I’m sure we’ll see more PR’s reminding eligible voters about these efforts

In this round of forgiveness, more than 206,000 borrowers will collectively get $3.6 billion in debt erased through the Biden administration’s new Saving on a Valuable Education, or SAVE, plan, due to the provision that allows for debt forgiveness after shorter periods than other income-driven repayment plans for those who originally took out small amounts for college.

You don’t want to deliver the forgiveness prior to the election or they won’t need you. You have to only deliver the promise that if I get ANOTHER 4 years, this time there will be student loan forgiveness.

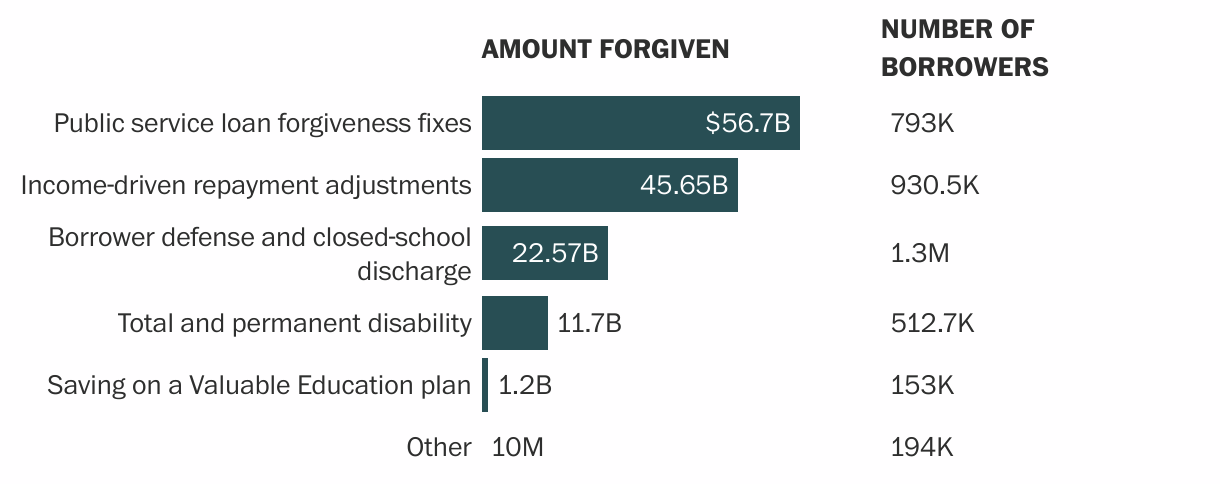

Here’s what I think may be a detailed breakdown of that number, but I can’t see it because I think it’s interactive and wasn’t archived properly by the archiving site I use:

To be fair, I don’t mind too much the forgiveness of some of these that were essentially promised to borrowers but never delivered due to a (deliberately?) messed up system. Public service loans and income-drive repayments might fit under that.

But some like the borrower defense and closed-school discharge, I disagree with. Outside maybe of students who were enrolled when the school closed and could not finish their questionable “degree”, it should not be the taxpayer’s responsibility to pay for suckers who frivolously got in debt for useless diplomas. That’s in the realm of personal responsibility. What’s next then? Pay for repairs on the used lemon they purchased without doing full inspection by a mechanic?

Same to some extent with total and permanent disability. These are unfortunate cases but why should the taxpayer be a backup disability insurer beyond what social security already offers? Especially without an act of Congress to validate that the whole society was ok to essentially add this to social security disability benefits.

Wait – are you saying that some of these loans were promised to be gifts when the loans were made? If so, why not make them grants/gifts/welfare? Regardless, if the borrowers were promised to never have to repay the loans when they made them, I certainly believe they should be paid by the taxpayers, as originally promised.

ETA: After a brief glance, it seems that NONE of these loans were “forgivable” at creation. Any supposed forgiveness is due to vote buying efforts. I’m not opposed to forgiving student loans if the taxpayer gets a benefit, eg doctors/teachers/veterinarians/etc in under-served/performing areas. IMO, that is getting a service for the payment of the loan. If you’ve got a 3+ GPA out of med school, and are willing to work in a ghetto or other under-served area, your loan should be forgiven and you should not have to pay tax on that forgiveness, since you earned it. OTOH, if you’re not willing to earn it … and I mean really earn it as in the above example … pay your debt.

Some of it is stuff like agreeing to be a teacher in a underserved area for X years, in exchange for loan forgiveness. It wasnt necessarily part of the deal when taking out the loan, but it was on the table when chosing what job to accept.

I have no problem with that forgiveness, it’s more a barter. Income based repayment is a different matter, loans shouldnt be forgiven because the borrower slacked off for long enough to qualify.

These have been offered since 1995. Unlike the government job-related forgiveness, the forgiveness for these IDF loans was actually specified into the terms of the loans. So I don’t have a problem with the terms of these loans simply applying as written. Although I take issue with the years in forebearance (including during pandemics) being counted as part of the forgiveness rule after 20- or 25-yr of payments. But if the replayments were not processed right due to red tape from servicers (like the servicer which billed the monthly repayments at $0.01 below the owed amount to not count these months at all towards the forgiveness), that’s something that should be corrected.

However I agree that allowing borrowers to switch after the fact to income-driven repayment is a lot more questionable since it’s effectively changing the terms entirely. Nobody should be entitled to that just because their diploma is useless and/or they over-borrowed for it.

From a taxpayer point of view though, do we prefer these loans in default or forebearance forever compared to having these deadbeat borrowers still effectively paying something back in an income-driven repayment plan with forgiveness after 25-yr of payments? It feels a bit like the Medicaid offices in some states, costing $6M/yr in operating costs and working hard to disqualify $900k/yr in insurance payments). If they end up at least repaying what they borrowed in inflation-adjusted dollars, I’d probably take the limited loss personally rather than them never paying even that much back.

A lot of this would fix itself if the government stayed out of offering loans altogether and we made these student loans just another variety of unsecured loans by private lenders (to which the same bankruptcy laws would apply as to credit card debt). Private lenders would not underwrite student loans without more careful consideration of the borrower’s future ability to repay. And maybe colleges would look a bit more closely at their costs if attendance craters due to lack of affordability. And if this means goodbye to some of the questionable-value majors that the current state allows colleges to offer, I don’t think I’ll be too crushed.

The federal budget deficit will hit $1.9 trillion this fiscal year, according to an updated projection released Tuesday by the Congressional Budget Office. That’s 27% – or $400 billion – larger than the agency estimated in February.

Most of the spike in the fiscal 2024 deficit stems from four factors that are expected to boost projected spending. The largest is a $145 billion increase that’s partly due to changes the Biden administration made to student loan repayment plans and a new, proposed forgiveness program that would waive some accrued interest for millions of borrowers.

Of course it’s CNN so they can’t avoid trying to wedge in a comment about how illegal immigration will magically help reduce the deficit, which just isn’t true since most of the illegal immigrants are unskilled and cost a lot more in welfare and public assistance than they produce in taxes or economic activity (hence the irony of the blue sanctuary city lamenting their budget woes from getting shipped a tiny fraction of the illegals from the border).

Aren’t they just reporting the CBO own estimates that this immigration surge will boost economic activity? The CBO reported these estimates with high uncertainty and I definitely agree doubts on the conclusion that unskilled illegals will help reduce deficits. But I don’t think it particularly biased of CNN to be reporting these CBO estimates no matter how uncertain they may be.

Either way, it’s no surprise that deficit will skyrocket again due to increased spending. There’s no accountability mechanism of any kind for running deficits. This will continue until the heads of those who run deficits are on the chopping block at each election cycle (or when we default on that debt directly or more likely indirectly via runaway inflation).

in an entirely unexpected move, Biden plans to propose giving away tons of money to students in Oct just ahead of the election vote and with little enough time that the courts will tell him, again, it’s illegal.

Based on the orchestrated chorus of bigwigs asking Biden to kindly drop out of the race, me thinks he won’t be there in October. His replacement likely will offer more student loan forgiveness and amnesty for illegal immigrants too.

Hopefully you’ll be right and I’ll be proven wrong. Crossing fingers!

However, sadly most likely Trump will continue energizing his base the way he normally does.