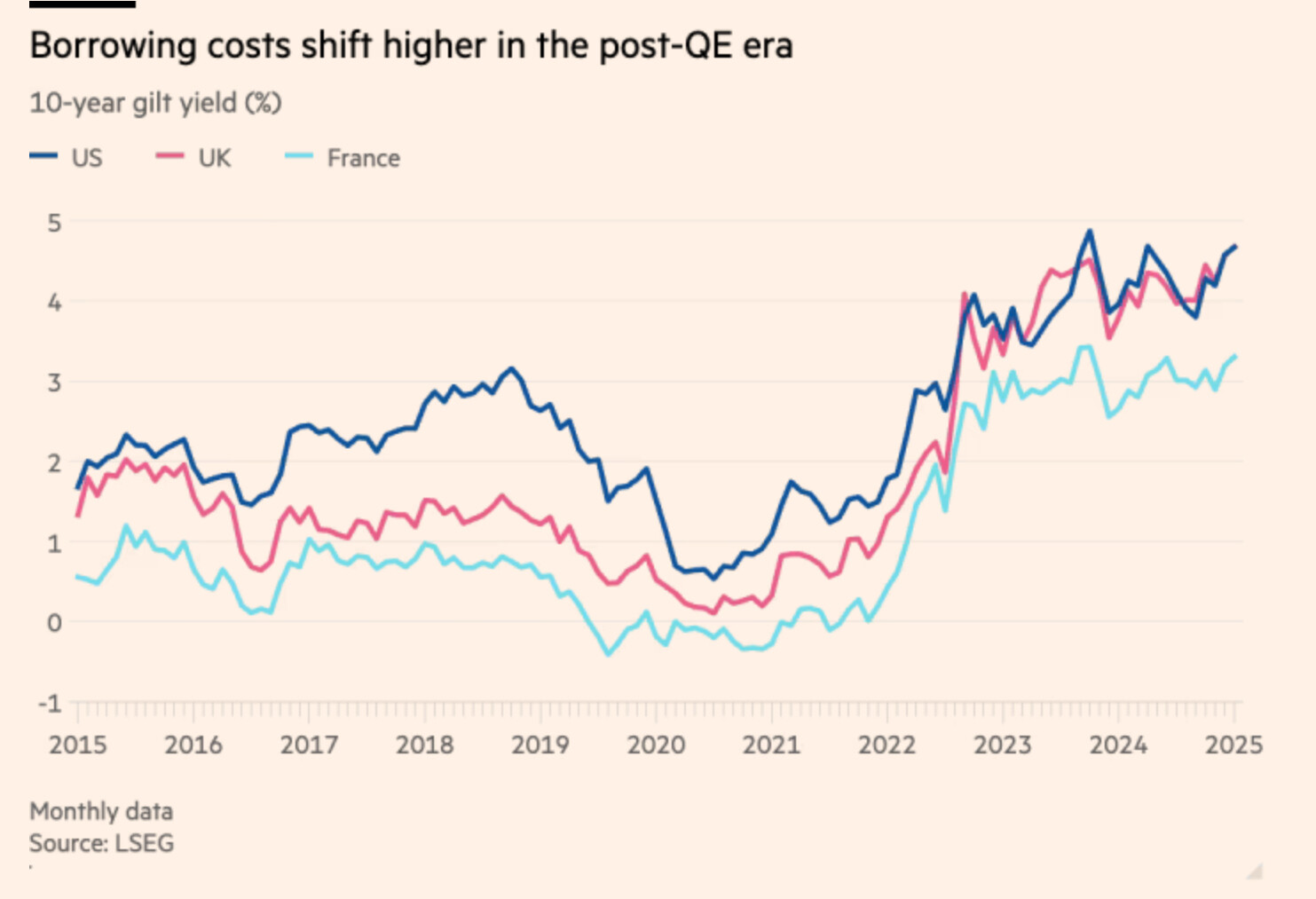

I think the Fed hopes long term rates will decrease when they lower short term rates. The 10 year rate is used to set interest rates for many types of loans so a high rate slows economic activity.

As you mentioned the Fed funds rate directly affects only short term rates. Quantitative easing where the Fed buys bonds and mortgages to affect long term rates was not used in the United States until the GFC starting in 2007. The latest round ended in 2022. These rounds lead to a huge buildup in the value of the assets held by them. At the end of the latest round, the Fed held over $6 trillion in assets.

As the assets mature they affect the money supply and cause other distortions so the Fed is reluctant to do more purchases. They are only left with a hope. The graph I posted shows it is not happening.

Are you referring to the long term debt investors, they don’t have to bid on treasuries if they don’t like the yield given our countries credit situation?

Or are you talking about the Fed - Manipulating the rates lower the way the bank of Japan has, forcing interest rates lower by being willing to buy unlimited amounts of debt to push their long term debt yield is low they want them?

If he and Vivek lotsofletters can actually drain a small portion of the swamp, that will lower 10 and 30 year rates more than Powell (who got his last shot at Trump before bailing). But that is a very tall order. The swamp is supported, and filled, by members of both parties.

Outside of 30-yr TIPS, not many I suspect. The current yields for 10+ yr bonds are way underpricing the credit/inflation risk IMO. Only treasuries I’m buying are ultra-short term (as cash basically) or TIPS. With current fiscal trajectory, anything else is too risky for me.

FED’S BARKIN: INFLATION TRENDING TOWARD 2% TARGET, JOB MARKET STABILIZED, ECONOMY REMAINS SOLID WITH NO OVERHEATING CONCERNS; NOTES BUSINESS PRICE-SETTING RETURNING TO PRE-PANDEMIC PATTERNS AND LONG RATES UNLIKELY TO INFLUENCE POLICY FOR NOW

FED’S BARKIN: I AM NOT CONCERNED ABOUT AN OVERHEATING ECONOMY RIGHT NOW, DEMAND IS SOLID BUT NOT BOOMING.

FED’S BARKIN I HAVE NOT SEEN ANYTHING IN LONG RATES THAT WOULD INFLUENCE FED POLICY AT THIS POINT.

FED’S WILLIAMS: MONETARY POLICY DATA-DEPENDENT IN UNCERTAIN ENVIRONMENT; EXPECTS DISINFLATION TO CONTINUE, GROWTH TO MODERATE TO 2%, UNEMPLOYMENT AT 4%-4.25%, AND INFLATION TO REACH 2% IN COMING YEARS; NOTES EASING HOUSING INFLATION AND SMOOTH BALANCE SHEET DRAWDOWN

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For December, the BLS set the inflation index at 315.605, an increase of 0.04% over the November number.

It is normal for non-seasonally adjusted inflation to run lower than official inflation in December. In fact, last month was the first December since 2021 to not record non-seasonally adjusted deflation for the month. The numbers will turn around in January, with non-seasonal running higher than seasonal.

For TIPS. December inflation means that principal balances for all TIPS will increase by 0.04% in February, after falling 0.05% in January. Here are the new February Inflation Indexes for all TIPS.

For I Bonds. The December report is the third of a six-month string that will determine the new variable rate, to be reset as of May 1 and eventually roll into place for all I Bonds. As of December, inflation has increased just 0.1% for the three months, translating to a variable rate of 0.2%.

However, that is pretty meaningless. Non-seasonally adjusted inflation will pick up in January. For example: In 2023, inflation for October to December was -0.34%, but the next three months brought the variable rate up to 2.96%. Here are the data:

No, they use a different index. From the tips article above,

It is normal for non-seasonally adjusted inflation to run lower than official inflation in December. In fact, last month was the first December since 2021 to not record non-seasonally adjusted deflation for the month. The numbers will turn around in January, with non-seasonal running higher than seasonal.

Coffee is one of the world’s most popular beverages. Brazil is the world’s top coffee producer, followed by Vietnam and Colombia.Ethiopia and Indonesia round out the list of top five coffee producers.