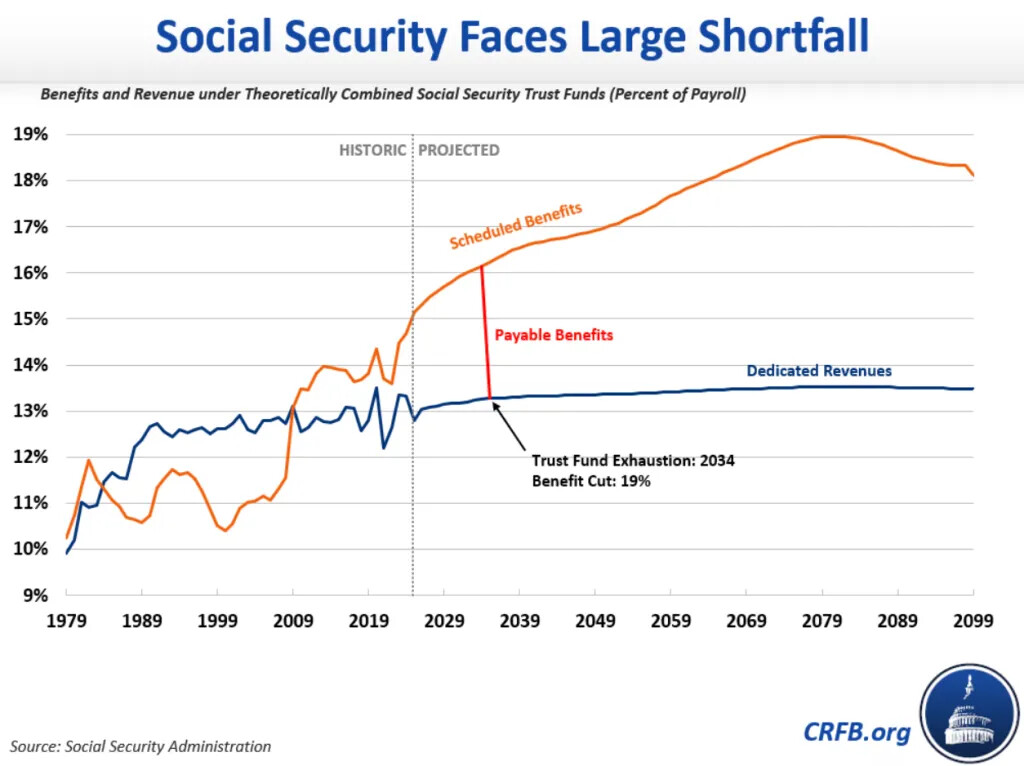

It definitely sucks. They fixed a lot of it in the inflation reduction act but it expires this year.

The bill passed, so the benefits cliff gets reinstated starting in 2026.

There were a bunch of other random technical changes that makes it harder to signup, auto renew, or prove income.

This takes food off of my table, but I’m hardly the poster boy for pain on this as an early retiree.

Good summary at kff.org.

2 Likes

That was before passage of the OBBBA right?

I’ve read that because taxes on social security benefits (set to decrease from extra tax deduction) usually add to the trust fund revenues, the trust fund is now expected to be depleted in 2032 or 2033 depending if combined with disability trust fund or not. Either way, it sounded like OBBBA shaved about 1 year off the Trust Fund solvency.

2 Likes

Go for the white and Asian doctors from the new crop, but you probably just want some older doctor from back when they taught medicine full-time instead of diversity training in med schools.

It’s been two years since the Supreme Court banned racial discrimination in college admissions. Nonetheless, at medical schools, evidence suggests that the discrimination continues.

Accepted black applicants had lower average MCAT scores than accepted white or Asian students at all but one school, Carle Illinois College of Medicine. Thirteen schools accepted black students with average MCAT scores lower than the score of the average rejected Asian or white applicant. That suggests black applicants receive significant preferential treatment.

In fact, at two schools—Eastern Virginia Medical School and the University of Wisconsin School of Medicine and Public Health—black applicants were about ten times likelier to be accepted than were Asian and white applicants with similar grades and test scores. And Asian students face a conspicuously difficult road to acceptance, despite significantly better credentials on average

2 Likes

Medical cost inflation looking like ~10% for next year’s insurance proposals.

Consumers who don’t qualify for government subsidies to buy health coverage on the Affordable Care Act exchanges could face double-digit premium increases for next year, according to early filings from insurers.

Workers with employer health coverage could also have to pay higher premium and out-of-pocket costs next year.

Large employers are projecting their overall health coverage costs will rise an average of 9% in 2026, according to several business group surveys, which would be the highest level of health-care inflation since 2010.

2 Likes

Insurers should just exclude any coverage for GLP-1 for non-diabetes purposes. Let people with unhealthy lifestyle pay for their diet pills out of pocket instead of increasing everyone’s premiums.

I guess, but the costs are coming down and the long term health effects of losing 30-50lbs are so good for heart disease, diabetes, new evidence for reduced additive behaviors like drinking and smoking, etc, the insurers might want to pay anyway (assuming they’re insuring that person for the long term).

3 Likes

I imagine it’s a matter of price. These drugs will eventually be generic and much cheaper.

It’s pretty expensive to be overweight over the long-term.

2 Likes

Thanks Trump!

I listened to a podcast on the subject, I think this one. IIRC, basically when GLP-1 hit the market, there was such a high demand which led to crazy shortages that the copyright-holding manufacturers could not meet the demand, and due to some existing law, pharmaceutical labs were allowed to create and sell the identical “knock-offs” without violating the copyright. And IIRC, once it had been allowed, it’s not being disallowed (or maybe the laws aren’t being followed by foreign labs), and it’s still possible to get the same drug without the brand on it for much cheaper.

1 Like

I’m not convinced that the improvements in health outcomes outweigh the cost of these $15k/yr/person prescriptions. Otherwise, on-aggregate, why are all insurers seeing skyrocketing costs that they have no option but pass on in premiums? I mean if the lower health expenses from healthier patients made up for the costs of these diet prescriptions, that’d not make sense.

losing weight lowers future costs, but not current costs so much.

These drugs are new enough the long term health benefits havent started to be realized yet.

And, maybe costs would be skyrocketing even more without these drugs? Rising costs could have premiums going up 25%, but these drugs are reducing costs so that they are only going up 10%?

This is the type of short-sighted, quarter-to-quarter thinking that is an absolute malady in our financial system.

Isn’t it early to make that claim? Like some highlighted, there’s no data yet on long-term benefits/harm because the drugs are still too new. We’re still dealing with aftermath of an opiod crisis fueled by big pharma push to hand out drugs that turn out to not be that beneficial to the public. For the sake of not repeating that fiasco, would it not be prudent to not lock in losses (increased drug costs) until data supporting gains (long term health benefits and cost savings) becomes available?

Personally, I don’t want to subsidize unhealthy lifestyles by paying higher premiums. I think people who choose to live unhealthy lifestyles should pay for that choice, not socialize the burden on society that comes with their choice. And if insurers want to pay less expensive claims so they make more money, fine. I don’t mind them profiting from the potential future cost reduction. But do so as an investment of their money instead of mine. More so when the (health and financial) benefits are far from proven to be realized at this point in time.

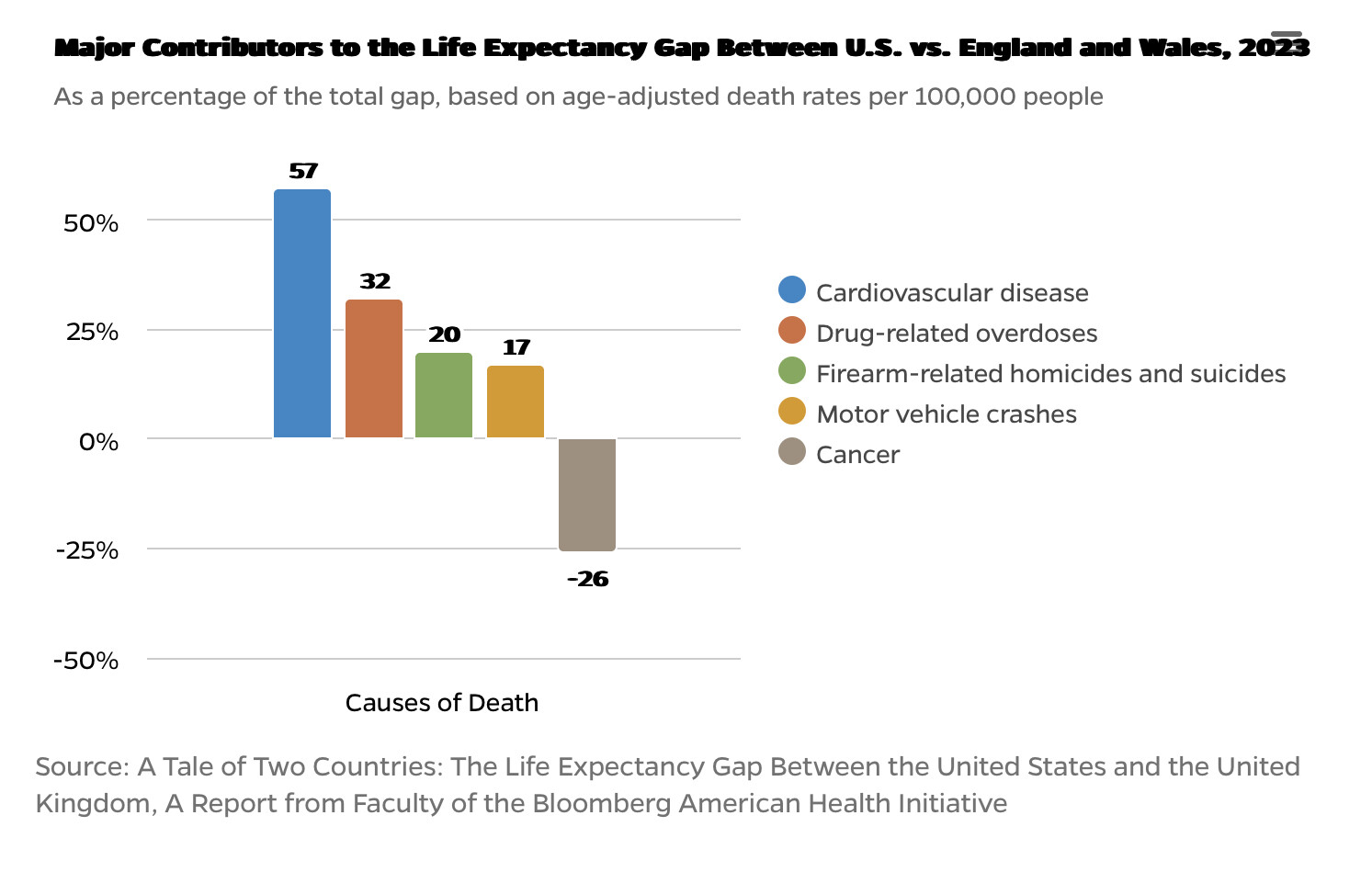

US has by far largest healthcare spending per capita in the world despite having shockingly lower life expectancy (by ~4 years) than every other developed country (ref). So allow me to remain skeptical of big pharma pushing to socialize the costs of yet another expensive “advance” in healthcare considering this track record.

The differences are not due to medical care. The reforms being put in place by HHS secretary Kennedy may have some effect on heart dsease but the other factors except cancer. would not be affected no matter how much money we spend. The lower cancer rate may be due to the wider availability of cancer radiation therapy and advanced diagnostic imaging like ct scanners.

t

1 Like

Another big factor is the EU defines premature births as miscarriages several weeks earlier than the US does, so when some of these very premature babies die, they count as a “zero” for US life expectancy and don’t count at all for the EU. Due to US differential demographics, we have more premature births as well.

If you look at the health care outcomes conditional on a problem (ie how long do you live if you get this type of cancer, or after a heart attack), it’s definitely better results for the US population. We just have unhealthy lifestyles and had more of these problems due to weight, diet, lack of exercise, etc.

1 Like

I don’t see how massive socialized spending on medicating said unhealthy lifestyle will help close that gap. Especially when you look at the second cause of this longevity gap which is drug overdoses. Something directly promoted by over-prescription of opioid drugs pushed by big pharma starting in the 90s. Given this track record why should we then sponsor getting people on a lifetime of GLP-1 drugs with unknown long-term side effects and at unmanageable costs?

Second exhibit is why should insurers and the public pay for something Medicare won’t cover? Trump wisely nixed Biden’s administration plans to have Medicare cover it. Mainly from looking at the CBO report of Oct 2024 which figured that the cost to Medicare would be $35B to extend coverage to weight loss with minimal cost savings ($3.4B) in return from 2026-2034 (CBO report). Even adding another decade for uncertain health benefits to turn into savings, the CBO estimated that it’d still be an extra drag on the Federal budget.

Just let those who decide to continue with unhealthy lifestyles cover the costs of their choice out of pocket, then wait a decade or two for long-term benefits to be better measured (and avoid another opioid-like debacle) and for generics to become available to make the coverage more affordable if need be.