I agree. Power of the purse should apply both on the spending and revenue sides.

That’s how the budgets work. Especially thinking about how the recent budgets have gone (through reconciliation to avoid fillibusters). The budgets have had to be balanced over a 10-years period counting expected revenues and expected spending.

So any time, the Executive deliberately avoids collecting revenues that Congress directed it to (not collecting on defaulting federal student loans or not collecting ACA penalties which were determined by SCOTUS to be a form of tax), it effectively usurps Congress’ power of the purse.

High time Federal government gets out of student loan underwriting entirely. These charts make it obvious it’s incapable of operating this program in a non-money pit fashion. Just keep on servicing the current loans (or try to sell the business to private lenders) but at least stop underwriting new loans and allow the market to dictate terms of all student loans (preferably allowing the private student loans to be discharged by bankruptcy like other non-secured loans).

Agree entirely. The loans and the losses represent a direct subsidy from the taxpayers to the universities. The universities have abused the system and increased their tuition and fees at a rate much higher than general inflation. Students look at the loans as “free money” and do not evaluate the worth of the studies objectively…

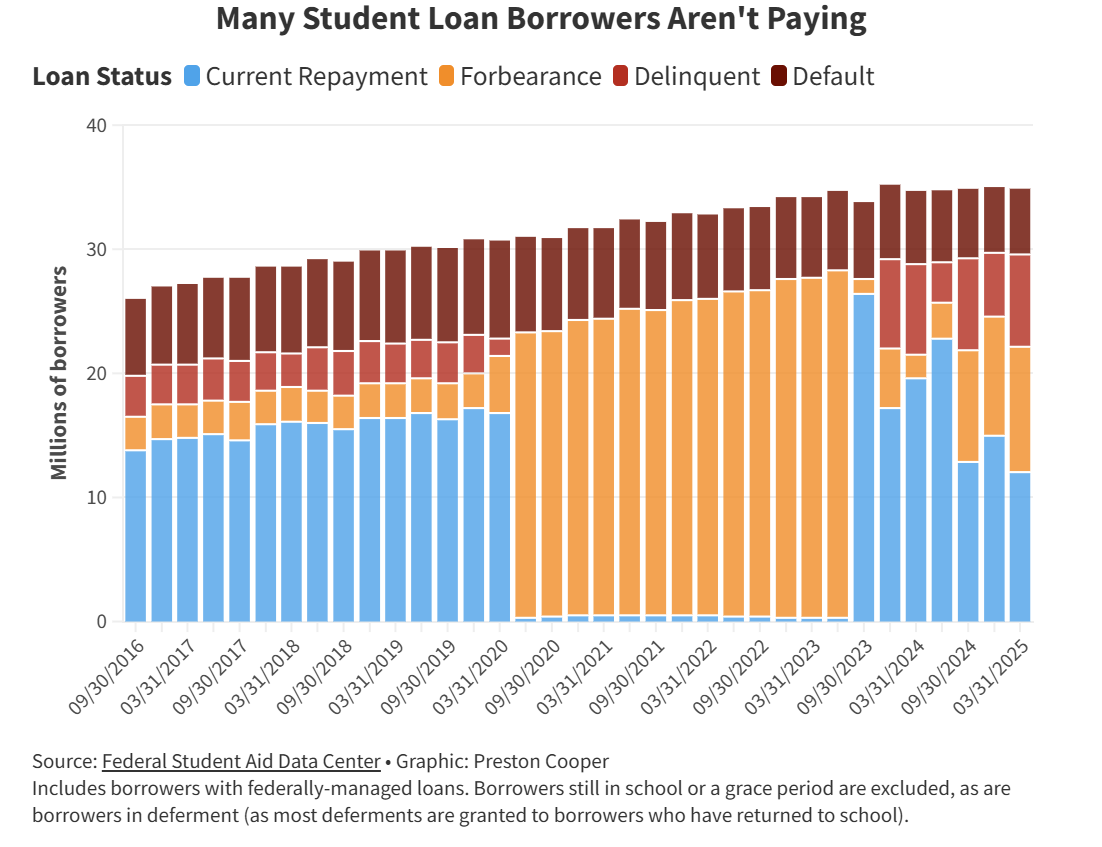

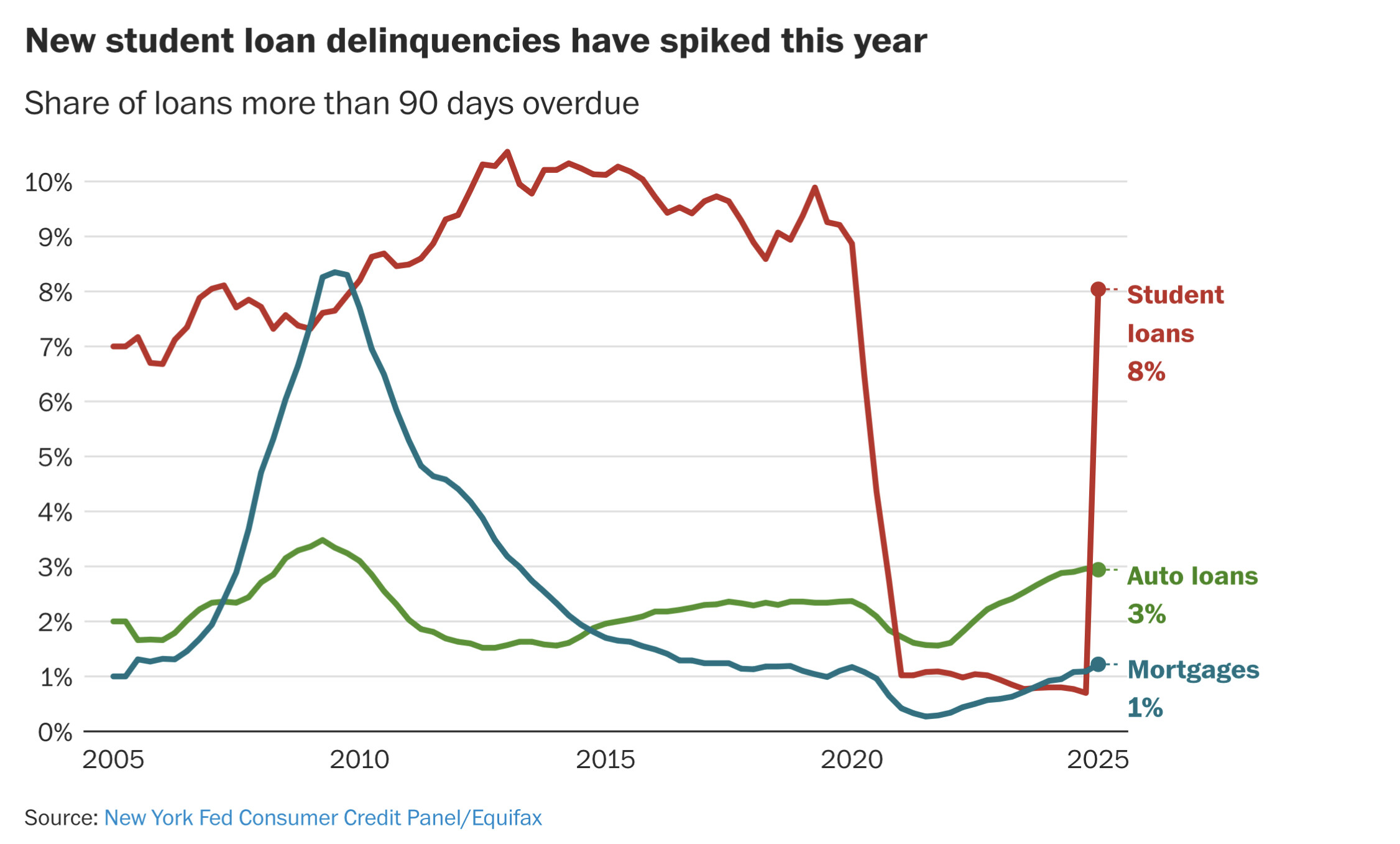

Credit scores dipped by more than 100 points for 2.2 million delinquent student loan borrowers, and 150 points or more for more than 1 million in the first three months of 2025, according to an analysis by the Federal Reserve Bank of New York

Trump wuss’s out, wont garnish SS checks to collect student loan defaults, to avoid looking like “he’s cutting social security”. I guess if you managed to not pay your student loans til you’re 62 (pretty impressive), maybe you got away with it.

Probably why it’s not worth it. How many people borrowed a ton of money in the mid-80s and are still in default? Plus if they defaulted and never got their wages garnished for student loan repayment, maybe their wages (and thus their future SS checks) are not worth much. All in all, I’m guessing it’s not a huge write-off compared to the poor optics.

I can see students that enrolled in universities like Phoenix or similar being the most important beneficiaries here. Those students tend to be a lot older, even in their late 40’s, and could have racked up serious debt to earn not just their bachelors but also graduate degrees, while being made to believe their degrees were a path to riches. Those universities were enrolling thousands and thousands of students back in the 2008-2014 period, maybe still are to this day.

The whole concept of student loans not being dischargable is because unlike other assets, you cannot stop using and “give back” the education asset you received for that debt. Since you retain the knowledge, you remain liable for the debt.

But once you start drawing social security, there’s a case to be made that people are no longer using that education (even if they technically still have it), and even that many old people do start to lose the knowledge and in fact no longer have it. The reasons for it being treated differently from other debts start to no longer apply, and you arent really getting away with anything more than you get away with when any debt pasts the statute of limitations for collecting.

I’m not convinced that is unique to student loans. Comparing to credit card debt or similar personal loans not secured by any collateral, you don’t stop using some of the things you procured with the loans, especially intangible goods like vacations, dining experiences, concerts, etc. Some low-value tangible goods you acquired on credit may also not be liquidated upon bankruptcy. But I still don’t see why education is different from intangible goods obtained on credit. Only difference I see is that you can potentially leverage your education for better income (although if you’re defaulting, that is likely because said education was of low value in the first place).

I think the main reason they cannot be discharged via BK is because it’d allow students to graduate, immediately file for chapter 7 bankruptcy with next to no assets to liquidate, and be done with it (albeit at the modest cost of having their credit history trashed for their first few years after college).

Still, one issue that needs solving is that unlike any other kind of debt, student loans are extended to borrower with basically no due diligence from the lender on the borrower’s ability to repay the debt. Protection from bankruptcy is what lead to this frivolous lending practice where loans are extended equally to someone studying dance or culinary arts vs. someone studying civil engineering. Ability to repay via expected career earnings never seems to enter this process and IMO what lead to excess lending/borrowing and trickled down to associated college costs.

Sure you do. Once you eat a dinner, you can’t keep eating it. Once you use a concert ticket, you don’t get to keep going to concerts. Once you fly to Hawaii, you don’t get to keep flying there on demand. You may retain memories, but you don’t keep experiencing it.

While the skills and knowledge you obtain in college stay with you for a lifetime. Those skills may become obsolete, but you still have those skills; they don’t get used up, they don’t have finite usefulness by design.

As of July 2026, total graduate school borrowing will be limited to $100,000, or $200,000 for professional degrees.

Graduate students will also face a lifetime borrowing limit of $257,500 for all federal loans, including undergraduate loans. Parents borrowing on behalf of their children will also see caps.

In addition, the Education Department has proposed no longer classifying fields such as nursing and accounting as professional degrees. That means students in those fields wouldn’t be able to borrow as much for graduate school as those pursuing dentistry, law and medicine.

Currently, graduate students can borrow up to the full cost of attendance, minus other aid. Undergraduate borrowing was already limited, and those caps will remain the same.

The department says the new loan limits will help drive down the cost of graduate programs. Critics say students will simply turn to private lenders, which tend to offer less-generous repayment options.

If they are pursuing a graduate degree, they should be able to understand and accept the consequences of borrowing large amounts. The less-generous the repayment options, the more likely the point will get across that they shouldnt be borrowing this money.

I can’t help but believe that the ability to finance is what has pushed college cost into the stratosphere. Not much different than the inverse relationship between housing prices and interest rates on a macro scale…

I suspect there might be a push to do some things that even Democrats will like as we get closer to the midterms .

If I’m not mistaken, private student loans can be discharged in bankruptcy like other consumer debt, which means they’re not going to be given out like candy on Halloween, and they’ll have commensurate interest rates. That’s not a problem, it’s exactly what’s needed to bring down costs.

“This decision formally ends the SAVE injunction that has forced over 7 million SAVE borrowers into economic limbo—pushing meaningful debt relief and affordable monthly payments out of reach,”

No, excessive borrowing for gender studies degrees is what forced them in economic limbo.

Why does a judge get to sign off on this? His ruling is that it is either legal or illegal.

“I’m bracing for an astronomical bill,” Brenda McCoy, a 60-year-old SAVE borrower, said. “My goal was to be self-sufficient. I was making the payments, I was being a responsible person, but it has to be something I can afford.”

Why arent such people being put up as cautionary tales, instead of faux innocent victims?