What goes into “corporate tax collections?” Because many corporations I’ve seen are still working on trying to figure out how to incorporate the changes and actually come up with numbers. Most definitely didn’t know by March how to handle the changes. Not sure how the tcja specifically would have affected these numbers, unless it was like the promise of change that should’ve caused increased collections.

Mad Fientist did a great post about the tax changes, specifically section 199A.

If you own a business, be sure to check this out.

3 Likes

Isn’t $100B/month about average for debt increases the last 12 years?

This can also work on rental income. Though I believe it has to be within a business entity, (i.e. in an LLC or other).

1 Like

I’ve read that post and the contributor’s blog it links to. I didn’t see anything about an LLC. It can be applied to individual investor’s passive income from real estate. One thing I couldn’t figure out is whether it can still be taken if depreciation puts rental income < $0. There were multiple somewhat contradicting examples with no concrete answer.

OK I may have been mistaken. I thought it needed a business entity like LLC or C corp. But seems rentals are considered a sole proprietorship without another business entity. So maybe the LLC isn’t necessary.

But also it appears that the deduction applies to net income only so if you’re showing a loss after depreciation then it won’t help.

I would encourage you and anyone else to post questions in the comments of the blog. The CPA is answering a lot of questions. I know of him from another web site and he is a solid, helpful guy.

1 Like

Treasury released proposed regulations a couple weeks ago. I haven’t read through them at all, but maybe they answer some of the questions. It’s at least worth a look.

1 Like

Basically the corporate income tax. I assume the ‘Fiscal Service Bureau’ can count.

Why would you even think that ? The deficits in Obama’s second term were $679B, $485B, $438B, and $585B. The debt to deficit ratio went from the almost 10% he inherited down to less than 2.5%. Now it’s exploding again.

So then, for the most part, the numbers from January through March of this year would not reflect the changes in the TCJA. Corporate income tax returns for calendar year taxpayers weren’t due until April.

1 Like

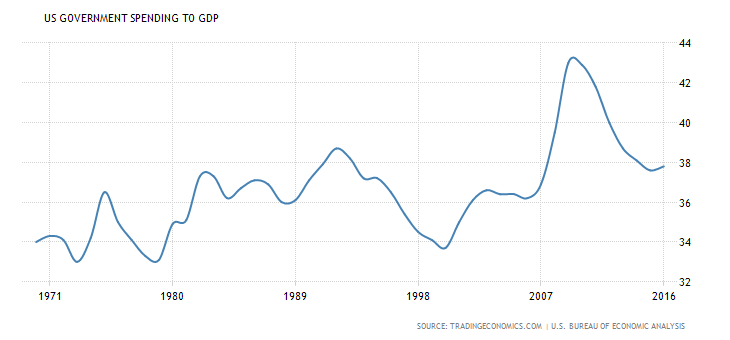

The republicans liked to point to the rising debt number when they didn’t control the oval office because it was going to go up no matter what. Which obviously is a huge mistake long term because now they do control the oval office and it is, of course, still going up. A better measure is Gov’t spending as a percentage of GDP. Unfortunately, that looks like it is going to be a loser for Trump because even though we have a growing economy, the percentage isn’t likely to go down. Hard to compare to Obama because spending to GDP shot up in the beginning of his tenure and shot back down over the rest as the economy rebounded. Gov’t grew under Obama, but long term, the economy grew at a similar rate. I’m concerned that we will be back to gov’t growing faster that the economy under Trump as soon as the economy inevitably hits a bump (or a giant pothole) in the road.

The ideal historical makeup, if you are a republican and want lower spending as a percentage of GDP, is to have a democrat in the white house and republicans controlling congress.

2 Likes

Deficit != Increase in National Debt. The national debt increase under Obama was far larger than the deficit, year after year.

Blue state end runs around state tax deductibility caps are about to be slapped down, but the question is whether preexisitng state tax donations to charity programs will become collateral damage in the upcoming guidance.

The rules are likely to halt a strategy embraced in New York, New Jersey and Connecticut, high-tax states where high-income residents are getting pinched by the cap. Tax experts are watching the rules for how Treasury handles similar credits that predate last year’s GOP tax law, including programs in Alabama, Arizona, Georgia and South Carolina.

Businesses make quarterly estimated payments.

FEDERAL debt. National debt is a whole different metric.

Eh, you posted:

Isn’t $100B/month about average for debt increases the last 12 years?

The federal deficits during Obama’s second term were less than half that.

Here’s the details of the IRS treatment for donations to the charity of your favorite tax jurisdiction. No go, unless you’re getting 15% or less for it.

https://www.irs.gov/newsroom/treasury-irs-issue-proposed-regulations-on-charitable-contributions-and-state-and-local-tax-credits (Summary)

Federal Register :: Contributions in Exchange for State or Local Tax Credits (Details)

the Treasury Department and the IRS believe that the amount otherwise deductible as a charitable contribution must generally be reduced by the amount of the state or local tax credit received or expected to be received, just as it is reduced for many other benefits.

The de minimis exception reflects that the combined value of a state and local tax deduction, that is the combined top marginal state and local tax rate, currently does not exceed 15 percent. Accordingly, under the proposed regulations, a state or local tax credit that does not exceed 15 percent does not reduce the taxpayer’s federal deduction for a charitable contribution.

The amendments to these regulations are proposed to apply to contributions after August 27, 2018.

See page 28-29 of the detailed letter for examples of the math for how this works out.

2 Likes

Aside from all the other problems of using estimated payments to determine the effect of any mid-year change, there are no estimated payments due for calendar year taxpayers in January through March.

I think they did it right for the most part (certain problems that will likely be fixed notwithstanding, to account for changes in state rates, etc). And I actually think they’re right (in their overall conclusion) both from a legal and policy perspective.

It should be noted that the regulations purport to have effects beyond just the cap.

1 Like

Why are you talking about deficits when the original metric you posted is the $500B increase in federal debt?