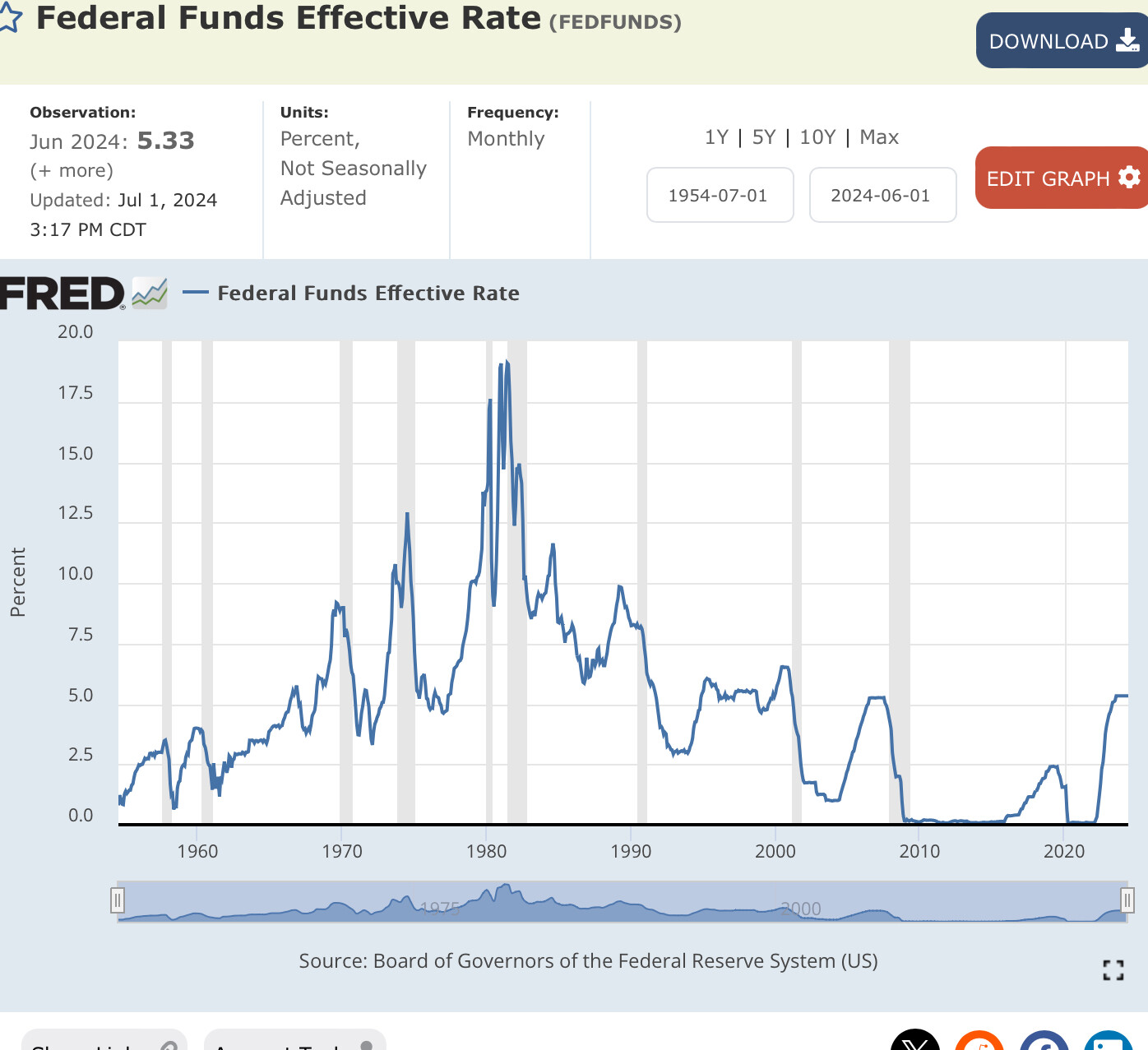

I thought it was entirely because of recent inflation and historically low unemployment. Now that inflation is down to a more reasonable rate and unemployment appears to be ticking up, they need to make sure it doesn’t turn into deflation and unemployment doesn’t go too high.

The economy did well with no deflation or high unemployment during the 1990s when there was an extended period of rates above 5%. Conversely, there was high unemployment and stock market and housing price deflation during the 2008 to 2016 period when rates were essentially zero. Today there is low unemployment and no sign of deflation with housing prices and the stock market at all-time highs.

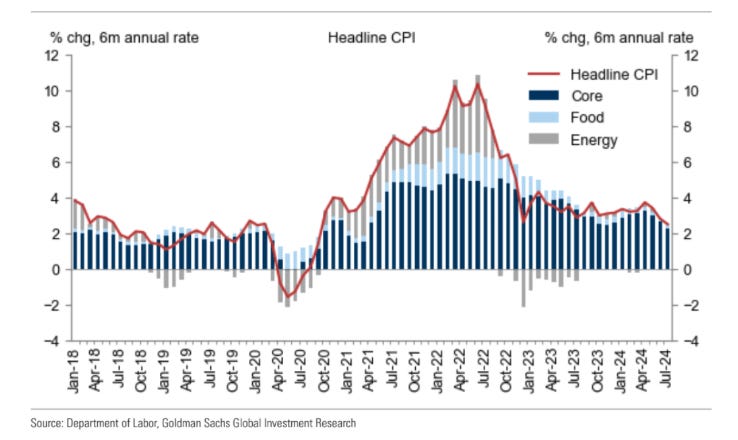

A lot of the decrease in the rate of increase of the CPI is the price of oil dropping. But with the SPR near empty, the war in the Middle East heating up and unrest over the stolen election in Venezuela, oil prices may be going up.

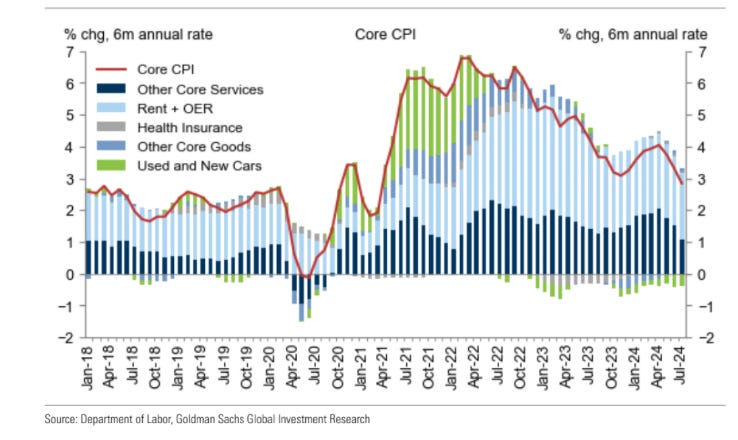

The large contribution of shelter prices to CPI has been a constant feature in the past few months. Again this last month it represented 90% of that +0.2% monthly CPI. Probably not gonna stop soon but if it did, Fed might get much closer to their 2% inflation target.

Surprise surprise the bureaucrats at the BLS have been cooking the books

The Bureau of Labor Statistics revised down its total tally of jobs created in March by 818,000 as part of its preliminary annual benchmark review of payroll data.

It marks the largest downward revision since 2009, and suggests the labor market began losing steam earlier than initially thought.

“The labor market appears weaker than originally reported,” said Jeffrey Roach, chief economist at LPL Financial. “A deteriorating labor market will allow the Fed to highlight both sides of the dual mandate and investors should expect the Fed to prepare markets for a cut at the September meeting.”

The revised data is mostly derived from state unemployment tax records that employers are required to file. The figure may be updated when the government releases the final figure in February 2025.

FED MINUTES: ALL PARTICIPANTS SUPPORTED MAINTAINING POLICY RATE IN CURRENT RANGE.

FED MINUTES: THE MAJORITY OF PARTICIPANTS SAID RISKS TO EMPLOYMENT GOAL HAD INCREASED; MANY NOTED RISKS TO INFLATION GOAL HAD DECREASED.

FED MINUTES: PARTICIPANTS VIEWED THE INCOMING DATA AS ENHANCING THEIR CONFIDENCE THAT INFLATION WAS MOVING TOWARD 2% OBJECTIVE.

FED MINUTES: THE FED STAFF’S OUTLOOK FOR ECONOMIC GROWTH IN THE SECOND HALF OF 2024 HAD BEEN MARKED DOWN LARGELY IN RESPONSE TO WEAKER-THAN-EXPECTED LABOR MARKET CONDITIONS.

FED MINUTES: SEVERAL PARTICIPANTS SAID REDUCING POLICY RESTRAINT TOO SOON OR TOO MUCH COULD RISK A REVERSAL OF PROGRESS ON INFLATION.

FED MINUTES: MANY PARTICIPANTS NOTED THAT EASING POLICY TOO LATE OR TOO LITTLE COULD UNDULY WEAKEN ECONOMIC ACTIVITY OR EMPLOYMENT.

Fed minutes point to ‘likely’ rate cut coming in September

I’ve got to admit that I expected the Fed to cave before the beginning of the year, jacking up the economy, the housing market, and the stock markets to coincide with a jacked up Joe. I also never expected them to nail a soft landing. I’m leaning toward being in errrrrr … not perfect. My gold bets are all good and my bonds are almost ready to be profitable, presuming a >25bp cut. My hat is almost off to the fed.

I think they publish these annual revisions to the benchmarks on a more or less fixed schedule.

I agree the lag is annoying but to be fair I don’t know what all is involved in gathering that data. Clearly, publishing the numbers for Q1 in April requires some kind of rough estimate based on a benchmark they hope represent the total job market. Why it was more off this time than the usual 0.1% correction is a good question. My guess is that the job market slowed down faster than anticipated in underweight sectors in their benchmark.

Alternative is a conspiracy to make the administration (or the Fed) look better 7 months before the election but not realize they’d have to revise the numbers for the worse 2 months before that election. That’d be extremely inept as far as conspiracies go knowing these updates are planned way ahead of time.

They are relying on most peoples memory being short. These are the numbers that have been publicized for the last six months by the leftist media

President Joe Biden isn’t running for reelection, but his record will still be on the ballot in the fall. Here we look at how the U.S. has performed under the Democratic president:

The economy added 15.7 million jobs. The number is now 6.3 million higher than before the pandemic.

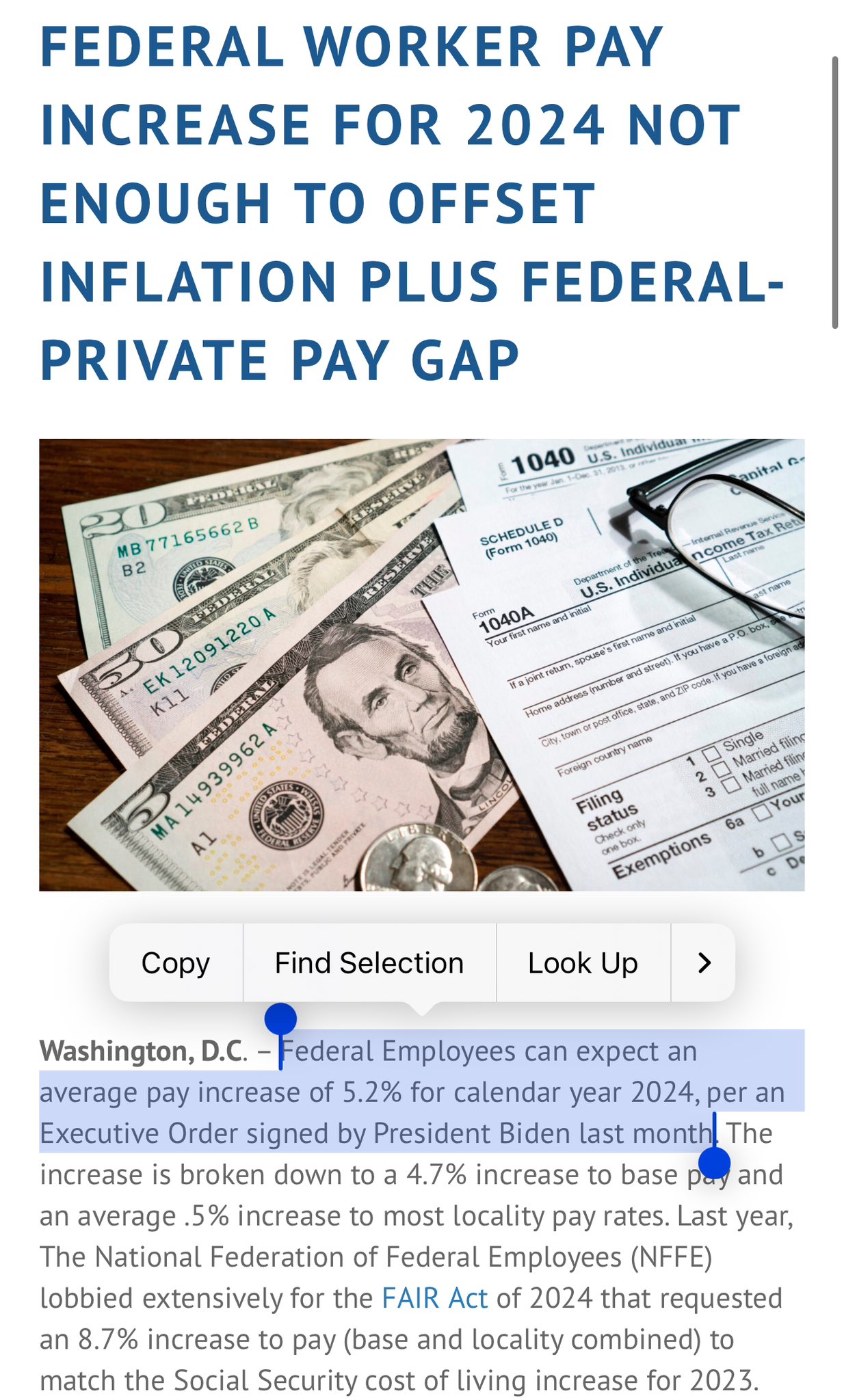

Not really what it states: only that the 5.2% raise is not enough to cover inflation PLUS the usual pay gap between public vs private sector job compensation.

But then again, the exact pay gap is kinda confusing to me. I thought that once benefits are taken into account, Federal employees were actually compensated more than private sector ones…Cato Institute 2019 report

So which is it 80% overpaid or 25% underpaid? Or did the Biden administration slash federal employee compensation by half in the last 3 years?

I have no data tables to back this up; just decades of contact with government workers (municipal, state, and federal. From that experience, the pay gap was real until sometime in the late 80’s or early 00’s. It was an acceptable pay gap for many because you gave up money for security. As the security disappeared, the pay rates rose … significantly.

Security, and perks. The previous (and original) owner of our current home was a health department bigwig, and I’m pretty sure our driveway was paved by the city when they paved the road. All other driveways on the street and in the neighborhood have a transition to an obviously different material.

Imagine if a public employee received such a perk these days? They’d be in jail for theft before the asphalt cooled.

Fed cuts 0.5%, on the higher end of expectations (vs possibly only 0.25%).

Fed went big with a 50bp cut. The dot plot implies two more 25bp cuts this year. There was one dissent by a member of the Board of Governors - the first time since 2005 and the first time in favor of tighter policy since 1994. The catalyst for the dovish move seems to be concerns about the labor market and its pace of cooling. The dot plot suggests a further 50bp of easing this year and 100bp next year, bringing the rate down to 3.375%. The median dot plot estimate of the longer run Fed Funds rate is 2.9% with a wide range.