Isnt that expected? The higher wages are to keep workers, not get more out of them. And, if your goal is to narrow the wage gap between the peons and the executives, it’s inevitable since most peons arent capable of being more productive no matter how much they’re paid.

“Nonfarm productivity, a measure of output against hours worked, declined 7.5% from January through March, the biggest fall since the third quarter of 1947.”

If I’m understanding this definition correctly, productivity isn’t measured against compensation. So this isn’t about peons getting more money.

In the past, you wouldnt pay those peons more money, you’d let them leave - which improves your productivity averages (addition by subtraction). Generally speaking, a 7.5% decrease in productivity would correspond with a 7.5% decrease in labor costs, since the least productive get paid the least.

It isnt a direct cause-effect relationship, but they do go hand-in-hand. Not only are you paying more, you are paying more to retain those who produce the least.

The same difference. The higher wages have no impact on productivity. The impact might come from the more productive people jumping ship to go elsewhere, leaving the less productive people --with or without change in wages-- behind.

In other words, the odds aren’t high at present for a material softening in US inflation pressure or a significant rise in recession risk for the immediate future. As a result, the Fed will remain under pressure to aggressively raise interest rates for the foreseeable future.

Market sentiment continues to predict no less. One of many examples: the policy-sensitive 2-year Treasury yield, which in previous decades has tracked the Fed funds rate, is currently 2.66% (May 4) — far above the current 0.75%-to-1.0% Fed funds target range. The current premium on the 2-year rate over the Fed funds rate is unusually wide and implies that the central bank needs to accelerate rate hikes.

I posted this in the Ukraine too, but it’s a wide ranging 60 page article and they cover a lot of ground.

You really have to talk about the entire debt for the nation. Add in everything from a credit card to a student loan, to a municipal bond, and that number exceeds $89 trillion. That gives you a basis to understand that if interest rates are going to go up one percent—and I only mention one percent because it’s an easy number to work with—that means there’s another $890 billion of debt service, call it $900 billion for ease of calculation, in a $24 trillion economy. That’s a lot. If it were two percent, just to pick a number without predicting any particular scenario, that’s $1.8 trillion of extra debt service. I don’t think the country can handle it.

So, it’s not a sustainable system. And every day that number goes higher, so it gets worse. That’s the problem we’re in, not stagflation. The problem is a debt-burdened and debt-financed society. We’ve got to find a way out. And we’d better do it soon, otherwise we’re going to be in a for lot of inflation for a very, very long period of time.

we’re experiencing is not a momentary inflationary phenomenon that you could live through for couple months, but that this is the way it is going to be.

And why? We have structural shortages of commodities that have no possibility of being alleviated because, number one, nobody’s going to invest the capital to alleviate them. Number two, those companies, the commodity producers, can’t even obtain the capital. And, number three, even they were to, they will likely suffer an enormous amount of litigation, because a lot of people and organizations who are environmentally conscious don’t want expanded production in the extractive industries. And, number four, almost all such resource development requires licenses and permits, and these companies not going to get them from the government. So, that’s what I mean about a stenotic system. It’s not able to alter itself in its current structure. It’s just frozen in place. And that usually is a precursor of big trouble

Thanks, xerty. I was going to post that and credit you, but you posted it first. However, I think this part of your piece is also important:

Is our current condition stagflation?

Murray Stahl: Well, no. Our current condition is that as society—it’s not just an American problem; it’s a worldwide problem—societies have borrowed too much money. That’s the first problem.

The second problem is the way economic progress is measured, which is by GDP, which is a measure of consumption. Therefore, the more money you borrow, whatever it gets spent on, adds to the GDP. Stop spending that money, and GDP is going to contract. Be aware that your expenses, including your income tax expense, is somebody else’s income. That’s the thing. We’ve had a debt-financed economy since, probably, 1960. That’s basically the problem. It’s been 62 years since then and, in the long-run, it is not sustainable. We’re now at a national debt number of $30 trillion. Somehow, we’ve got to do something about it. There are not a lot of good options for changing it, but we’re going to have to learn to live with a lot less borrowing.

But that’s not the whole measure. You really have to talk . . . .

I mean, what the heck, your entire piece is a gold mine of good sense.

That writing about the second law of thermodynamics invalidating the current green movement . . . . . WOW!! While I did endure a thermo course as an undergrad . . . . let’s just say it was not my strongest subject! And that’s putting it as generously as I’m able.

Yeah, they’re quite good. As long term investors, you have to cut through the bull and actually see things as they are. You can find more of their similar comments here

They are investment managers for various funds, and while I respect their thinking, I’m not sure they’re something I’d invest in personally (but I have high standards). Their oldest Paradigm fund WWNPX has done about 4%/year better than the market, but more like twice that when they started out and in line over the past 10 years. Their small cap fund KSCOX is still doing quite well also and beat the market by about 4-5% annual for a long time.

This is hilarious. After dumping 180M barrels of oil onto the commodity markets right into midterms, they’re already telling the market they’re going to be buying it back, starting with 1/3 of it right after midterms. Bids for oil to refill the Strategic Reserve are requested for fall 2022 for delivery in early 2023.

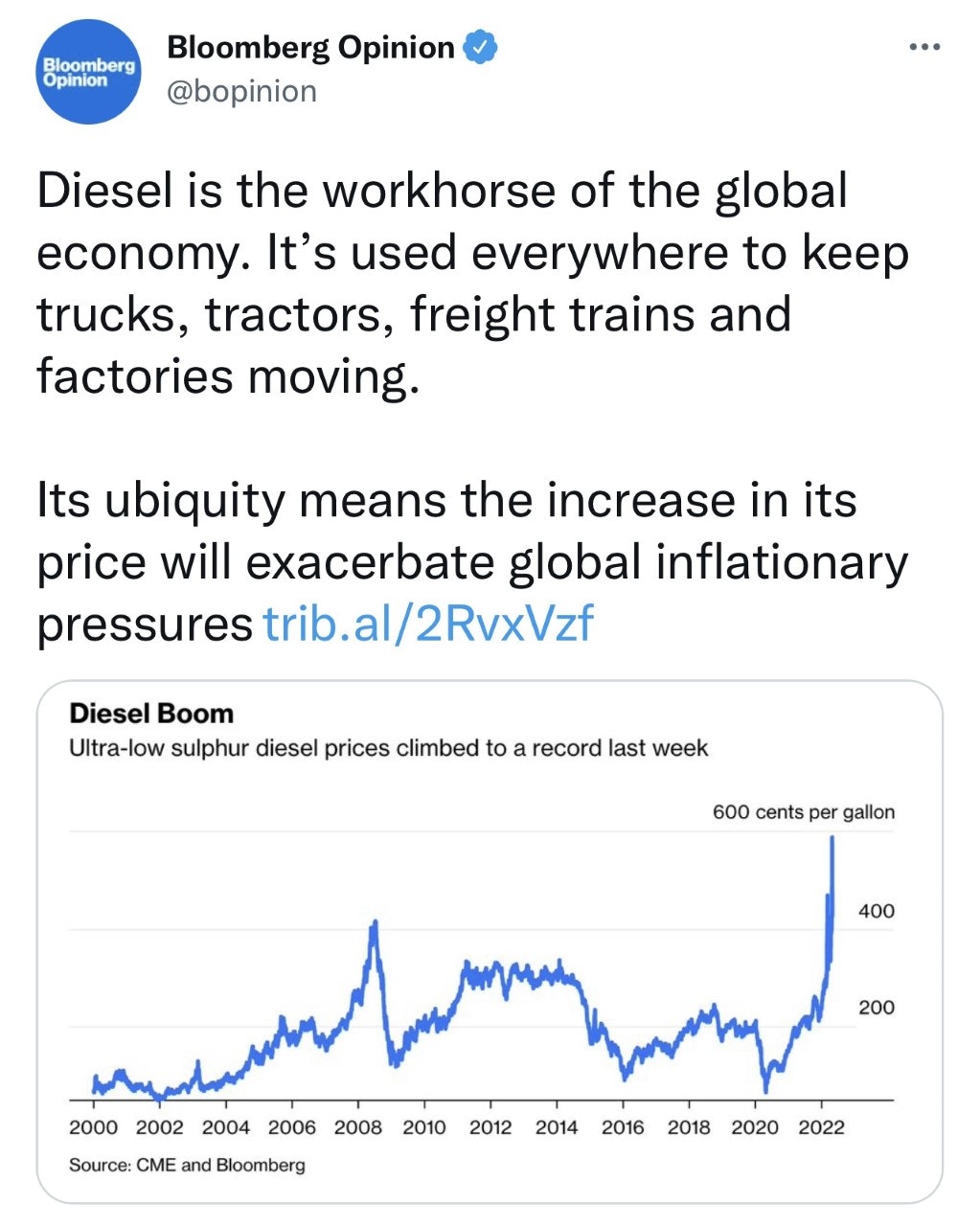

In addition to high gasoline and nat gas prices, diesel is expensive as well. Everything that moves or is made has energy costs in its price, not unlike those EU style VATs that tax every step of the supply chain, so if these energy prices stay high, it will feed into inflation and high prices for everything else to a greater or lesser extent.