“Unretirement,” or the act of going back to work after retiring, isn’t just for young Buccs like Tom Brady.

John Tarnoff, a reinvention career coach based in L.A., says unretirement is an underreported phenomenon that has been going on for years.

“The costs of living were going up even before the current inflationary cycle that we’re in now — costs were rising, fixed incomes were no longer good for people, Social Security as an institution is under threat,” says Tarnoff.

“Retirement is a misnomer — there is no more retirement,” says Tarnoff. “I think that older workers are going to be caught in a tight squeeze, because they don’t have the income overall to keep up with inflation.”

Sure, keep withdrawing all your earnings every year and maintaining the same nominal principal (not principle, by the way). In eight years, at 8% inflation, your principal will have half the purchasing power it has today. In 15 years, it will have a quarter of the purchasing power. Typical retirement is 30-35 years, more if one were to retire early.

Real vs nominal prices and asset values have not mattered in some 40-45 years, but anyone who was around in the 70s knows how devastating it can be when you have high inflation. I have witnessed elderly folks from my parents generation literally run out of money because the nominal assets they had accumulated before retiring had completely lost all purchasing power.

I recall a time when a 60k salary was considered good and bay area house prices at 700k were considered high, a million meant something back then. Nowadays kids out of college make 200k in Tech, Bay area house prices are at 3-4 million and 10 million is the new million. And that was with benign inflation in the last 3 or so decades, not at anything like 8% per year.

The only thing that matters is “inflation adjusted” principal/prices/assets/incomes. Nominal means nothing.

This I agree with wholeheartedly! The financial planning industry has lined their pockets with our money by giving this type of false sense of security which has completely destroyed thrift and savings habits.

And as long as the earnings keep paying the bills, why would you care? It’s no different than a dividend stock held for cashflow - whether the share price goes up to $80 or it falls to $20, you keep collecting that $3 dividend either way.

As I said, your heirs might think differently, but maximizing the value of the inheritance you leave is a different subject altogether.

Yes, I understand what you are trying to imply, that after 30 years you might need your principle to earn 80% annually to earn enough to keep paying those ever-inflating bills. But that ignores the fact that you only need your earnings to increase by that inflation number to continue paying your bills. And as was illustrated, a 300% increase in earnings can absorb an awful lot of years of 8% inflation… At least in my mind, spending every penny of what your principle earns only means you dont have enough principle to retire in the first place. A cushion for increasing or changing expenses over time needs to be included in that budget.

Didn’t the Trinity study, where the 4% rule of thumb came from, suggest 4% at start and increasing annually with inflation? Not 4% of the current balance, which would naturally have you spending less in down markets and more in good ones?

And wouldn’t one spend a little more aggressively if they wished to die broke?

yes its inflation adjusted 4% of the starting balance

Also its not meant to retain 100% of principle. not at all. Maybe I’m wrong but I think some people are assuming that you’re supposed to keep principal for some reason. The 4% rule idea is just to not outlive your money. Spending principal is expected by its design.

…and it’s that design that has left retirees feeling like they can no longer afford to remain retired. Drawing down the principle regardless of earnings is hoping for the best, only spending the earnings ensures you will remain financially secure indefinitely.

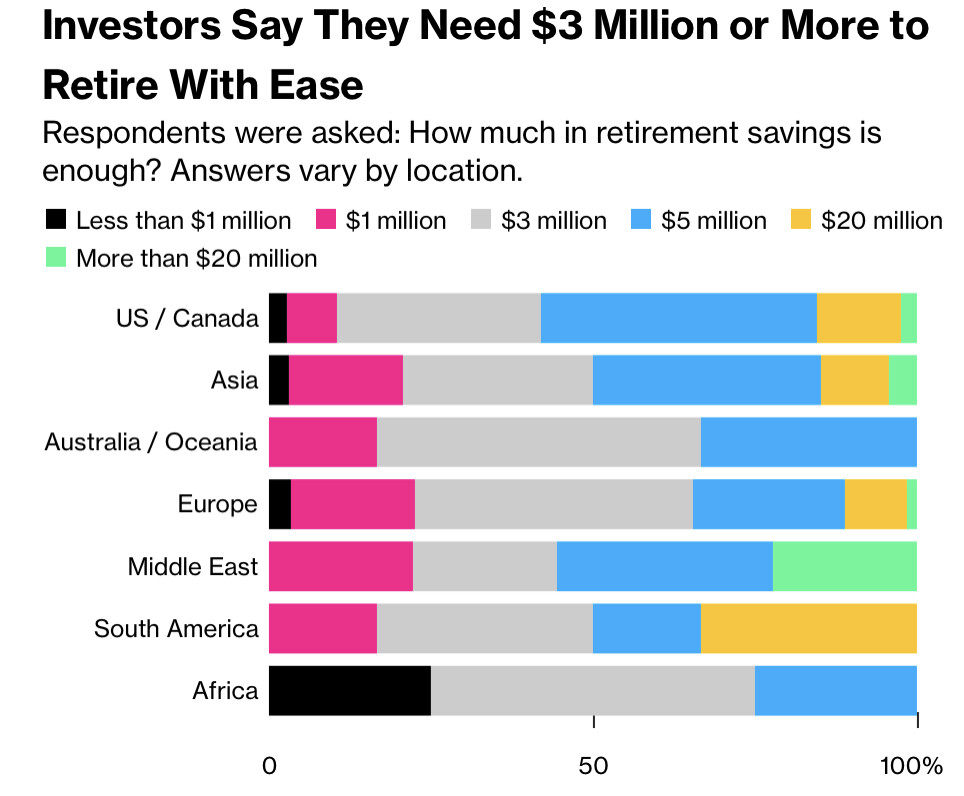

Not surprisingly, American workers were most worried about inflation shrinking their assets in retirement. The second most-feared scenario is becoming a reality, at least right now – 53% of respondents fear “a major market downturn significantly reducing assets.”

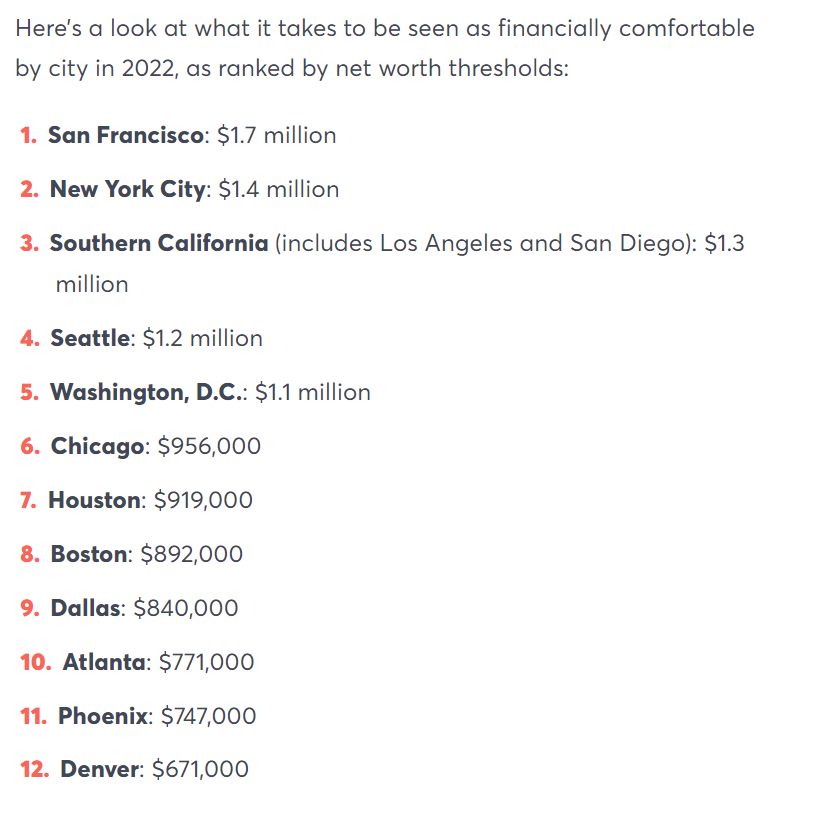

They " examined 12 of the biggest metropolitan areas"

Its not the 12 most expensive. They seem to have grabbed a dozen cities out of the top 20 or something. Not sure what the point is…

For the most part real estate cost is what dictates COL.

Portland OR is clearly more expensive than Atlanta. At this point Boise is more expensive than Atlanta too.

Sadly, I’ve almost accepted it as a part of sacrificing, living within our means, and saving during our working lives. With my RMD, SS (for idiots, not a Nazi, German, or Chinese reference) is taxed to the point that it is worth less than the rise in my BP when I think about it.

LoL. That’s not enough people and certainly not a wide enough net to draw any conclusions. Being “investors” already puts them in a higher income/savings category. You could easily find a place to retire pretty much anywhere for less, especially outside of the US (healthcare and housing is too expensive).

The chart should be compared with the respondents’ current income and net worth. I bet there’s a correlation.