Thanks, xerty.

Seems like the problem might (or might not) be related to use of TurboTax. I have never used TT and have no plans ever to use it.

Thanks, xerty.

Seems like the problem might (or might not) be related to use of TurboTax. I have never used TT and have no plans ever to use it.

Inflation forecasts are worth no more than what you pay for them, but if you’re thinking about whether to buy your 2025 I bond allocation and front load it vs 3 year treasuries or something, it might be worth considering the ballpark people are thinking about for future inflation.

I have decided to buy my 2023 allocation by the end of the month. Still thinking about 2024.

seems to suggest that front loading at least 2 years worth of gifts is probably a decent idea if you can afford to have the funds completely illiquid during that time.

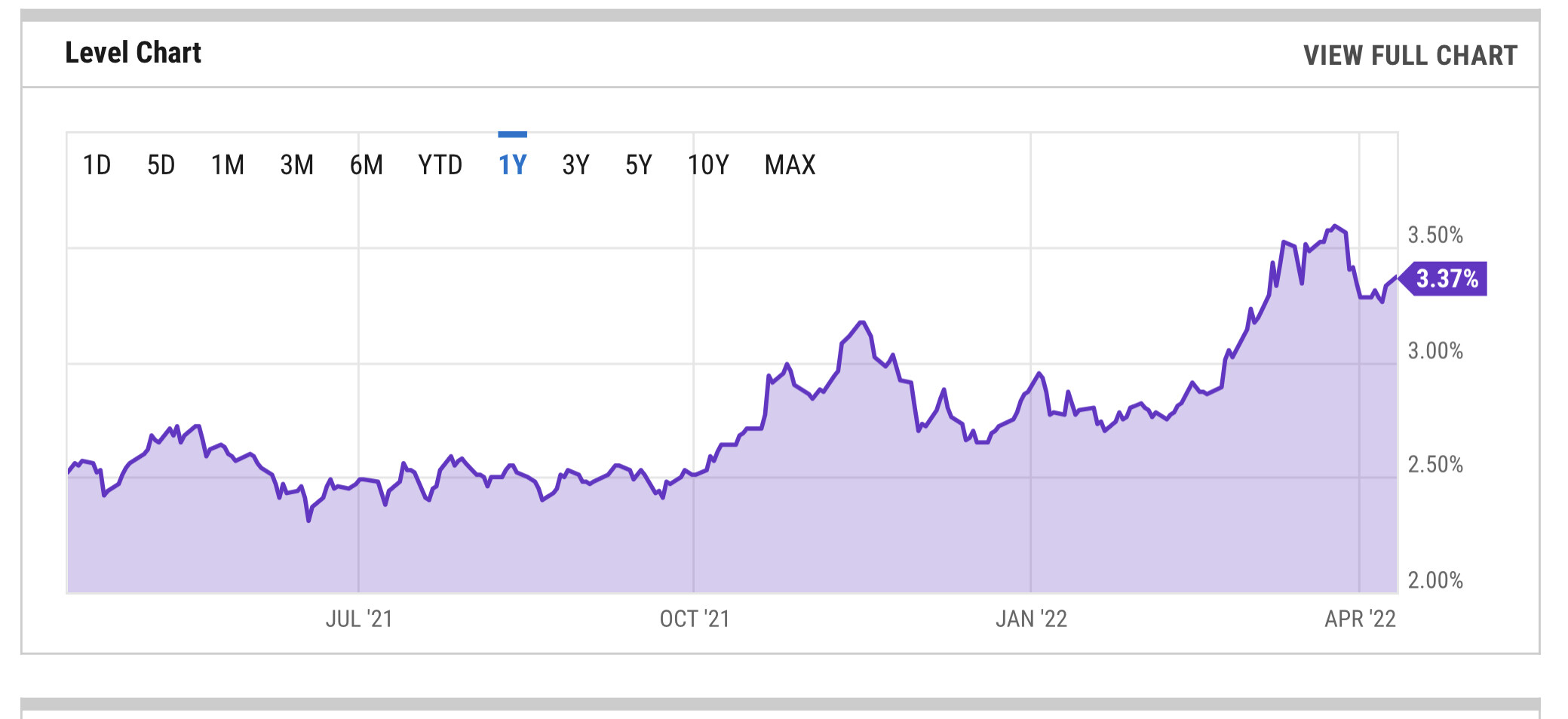

Two more perspectives on the market expectations of inflation. There are TIPS which pay inflation protection and no limit on buying (and pay much less). From their yields and the same maturity treasuries, you can subtract to find the market expectations for inflation, ie the average over that time to maturity. Here are the graphs for 5 and 10 year inflation expectations currently -

This is the 5 year breakeven chart. As you can see over the last year, inflation expectations have been rising in recent months.

5 year is predicting around 3.25-3.50%, while 10 year is more like 2.75-3%. Obviously the average is falling from 5->10 year horizon, implying the first 5 years would be say 3.5% and then the next 5 might be 2.5% to come out to a 3% average for the whole 10 year period. This is just the math way of saying the market thinks inflation is high now and will gradually decline to a more normal level as time goes by.

5 years is an interesting timeframe since that’s when you earn some extra on I bonds since the 3 month penalty goes away. Also, since you’re buying in April, the first year of inflation is know (and past) and the next 4 future years are the ones that matter for your payments. If you figure 3.5% for the next 4 year average, picking a higher end of the 5 year TIPS breakeven range since we only want 4 years and inflation is predicted to be falling broadly, you would earn (7.1+9.6)/2 = 8.4% (for sure) for the first year and then 3.5% (maybe) for the next 4, leading to an average of 4.5%. This is in contrast to top bank 5 year CDs paying 1.5-2% and treasuries paying 2.6%.

If you crunch the numbers for shorter times, you lose a bit of the interest to the 3 month penalty, which matters more the shorter you hold. You lose 20% of your interest rate holding 15 months (to get the known 12 good months and then give up the next unknown 3 months), so that headline 8.4% is really only 6.75% or so. That 20% factor drops as time goes on, so at 27 months (2 years of interest, then give up 3 months), it’s 11% etc.

At least that’s what they are currently paying. One would imagine the CD yields and treasuries are likely to inch up too as Feds raise interest rates.

That makes the decision on how much to front load I-bonds more difficult. Front loading 2023 seems like a no brainer. Whatever the Fed does, inflation is not going decrease that quickly (just like it did not happen overnight) especially with no end in sight to the Ukraine invasion-induced disruptions. 2024 is likely fine but if 5-yr expectation from 5-YR TIPS is for a return to 3%, that makes front-loading 2025 and beyond a bit more uncertain for me.

I’ve concluded that the biggest risk from buying gifts in advance is that they may increase the fixed rate portion from the current 0%.

Buying your 2024 allocation is only tying up the funds for 21 months (the gift can be delivered 1/1/24, with the one-year holding period already past so you can redeem right away). I consider it a pretty safe bet that this first year of interest will dwarf whatever lag there may potentially end up being in the rate for the last 9 months.

I think the more interesting lesson from that is:

Whale ![]()

I’ve concluded that the biggest risk from buying gifts in advance is that they may increase the fixed rate portion from the current 0%.

I would put the odds of that happening at zero, unless there is some legal mandate that requires the fixed rate to rise under some circumstances.

I seriously doubt it. I don’t know how they decide on the fixed portion, but this is probably the most popular government product right now.

Just to agree with everyone else’s replies, I think there’s absolutely no chance we see a fixed rate other than 0% on the I bonds come May 1st. Hence there’s no reason to wait to buy, unless you think 7.1% is too low but 9.6% (and the future 6 months) are good enough and will be higher than that.

You can see the history of the I bond fixed rate below - it’s been 0% ever since 2016.

https://www.treasurydirect.gov/indiv/research/indepth/ibonds/res_ibonds_iratesandterms.htm#fixed

This covers a period when the 10 year treasuries were about 2%, similar to where they are now, and ranged from 0.5-3% roughly, all the while without causing the fixed rate to change. 1 year treasury rates have ranged from 0% to mid 2% over that period, again with no impact, and like the 10 year, we’re in the middle of the historical range currently in terms of yields so no reason to think that might drive a change. Similarly, here’s the 10 year TIPS fixed rate (yield), which has ranged from -1% to +1% during the last 5 years or so:

the short term TIPS fixed rate yield is still somewhat negative for 5-10 year TIPS, so again no reason to think this merits a positive fixed rate for I bonds if they’re broadly comparable.

I agree. Guy said he overpaid on purpose to secure large profit.

First, that’s a darn large overpayment; possibly even suspicious.

Second, that’s one heck of a poor way to garner profit . . . in my opinion, of course. The smallest fee the guy could have been charged, at PAY1040, is 1.87%. There are more efficient ways to make money . . . again in my opinion, of course.

He could profit in two ways, not that I know what he was thinking. First, he could have earned 2% or higher cash back on his CC and used PAY1040, resulting in a small, positive net rebate. Second, and I think this was what he was doing, was getting paid 3% interest from the IRS for the time after his filing and until he was issued his refund. 3% isn’t bad for a short term CD, albeit one where you can’t ask for it early and don’t know if it’ll take 3 months or 12 to get paid.

^^^ good point on interest. It may also make sense if he was going for some bigger signup bonuses. For example, CapOne Venture had a $20K spend requirement for $1K bonus (plus it pays 2% cash back). CapOne Spark had a $50K spend requirement for $3K bonus (plus 2% CB). With 2 players it’s a ton, and tax payments make it really easy.

Of course you could gain a higher yield with signup bonuses that require less spend, but then you’d have to sign up for a lot more cards, and credit issuer rules like 5/24 make it difficult.

Yeah, I guess you guys are right. I didn’t think of any of that stuff because I would never personally do any of that stuff.

I agree. But I still consider it a bigger risk than regretting the interest being earned for the 21 months.

Fixed rate looks to me like it was 0.5% as recently as 2019. But before that it’s not gone over 1% since 2008 so not likely to go very high over the next 21 months.

Especially at the rate people are snapping them up right now, why would they increase the fixed rate if the I-bonds are already super popular and people front-load their purchases for multiple years?

Oops, you’re right, all those 0.xx%'s started to look the same to me. The fixed rate did pop up around end of 2018 and early 2019 when we had a high yield scare. Let me re-run my numbers in a bit.

Third, he could be generic withe the talk of “credit card”, and actually used a rewards debit card paying a flat amount per payment.

Fed comments from today. Sounds optimistic to me.

- HARKER: EXPECTS SERIES OF DELIBERATE, METHODICAL HIKES THIS YR

- HARKER SEES FED TREASURIES, MBS DEBT REDUCTION STARTING SOON

- HARKER SEES U.S. INFLATION AROUND 4% IN '22, 2% TARGET IN 2 YRS

- HARKER SEES U.S. GROWTH MODERATING TO 3%-3.5% IN 2022

If that were true, you’d see say. 4% for the first next year of inflation and then 3 years of 2%, leading to an average of (8%, 4%, 2% x3) for 3.7% average if you held to five years.