All you have to do is look at the rewards, which are separated by category. When the supermarket rewards and pending rewards reach $360 you’ve reached the limit for 6% grocery rewards for the year.

Cheese and crackers, it’s not that hard. I don’t consider multiplying one number by 16.6 as “math”. Differential equations on an n-space manifold is math.

Next time you pay for something in cash, after the cashier has input the tendered amount, say, “Oh I have the coins.” You can then slowly laugh or cry as you watch their wheels try to turn. ![]()

Oh, yeah. I can totally related to that. I’m the guy that hands the clerk $7.71 cents for a $6.96 purchase to minimize the number of coins in return.

But back to the thread … I was suggesting that anyone who optimizes their credit card reward points based on a balance of category spend, need for spend requirements, and purchase benefits is probably not someone who has trouble multiplying by 16.6 (with the aid of Alexa or Siri perhaps).

1 Like

That’s my opinion as well. Since I’m tracking this pretty carefully come year end, it’s not a big deal for me but it’s definitely less direct than before.

But for OP, it’s much less intuitive when your rewards changed mid-year. And either way, it’s hard to explain (other than trying to curb customer maxxing out rewards) why AMEX would take that step backward in how user friendly their rewards display is.

1 Like

From seeing how decisions of a lot of large corporations are made, I’m not sure it’s as nefarious as implied (though it could be).

But a very real possibility is someone high up said “get A done” to the person below them (not understanding what A is or what the collateral effects are). The person below them goes to IT and says “get A done.” IT comes back with “if we do A, C won’t work.” The middleman will often times just say “I don’t care, boss wants A done, do whatever you need to do.” And that’s how you end up with “improvements” causing many more problems.

3 Likes

Lol, so true. I work in IT and this happens a lot, especially at large companies.

1 Like

Hopefully if that’s what happens, negative feedback from customers should let them know they need to revert it back. We’ll see.

Intended or not, just out of curiosity, I’d be interested to see if it has any impact on the average amount of rewards claimed by customers over time.

I think keeping an AmEx without AF open is a good idea (like the 3% Blue Cash mentioned earlier).

It just sucks that everything is getting harder as people hit the Visa gift card to money order process so hard. When companies like Simon are essentially okay with that type of use, there is not much hope for every day normal, non-MS spending.

I still like AmEx offers (I never did the multiple card add-offer thing) and feel they continue to attract top merchants to that stackable program. I also like that AmEx categorizes more places as groceries than V/MC so it helps there too.

I frankly don’t think the Chase UR bonuses will last too much longer because of the noted high value and high accrual (such as the Tesla buyer via Plastiq). I only have the 5% Freedom card in that area which I use how I can. I did decide to avoid the Chase SR gave so far.

Yeah, right. ![]()

That’s the way it should be, but that negative feedback usually gets so twisted that by the time it makes it to someone high up (if it ever does), it will say how much the customers like the new colorful website and how moving the menus from the top of the page to the side of page means they will have a better “experience” - another buzzword that I can live without - and how they are more likely to think BigCorp cares how they feel. . // rant off

This is very likely why AMEX capped the BCP at $6k/yr. There are many grocery stores selling gift cards, some have them have a money order counter at the service desk. Kinda one-stop MSing and they did not like giving 6% without cap.

I’m surprised more cashback cards are not doing this but it’s tricky to implement for the travel cards due to customer profiles and type of expenses (larger).

i remember the days of uncapped BP cards. Oct 14 2014 was the date we were closed out… But they are honorable people. They closed the cards (bcash 5% in g/g/d/ uncapped) but paid my rewards of close to 2k I had left. Some folks had 10K paid out.Then 6 months later they allowed the closed folks to apply for the new BCash card with 5% (referred to as OBC) BUT capped at 55600. But only 50k is 5%. So you can still get about 2k after gc fees and MO fees. AND you can have more then one card…unfortunately no longer available. Dont know if this portends the shutdown of the new OBC cards, but its been unavailable for applications for a while.

also dont know why folks here have trouble with the amt spent on the BCP. All you have to do is go to Statements/and input date of 1/1/18 and then todays date. it gives you up to the minute spend on the card. Also works on OBC cards so you know when you hit the 56500 spend. Simple

1 Like

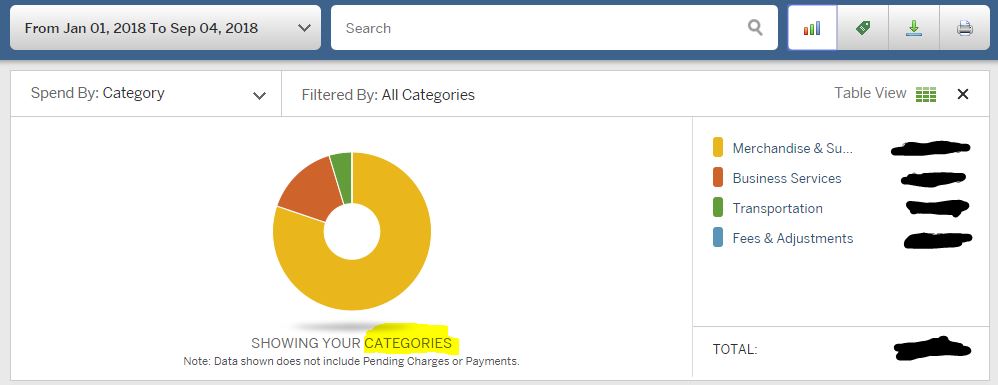

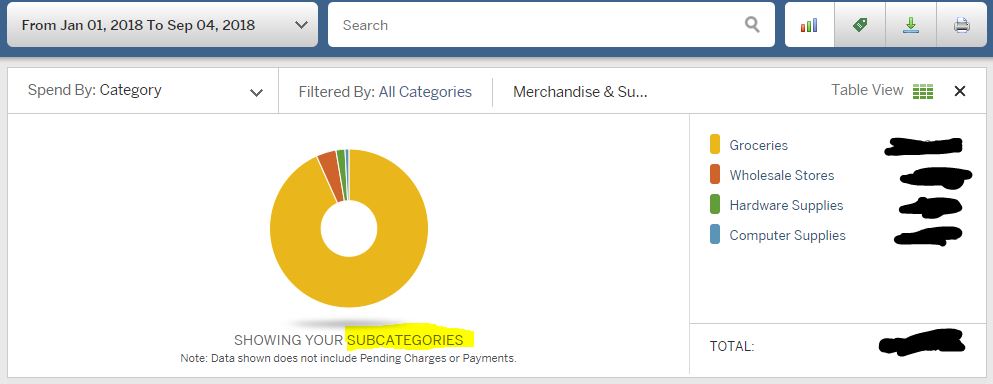

Because not all spending may be at the 6% level. Trying to figure out how much is specifically under Groceries is a pain in a … You can drill down to categories under transaction history, but 1) it takes lots of clicks, and more importantly, 2) those categories do not match up with how categories are assigned for the rewards purpose (!!!)

The categories don’t match up. But if you then click on the Merchandise category, you see the Groceries subcategory.

And sometimes transaction will fall under Groceries there, but won’t get you 6%, and vice versa. I’ve been through this with customer service.

1 Like

ok. I just use it exclusively for groceries…so its easy. Didnt consider that.

As have I, which led me to …

I now know which grocers are considered grocers by Amex and those are the only places that I use the Amex. In fact, my wife doesn’t even carry the card with her until Friday (her shopping day) rolls around.