5%, and has an ER of only 0.1%. This is basically a 4.5 year investment grade corporate debt basket, prepackaged for 0.1% in annual expenses.

The Index seeks to measure the performance of a portfolio of US dollar-denominated investment grade corporate bonds with maturities or effective maturities in 2026

Fund Characteristics

Effective Duration 3.60 yrs

Modified Duration 3.61 yrs

Yield to Maturity 4.44%

Yield to Worst 4.43%

Weighted Avg Life 3.91

Weighted Avg Coupon 2.99%

Weighted Avg Price $95.54

as of 07/01/2022

Of course your yield might be a bit lower if we see some defaults, but for investment grade that’s not too likely and is more diversified presumably than taking investment grade credit exposure to this one insurance company writing the MYGA.

Plus you can sell BSCQ for free at your broker for just a nominal spread, not a 3-9% screw job if you want to sell more than 10% of your investment for some reason. Here’s the last two weeks chart, compared to LQD (perpetual investment grade corporates ETF) and VGIT (intermediate term treasuries).

I guess there’s some nominal value to tax deferral on the MYGA vs the debt ETF, but I’m sure I would never invest in the MYGA instead of a liquid etf with the same expected return.

Not really. You either get sick / die early or you don’t, and the premiums from the survivors payout the unlucky ones or their heirs. You can’t diversify mortality risk by living multiple lives with an average health or life expectancy. To the extent you’re risk adverse as to this outcome, the insurance companies give you a bad deal, ie higher than expected cost premiums, to do the diversification for you and collect the extra value for themselves if they got the average numbers right.

For investments, it’s a lot easier these days to diversify via some cheap index financial product like a mutual fund or ETF, so you don’t have to own a single riskier corporate bond instead of a broad basket of them.

You can sell it for free, but you could be selling it for 3-9%+ less than the price you bought it - BSCQ currently has a YTD return of -7.65%. Had you bought at the beginning of the year for a 4-year term and are now looking to bail, that 3% surrender fee isnt looking so outrageous. The surrender fees are because they’ve isolated you from market swings - so you know going in exactly what it’ll cost to bail early, as opposed to being at the mercy of the market.

Your exposure is limited to only this one insurance company’s wellbeing, but your primary risk within that insurance company is their investment portfolio - which is likely just as diversified as any bond ETF. The difference being that that company has all their assets to absorb any losses, will absorb any losses on their side of the 4.5% rate instead of on your side, and they are backstopping you from suffering any loss at all unless their portfolio degrades to the point the entire company implodes.

).

).