Just in time for 2022 rounds of budget reconciliation legislation to include debt forgiveness for all - or at least the promise thereof if you vote us in power after November!

Not sure if that’s gonna work though. For every student loan forgiven, there’ll be a few pissed off taxpayers who repaid their debts on time and don’t see why their money should get redistributed to deadbeats who demonstrated that they cannot make good financial decisions. And the biggest hurdle to handing Congress control back to GOP won’t be on the ballot on Nov 2022…

From your fingers … Sadly, it’s been working for 2 or 3 decades, and probably longer. Not only do I not know the tipping point, I’m not even sure there is one any longer.

I was speaking for myself mostly since I know it’ll influence my vote. I was hoping it’d register beyond the general apathy of other voters as well.

I’ve read articles in favor of the debt forgiveness that do admit that it would not be a fair handout (to those who did not go to college - maybe because they could not afford it - or those who repaid their student loans). Regardless of the actual law and its supporters, it’s a bridge too far for me to accept that irresponsible behavior is rewarded while prudent financial decisions are punished. On basic fairness but also because it sets entirely wrong expectations that individual accountability is now worthless.

Heavily indebted lawyers figure they’d rather stiff their law schools than make a few bucks failing to get a few people over the “undue hardship” threshold in BK court. Bar association endorses student debt discharge.

Unless I read this wrong, how does their support stiff the law schools who have already been paid for the tuition charged on student loans? It’d stiff the lenders but I don’t think it’ll directly stiff their law schools.

Now the domino effect of lenders becoming much more cautious about lending could impact the law schools’ ability to keep selling their high-priced diplomas to student who can no longer find a lender to support risky borrowing. I’m not sure this would be a bad thing though.

Someone please confirm this is true. I’ll need to research who owns the most student loans.

I’m not fully versed on the whole student loan thing, but I thought these loans were govt backed. Thus, if a loan is discharged thru bk, aren’t taxpayers getting stiffed?

The Federal government by a long shot over the private lenders. 92% of student loans are Federal loans mostly because you take those out first because they are lower rate loans and only use private loans once we’ve exhausted your ability to borrow from Fed loans.

So you’re correct that it’s mostly the taxpayers who are getting stiffed. In fact, even Congressional Dems admitted that they likely do not have the authority to forgive private loans. So it boils down to another wealth redistribution handout from those who do not have student loans (for any reason) towards those who do. Which is the reason why not everyone wants to see their money go to pay someone else’s frivolous college spending.

Imagine you started working out of high-school because you could not afford college. You have a lower income than if you went to college but you now would also have to pay for someone else’s student loans while they enjoy the financial benefits (higher income, lower unemployment) from going to college. That’s a hard sale if I ever see one.

You’re right, I was assuming the law schools would carry some of those loans on their books. I think it’s mostly private lenders, since the unsubsidized direct DoE federal loans are only good for like $20k/year and law school will run twice that or more. I suspect private lenders are most of those involved.

I actually don’t think that’d be a bad idea honestly. Back the quality and worth of the education they provide with their own money rather than taxpayers’ and private lenders’.

Everyone who is fully “disabled” is getting their loans forgiven.

Here’s an article speculating on how Biden wants “targeted” rather than blanket forgiveness, presumably to make it more palatable, suggesting the previous requirements for things like public work forgiveness after 10 years could be “relaxed”.

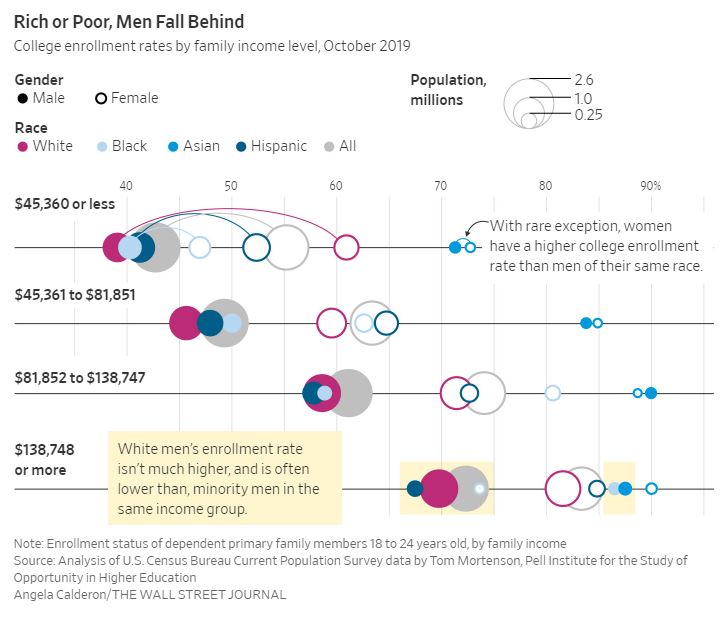

I wonder how much of that is the currently popular discrimination against white men and how much is guys who want to make money (for status, etc) realizing college is often not worth it at these prices. Sure the top ones and the STEM degrees still are, but I’d question the economic benefits of a middling college degree at this point especially when computer jobs or trade jobs can pay very well and don’t need formal education.

There are labor shortages in all skilled trades and if you ask any jobsite foreman, there are very few college aged young adult males applying for those open positions. The chunk of young men that used to go to college but aren’t now are mostly not entering the skilled trade workforce.

The Mrs degree is still a popular option. Why work hard and spend all that time and effort to become a well paid doctor or lawyer when you can just marry a well paid doctor or lawyer and spend his money?

It shouldn’t be nearly as popular considering women are competing for a smaller and smaller pool of available men that fit that description than ever before.

I hope Biden makes this giveaway retroactive. It took me a long time to pay off my student loan, but I returned every cent, with interest, and in a timely manner. Thereafter something strange happened:

I received a very kind letter from my college thanking me for having paid off my loan. At the time that letter was a head scratcher for me. I mean, of course I paid off the loan . . . and I never even considered any other option or thought somebody else would, or should, pay off MY loan. What a ridiculous notion!

It was only years later I realized not all such student loans were being timely repaid.

Isn’t that gold digger analogy REALLY old by now? In this century, many women are earning more than their husbands. This one included.

Plus that antiquated theory does not support the college graduation rates for women being higher than for men. If you only went there for gold digging, why would you bother graduating once you’ve accomplished your objective?

I hope Biden let’s this demagogic proposal die already.

We’re having more than enough giveaways as it is. No need to throw more money at people. Not when you’ve already bought their votes through other handouts.

Plus it’d be incredibly impractical and/or nearly useless. How much would you have to factor in inflation for people who graduated 30, 40 or 50 years ago? The strain on their finances was less then but with decades of inflation in college prices, it’d likely be peanuts now. Not to mention the difficulty in verifying the amounts paid due to how accessible records would be. Maybe you’ve kept track of these but I doubt that all lenders or colleges did. Potential for abuse from people claiming to have paid off way higher loans seems very high to me.

Social and psychological pressures and norms don’t always make this easy. Here’s a study of divorce risk with employed female spouses.

For marriages formed after 1975, husbands’ lack of full-time employment is associated with higher risk of divorce, but neither wives’ full-time employment nor wives’ share of household labor is associated with divorce risk. Expectations of wives’ homemaking may have eroded, but the husband breadwinner norm persists.

Just to add more speculatively - the traditional male breadwinner / female homemaker model worked well for many families because men tend to be ambitious for their career and women tend to like to care for their children. Each person got to do something that needed doing that played to their (traditional) strengths and motivations, and each would be socially validated by achieving success in those fields respectively (career vs family). Back in the days of more physically demanding jobs, it played to biological strengths as well. It also made it easy to work together since there was no direct competition.

Now with dual income families, men with a traditional mindset feel a competitive pressure to achieve more on the career front than their spouse (as well as their rivals at work), which can lead to frustration and insecurity when that’s not the case. Similarly, employed women still often have a traditional mindset of seeking a husband who has an equal or preferably higher social status than they do, which means smarter / richer / better job these days in professional circles, so there are increasingly few “eligible” men under this mindset for an accomplished professional women unless she is willing to “settle” for someone less professionally successful. And just as it makes economic sense with young children for the lower (or un-) paid woman to stay home and raise the kids, if the man is the lower paid spouse, it will make economic sense for him to take over the child care duties. But a lot of men aren’t going to be as good as or motivated or psychologically ok with that, which leads to further stresses on the relationship.