Yes its practitioners and technical people within healthcare.

They figure the hourly rates based on salary rates (2080 hours in a work year). Its not meaning to imply they are not exempt salaried employees.

The BLS data does NOT include self employed people and that probably leaves out a lot of physicians. Might be a big gap in the info. Self employed physicians earn even more…

NJ enacts a 2019 Obamacare penalty to replace the one the Feds repealed.

They expect to take in $100M or so, which will be used to try to stabilize the NJ individual insurance market via reinsurance subsidies. Not an unreasonable approach.

The unreasonable part is who is paying the tax. It’s mostly middle class and lower class folks. When the federal mandate was is place, 78% of penalty payers in New Jersey had a yearly income of less than $50,000. 38% had an income below $25,000.

Japanese are overall healthier than Americans so it makes sense that they are spending less.

I checked a few quick online stats and the average American woman is 168.4 pounds versus 115 for the average Japanese woman. Some of that is attributed to height differences, but that is a lot of extra weight.

My car was low on gas this morning, so I just went ahead and siphoned some out of my neighbors gas tank. I used to vote for politicians that promised to steal for me, but I figured it was easier to just cut out the middle man.

Trump expands “association” plans, where smaller groups can now join up under a single umbrella to buy insurance similar to large group plans. Both these new groups and large group plans are exempt from the ACA’s laundry list of required coverage, so if you want to join a group without maternity or mental health benefits you’re welcome to try and pay less while you’re at it.

Under the new rule, small companies or self-employed people with a shared industry or geographic location will be able to form an association focused on a business interest and buy insurance. A regional Chamber of Commerce could offer association plans to members.

A group could use its collective membership to negotiate prices with payers and providers, according to a senior administration official. The associations couldn’t charge an individual higher premiums based on pre-existing health conditions, but they could base premiums on other factors, such as age, industry and employee classification.

Premiums could be $9,700 a year less for association plans compared with those on the individual market, according to a February report on the proposed rule by the health-consulting firm Avalere. Their premiums would be about $2,900 a year less than those for plans in the small-group market, which includes employers with less than 50 employees.

The idea sounds good to me, just as when Rand Paul proposed it, except for the lack of mandated coverage categories. What allows them to get around that? I thought it was part of the statute?

Back to the junk policies that aren’t worth the paper they’re written on, where if presented with anything more than minor medical bills, they can rescind the policy and stick you with massive medical bills. Back to annual and lifetime caps, and discrimination for pre-existing conditions.

Brace for a return to skyrocketing healthcare inflation, massive increases in medical bankruptcies, home foreclosures, and rising Poverty.

Maybe you read too quickly, or just get your daily exercise jumping to conclusions?

Brace for a return to skyrocketing healthcare inflation…

Healthcare inflation is harder to judge, but those ACA premiums have been doing a fine skyrocketing imitation since Obamacare was enacted and that’s the part you pay for sure.

Massive increases in medical bankruptcies? I suppose it is possible. But how would we determine that it is from rising healthcare costs rather than baby boomers just getting older and sicker?

It’s the super expensive procedures that put people into bankruptcy. A 5% increase in healthcare inflation means a $10,000 procedure will cost $10,500 and a $300,000 procedure will cost $315,000. The person getting the $315k procedure was gonna declare bankruptcy back when was it was $300k anyway. The other person isn’t going to declare BK over a $500. So where are the “massive increases” going to come from?

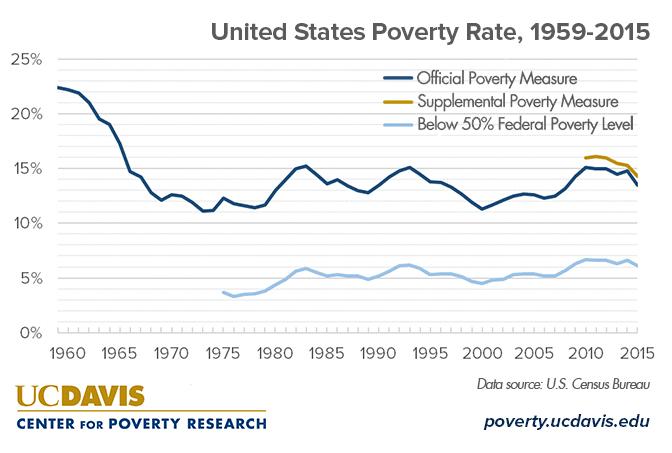

Living in a reality where the poverty rate hasn’t gone over 15% since the mid 60s.

a. Has a home

b. Doesn’t have a job that gives medical coverage

c. Is not covered by COBRA

and

d. Has a huge medical expenditure not covered by anything else

And yet, assuming that is true (i’m skeptical), how do you reconcile that

Insurance companies are losing money on ACA plans, and

Individuals are paying much higher premiums for ACA plans, and

Individual deductibles are much higher for ACA plans, so they’re paying more OOP to the extent they use services.

People are paying more to insurance companies, insurance companies are paying more to service providers, and yet healthcare inflation is down? I guess maybe useage is way up so costs are up, but per use costs are not? Or maybe in some broad sense healthcare inflation is down, but that doesn’t apply to the ACA market, so fat lot of good that does people who are stuck paying triple what they paid before for the same care under the ACA.

Those things can all happen regardless of whether or not national healthcare costs go up by 2% or 6% in a given year.

I think insurance companies are having problems with their profits because they’re having difficulty figuring the risks and pricing for ACA plans.

ACA plans are more expensive because they cover more and cover more sick people.

Deductibles are not higher for ACA plans. You can find a $500 deductible ACA plan. People often pick plans with higher deductibles because premiums are lower and they can’t afford the low deductible plans.

On average ACA plans aren’t more expensive than the actual costs of employer provided coverage.

Yes, but ACA plans actually purchased are mostly Silver and to a lesser extent Bronze (for cost reasons, as you say). The average deductible is over $4k. This is in contrast to the average group plan where the average deductible is more like $1-2k.

In addition, deductibles have been rising for a given plan. So if you get the benchmark Silver plan, the deductible is maybe 5-10% higher now than it was 4 years ago when the ACA started. Of course that’s not too much pain compared to the deductibles that doubled from the pre-ACA days and premiums that have more than doubled since then. See the table below:

I don’t know about national inflation metrics, but it’s clear insurance for individuals is now over twice as expensive as it was before.