I hesitate to ask… but should we discuss Bilt 2.0 here? Buckle up for the most confusing system I’ve ever seen in 25 years of being in this game.

In simplest terms, they have three new cards:

- Blue

- 1x on everything

- 4% back in “Bilt Cash”

- $0 AF

- Obsidian

- 3x on choice of dining or groceries (groceries specifically has a $25k/yr cap)

- 2x on travel

- 1x on everything else

- 4% back in Bilt cash, $50 semi-annual hotel credits.

- $95 AF, $50 AU fee

- Palladium

- 2x on evertyhing

- 4% back in Bilt cash, $200 semi-annual hotel credits.

- $200 annual Bilt cash credit

- Priority Pass

- $495 AF, $95 AU fee (who also gets a priority pass)

There are also SUBs but I won’t get into those because that’s not the interesting thing. The Bilt Cash is the thing worthy of discussion.

Bilt cash can be used one of two ways:

-

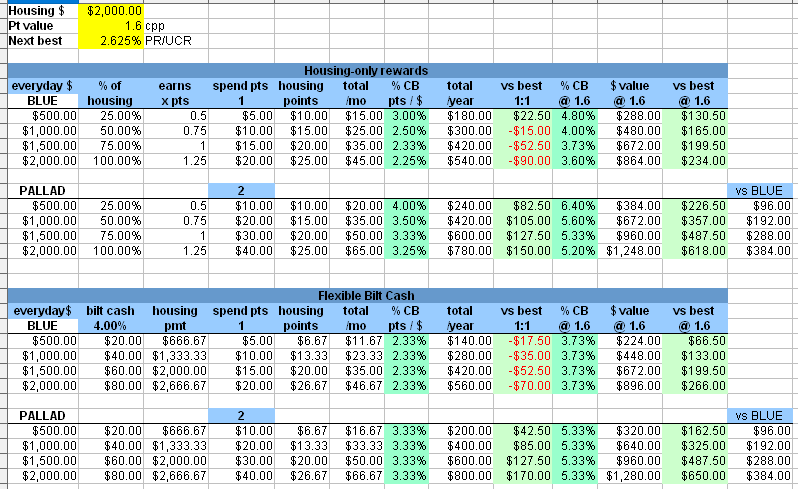

You can spend it to earn Bilt points by paying your mortgage or rent through Bilt. They give you a routing and virtual account number that, when drawn on, will pull money from a linked bank account. To get 1x on your entire rent or mortgage, you must pay a fee of 3% of your total mortgage or rent. Bilt Cash (or actual cash) can be used to pay this fee. You can optionally earn less than 1x if you just want to spend whatever Bilt Cash you have, at which point you’ll earn some proportional number of points to the amount of Bilt cash you would have normally needed.

E.g.: To earn 1x on $1k in rent, you must pay a 3% fee or $30. You can use Bilt Cash to pay this fee. Or, you can pay any combination of actual cash and Bilt Cash to get the full 1x. Or, let’s say you have $15 in Bilt Cash - you could spend all of that and choose to earn .5x points back on your mortgage.

-

OR, you can use Bilt Cash to purchase coupons for use in their ecosystem. The most interesting things to me here looked like $100 Bilt Cash for a $100 hotel travel portal credit, $200 Bilt Cash to increase all your multipliers on spend above by 1x up to $5k in spend (so palladium for instance becomes 3x on everything), or $10 at Walgreens.

Confused yet? Well, there’s yet another option. You can forego the Bilt Cash stuff and just earn mortgage or rent rewards according to this formula. Instead of the above you can earn:

-

Points on Housing Minimum everyday spend as a % of monthly rent / mortgage (Example of $2,000 rent) 0.5x points Spend at least 25% of monthly rent ($500) 0.75x points Spend at least 50% of monthly rent ($1,000) 1x points Spend at least 75% of monthly rent ($1,500) 1.25x points Spend the same or more as your monthly rent ($2,000

I did apply for the palladium and was approved. My primary reasons for going down this rabbit hole are (a) I’m in the PNW so Alaska points (which transfer 1:1 from Bilt) are valuable to me, (b) I’m a Hyatt Globalist and they also transfer 1:1 from Bilt, and (c) I have a lot of non-category spend that could benefit from 2x Hyatt or Alaska.

If anyone can explain this better than I can, I’m all ears… I think for most folks it is a pass unless you place high value on their specific transfer partners.