OK, maybe they’re not technically “narrow,” but the ones I’ve looked at are still junk in comparison to the full BCBS PPO. They seem to resemble Medicaid plans more. That includes my state BCBS entity’s marketplace plans.

Sure, LA and NYC have some decent competition and probably some better plans, but there is still a large chunk of the country with inadequate competition. Even 3+ insurers seems insufficient to produce anything better than Medicaid-style plans.

Yeah thats a big problem. But no its not just LA & NYC who have choices. There are 3.5 insurers per state on average and most of the states with 1-2 insurers are low population rural states.

Most people have 4+ insurer options. I have 4 plans in my market with 2 good ones and 2 dozen plans but I’m in Portland OR. Red states on the other hand that sabotaged things from the start have it much worse… on purpose. But its not just a red vs blue state thing. rural areas of blue states are f’ed too and some red states are fine, e.g. TX.

[quote=“anotheruser”]

If we’re not going full M4A, we need to decouple healthcare from employment.[/quote]

Yeah I think this is one thing that both sides COULD agree on except for the politics in telling 90% of the country that their apple cart is going to be overturned. A lot of small biz employees will cheer, sure, but a lot of Megacorp employees won’t because they (usually) have good, cheap insurance courtesy of Uncle Sam and the employer.

Just another subsidy that hides the true cost of HC, and it’s way bigger than the ACA.

I guess what I’m really getting at is it seems like a sicker person switching from the standard employer-provided broad PPO to a marketplace plan stands a good chance of having to change at least some of their doctors. That’s the kind of test I’ve had in mind. And that seems to stand even with reasonably robust competition (like 3 or 4 insurers), but I’m sure there are exceptions.

If anything, fewer/larger insurers in a county (even one) should have an advantage here, in that network adequacy requirements will require them to contract with more doctors (enough to service the plan’s member base) than plans in a more fragmented market. That would lead to a lower chance of an employer-PPO-to-HMO person needing to switch any doctors. But that relies on network adequacy requirements being enforced. (I know Centene, which is the only option in some places, has been accused of failing to meet those requirements.)

Thinking about it further, if we moved everyone over to the marketplace, the problem should (mostly) solve itself: if everyone has a marketplace plan, doctors will need to ensure they are in enough marketplace networks to stay in business. Right now a lot of them can (and do) just contract with networks used by group plans and ignore the individual marketplace.

Yeah. But then I’d expect that if I switched employers that I’d also face a different plan with different network and fair chance my all our doctors aren’t covered. Only about 50% of people at large employers are in PPOs now so its not as if everyones in a broad inclusive PPO to begin with.

Seventy-three percent of covered workers in firms offering health benefits work in firms that offer one or more PPOs; 58% work in firms that offer one or more HDHP/SOs; 37% work in firms that offer one or more HMOs; 10% work in firms that offer one or more POS plans; and 1% work in firms that offer one or more conventional plans [Figure 4.4].

I was surprised about the 50% number you mentioned and was going to ask where it came from, but now I think I see where that’s coming from:

Forty-nine percent of covered workers are enrolled in PPOs, followed by HDHP/SOs (29%), HMOs (16%), POS plans (6%), and conventional plans (less than one percent) [Figure 5.1].

They’re breaking out HDHPs into a separate category for this, even if many of those HDHPs probably have PPO-level network coverage. (Limited data points, but when I’ve seen non-HDHP PPO and HDHPs offered by the same employer, they use the same network, even if the PPO term isn’t used in relation to the HDHP.)

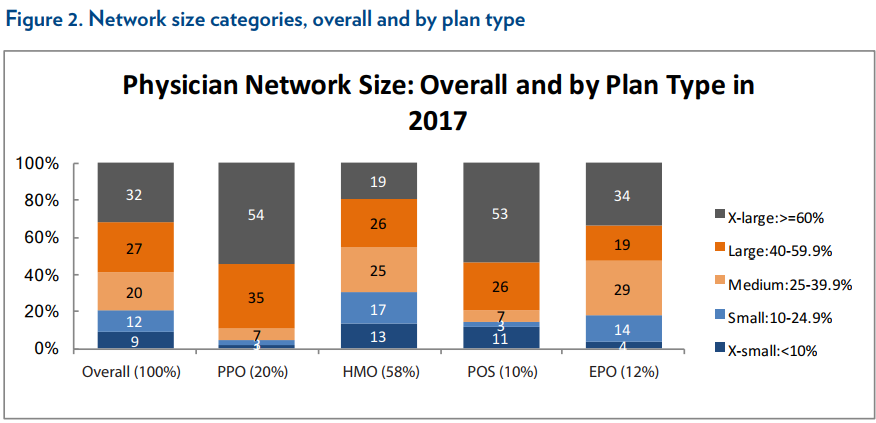

The thing is, I don’t know that all PPOs are the same. I’m thinking of the “good” networks like the BCBS national PPO I’m familiar with, but there may be some more restrictive networks that still use the PPO label. Is there data on network size for employer PPOs like what you posted for marketplace plans?

yeah. I was looking at the ~50% who are enrolled in PPOs. I overlooked the HDHP figure there. HDHP can be PPO, HMO, EPO or POS. I don’t find anything that says what the mix is though. But whatever the mix is, theres definitely a % of HDHP that are PPO so the % of people enrolled in PPO is higher than 50% when including the HDHP PPOs.

For the individual markets :

Almost all PPOs (89%) have large networks. So its almost true to assume that PPO = good network.

But that still leaves 11% with medium or smaller so its not a given.

Since 73% offer non-HDHP PPOs, I’d guess most offering HDHPs have a PPO option for that. I wish there was more data.

This individual marketplace data is probably the best we have; I couldn’t find anything specifically for employer plans. If anything, the 89% number would be larger on the employer side.

One difference I have seen is that marketplace plans usually do not cover out-of-area non-emergency care, while the usual employer BCBS PPO plan does to some extent (I realize BCBS isn’t the only insurer, but they are one of the largest if you combine all the affiliated entities). For example, looking at my state BCBS entity’s site, they do have a smaller PPO/EPO option for employer plans that only covers a few counties and probably fewer providers – but their site specifically says plans using that network cover out-of-state providers via the national PPO network. In other words, the smaller PPO actually provides better coverage for out-of-state users than in-state users (and a lot of users will be out-of-state with multi-state employers that set up plans with an insurer where they’re headquartered).

I’d guess a significant portion of that is Kaiser and similar integrated HMOs.

Yep, the tax bennies. I was specifically saying that you’re going to see a lot of employee resistance to giving up a $200/mo. or so gold-plated PPO family plan for something a lot worse (potentially) if the government tries to remove the ties between employers and insurance.

I think the only alternative at this point is a reasonable M4A replacement, trying to remove those ties on its own is a political non-starter.

But surely you’d see a lot more resistance for doubling their taxes to pay for a M4A scheme than just having to pay for their own worse health insurance out of pocket.

I think the decoupling could happen, especially since it’s something where the employer is able to shift costs on to the workers so there’s a profit motive and it can be done incrementally at a per business level. Places that offer low benefits can just dump everyone onto the exchanges and they can get their poor benefits there instead, and the subsidies for poor people will act as a buffer to too many people complaining. Industries that have high benefits will have a harder time making that transition, but when business times get tough and jobs are at risk, these types of things might be the equivalent of a pay cut. But until the exchanges offer good quality PPOs with broad coverage, this may not be feasible.

Of course the Cadillac plan tax would accelerate this a lot (dumping everyone onto the exchanges or at least billing the workers for a lot more of their healthcare costs). Remembered that tax was supposed to be paying for Obamacare by now, but union lobbying keeps pushing it back another few years every time it gets close (kinda like those copyrights that never actually expire thanks to Disney lobbying for another 20 years when the last round of political bribes are running out). If you want a model for how much resistance there is to losing good plans, looking at the politics of that is a good example.

For anyone in TN, I read some good things about the various non-ACA offerings from these guys. PPOs and Major Medical coverage, pre-existing excluded, for very reasonable costs.

I’m not necessarily opposed to a decoupling of health insurance from employers IF the money the companies was contributing is given as a raise to employees. Yes, employees would now pay tax on that income rather than pre-tax contributions to their plans, but I doubt very much that most employers would compensate their employees in full for their savings from the employer portion of plan contributions. It likely wouldn’t trickle down to employees in the form of a raise.

In the process of decoupling it, the gov’t would have to allow people to take a deduction for their health insurance premiums or the electorate would never go for it.

It may not happen overnight, but there is a thing call competition, and over the long term, people would stop working for the companies that don’t compensate well and start working for the ones that do. Without some sort of industry by industry collusion to pay below market wages (it doesn’t happen now so there is no reason to think it would happen then), employers would be forced to pay what they were paying before plus whatever they are saving on not buying insurance for that employee.

Discussion of how state level individual mandates likely run afoul of ERISA and may have difficulty achieving compliance with anything beyond an honor code.

While states can require citizens to purchase health coverage, they will have trouble ensuring compliance. Federal law prohibits the Internal Revenue Service from disclosing tax-return data, except under limited circumstances. And there is no clear precedent allowing the IRS to disclose coverage data to verify compliance with state insurance requirements.

States already cannot require federal agencies to report coverage. This means their mandates won’t track the 2.3 million covered by the Indian Health Service, 9.3 million receiving health care from the Veterans Administration, 8.8 million disabled under age 65 who are enrolled in Medicare, 9.4 million military Tricare enrollees and 8.2 million federal employees and retirees. If a successful Erisa challenge also exempts some of the 181 million with employer-based insurance from coverage-reporting requirements, state insurance mandates become farcical.

I’m not sure I follow. First, the IRS has information sharing agreements with states that allows the IRS to share information to ensure compliance with tax laws. If the state mandate is structured as a “tax” that would seem to allow information sharing.

Also, if the state audits someone and requests proof of insurance coverage, it doesn’t matter that the federal government can’t be forced to release the information. The individual would be required to provide the proof.

No employer has used Erisa to challenge Massachusetts’ 2006 individual mandate, which includes reporting requirements, but that doesn’t mean it’s legal. Last month a Brookings Institution paper conceded that “state requirements related to employer benefits like health coverage may be subject to legal challenge based on ERISA preemption.”

A 2016 Supreme Court ruling would bolster such a challenge. In Gobeille v. Liberty Mutual , the court struck down a Vermont law that required employers to submit health-care payment claims to a state database. The court said the law was pre-empted by Erisa.

Writing for a six-justice majority, Justice Anthony Kennedy noted the myriad reporting requirements under federal law. Vermont’s law required additional record-keeping. Justice Kennedy concluded that “differing, or even parallel, regulations from multiple jurisdictions could create wasteful administrative costs and threaten to subject plans to wide-ranging liability.”

Justice Kennedy’s opinion provides a how-to manual for employers to challenge state-level insurance mandates. A morass of state-imposed insurance mandates and reporting requirements would unnecessarily burden employers with costs and complexity. It cries out for pre-emptive relief.

They also talk about how the various federal agencies that provide healthcare, military / disability Medicare / etc, can’t be forced to share info with the states, and large self-insuring corporations may pose difficulties as well.

Yes, the states can audit for it, but if they have to do that for every person, it won’t be cost effective since nearly everyone is already covered. The question is whether the states can impose all the compliance and reporting costs on the Feds or the companies just to push around the individual market in their state. More for the lawyers to argue about I guess.

Oh, fair, that’s all about erisa and whether they would be allowed to mandate which could very well be true.

But if they can legally mandate, the compliance aspect doesn’t seem that difficult to me. The IRS already receives health care coverage information. I’m not aware of any reason why that wouldn’t fall under an information sharing agreement.

With regard to an “honor system” that could sort of be true, but if you have to do something like check a box confirming you have health care, and you lie, that could potentially be tax fraud. In most cases, I think that would be enough of a deterrent.