The current 6 month block of inflation for I bonds is at 6.9% annual and that’s with one month to go.

So buying before April ends will get 7.1% for 6 months and then 6.9%+ for the following (both annualized). I’m probably going to buy this time.

The current 6 month block of inflation for I bonds is at 6.9% annual and that’s with one month to go.

So buying before April ends will get 7.1% for 6 months and then 6.9%+ for the following (both annualized). I’m probably going to buy this time.

I’m currently maxed out. Have zero regrets. Feel very fortunate to have gotten in.

Where else you gonna be able to get ≈7% on government insured paper?

For at least a year and with no state tax!

Do you have a trusted companion you could give $10k, so they can but you a bond as a gift? They then distribute it to you Jan 1, and you get all the benefit of a 2023 purchase, but also score 12 months of 2022 high rates (and you wont have to wait until 2024 to be able to sell).

Even “Ken” got caught up in the problem of having to update his linked bank account in the outdated way required by the website. See NYT article at: Government Site for Buying Savings Bonds Shows Its Age - The New York Times

which states:

"Ken Tumin, founder of the consumer banking website DepositAccounts.com and a close watcher of I bonds, said he was in the same situation: His TreasuryDirect account is linked to a bank account he no longer uses. He said he planned to visit his bank “soon” to have the form signed and update the account. The paper process may help thwart hackers, he said, but “it’s important to link your TreasuryDirect account to a bank account that you plan to keep and maintain for the long term.”

Excellent post. Thank you KCK. I did not know!!

Also in my earlier, most recent, post above:

While I mentioned state tax I failed to mention, for us older folks, the help I bonds offer where the hated, dreaded, IRMAA is concerned.

As Tony the Tiger would say, "I bonds are “GRRRRR-ATE!”

i hear ya. it’s like the feel of crisp bills. but no worries of theft or loss either right?

Agreed. Good point.

So now that I’m doing taxes, how do I report my child’s interest income annually? I see there’s form 8814 (parents’ election to report child’s interest and dividends), but it won’t be automatically filed (I added the data, but the software didn’t mark the form for filing) if the interest income is < $1100. I got 10K in August, so with the 3-mo penalty included, the interest for 2021 is $28. I got another 10K in Jan, so the interest for 2022 will be > 1100.

I want to elect the annual reporting method to minimize taxes, but what am I supposed to do if some years that annual interest income is below the reporting requirement?

Just fill it out… ![]()

You’ll want to find the details - I dont remember if they were linked here (by Xerty?), or if I read a section in the Treasury Direct FAQ. But basically you file a 1040 for your child, listing the interest earnings for 2021. And include a statement/declaration that you (the child) want to claim bond interest annually (getting this declaration on file is the only reason a return is needed for this year).

Then, as long as the annual earning is under $1100, you need not do anything in subsequent years (until a bond is redeemed and the resulting 1099 needs to be addressed). If their income exceeds $1100, you’ll need to file a return for them for that year, paying tax accordingly. Their unearned income has to exceed $2200 before form 8814 potentially comes into play. Form 8615 is relevant to the subject as well.

Not intended to be tax advice, this is just my personal understanding of the situation.

FYI - I’d also consider claiming the full 2021 interest earned, not the net after backing out the redemption penalty. You may or may not ever end up paying that penalty, it certainly wasnt paid in 2021. And even then, for 2 months (5 months less 3 month penalty) a $10k bond should’ve earned more than $28.

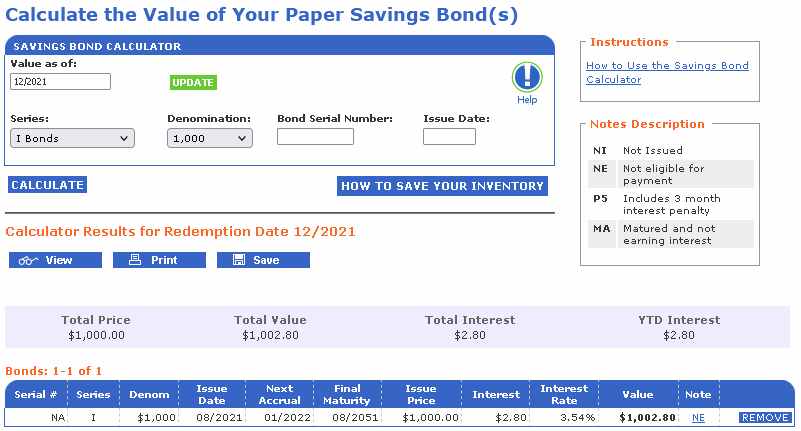

The interest rate before Nov 1 was 3.54%. I used the online calculator:

Indeed, it was right below my original question (here). I missed it last night.

Apparently I can switch to annual interest income reporting at any time. So I could skip reporting for 2021 and just report 2021+2022 earnings on the 2022 return (and every year thereafter):

I don’t see any way to attach any statements using the software (H&R Block), which means I have to write it up and print separately and can’t e-file, right?

I’m not familiar with HRB software, but I read somewhere that first time minor tax filers couldn’t e-file anyways.

Is there any guidance regarding the format or contents of the explanatory statements that get attached to a tax return? I couldn’t find anything. I’m thinking name, SSN, maybe date, signature, and the statement itself.

I just used the info they put on top of every form (name and SSN), and a short, clear statement.

If you are basing it on the redemption value, then technically the earned interest is $0, because you could not redeem the bond at all in 2021. As far as accruing interest, you’ve accrued 5 months. Think of a bank account that pays you interest at the end of the month - like the bonds, that value doesnt show in your bank account until the 1st of the following month (it posts overnight). That’s what happens with bond interest as well - you held the bond from August (per bond terms, counted as August 1) through December, which is 5 months of it earning interest. Even if that 5th month’s value doesnt show in your account until Jan 1.

Regardless, the…ambiguous…valuation tools focused on redemption value instead of accrued interest leaves some room for interpretation. But you get a “free” $1100 this year per child; I cant understand why you’d intentionally punt that interest to next year when you’re already going to exceed that $1100 threshold?

It’s a 3-page tax return (the 1040 and schedule B), plus the declaration, and should take you nearly as long to print out as it takes to prepare. Dont be afraid of it! ![]()

Because time to fill out 1040 + print + mail >> 10% of $28. Even 10% of $148 may not be worth it to me.

On the other hand… can I select the $3 to go to the Presidential Election Campaign fund on my child’s 1040? ![]()

Congrats on finally helping to fund the Liberal agenda.

I can’t ignore the obvious … uh, don’t report it?

Disclaimer, there weren’t reporting requirements for when I had kids under 18, or my tax acct ignored them. :=)

I got the feeling he was hung up on trying to claim his kid’s income on his return, rather than them filing their own returns. They’re independent (dependents file their own return), until it reaches a level where the parent gets dragged in to the equation (to prevent income shifting to the kid’s lower rate).

I think the requirements were the same when you had such kids, but unless you had lots of income-producing assets stashed in their names it never came into play.

I was hung up on the fact that once I elect to pay taxes on the child’s I-Bond interest annually, then I’m required to continue reporting all the interest every year. It doesn’t say that I don’t have to report if it’s below the filing requirement. Otherwise, once I sell the Bonds and receive the 1099-INT, how will they know that I already reported all that interest and paid all applicable taxes?

That’s in the FAQ somewhere, too. You list the 1099 interest, then a second “adjustment for interest already claimed” line to net the correct interest income for that year. Or something close to that.

I found the instructions in pub 550: U.S. savings bond interest previously reported.

It just describes how to make the 1099-INT adjustment. My curiosity was in how the IRS would ever know that I claimed interest every year or how much I claimed, if I didn’t file in some years because the interest was below the filing requirement. I think the only way they would truly know is if I filed a return every single year for my child and supplied the claimed interest numbers, even in years when his income was below the filing requirement.

The key words I’m questioning are: “previously reported”. How could it be considered previously reported if it was not reported due to being below reporting requirements?

They know you claimed it because you stated you were claiming it annually. Beyond that, interest earned each year can be easily verified, and they know you reported it just like anything else not reported by someone else on a 1099 - in other words, they don’t. The possibility of being audited, where you’ll have to show your calculations, is what keeps you honest.

If you only earned $8k on a w-2 last year (and had no other income), would you say you didn’t claim that income because you weren’t required to file a return?