If they just wanted to communicate changes, since the deduction has nothing to do with Social Security, wouldn’t it have made more sense to send it from the IRS email?

Or at least narrow it down to people who are or will be 65 by 2028. And if it were for information purposes, email to those 61+ now, should have mentioned the expiration of this deduction (tax year 2028), the AGI phase out/limits, and clarify that the deduction applied also to those not receiving SS benefits or even being eligible for them (so deduction does not impact their decision on when to claim SS benefits). That’d have been much more useful than spamming 71 millions households, many of whom will not be impacted directly (outside of being saddled with the extra deficit).

The new law includes a provision that eliminates federal income taxes on Social Security benefits for most beneficiaries, providing relief to individuals and couples. It does so by providing an enhanced deduction for taxpayers aged 65 and older, ensuring that retirees can keep more of what they have earned.

The highly political nature of this email is revolting. There is a reason they don’t mention the expiration – they are selling it now as a tax cut, and for the next election they’re going to say that the Democrats will raise your taxes (by allowing this temporary deduction to expire).

I’m against any temporary tax cuts, or at least ones set to expire before 10 years. They are just insidious. It’s human nature to get used/addicted to something good and then hate being deprived of it.

Moro than anything, these temporary cuts are just a loophole. An artifice to pass unsustainable permanent tax cuts that would never pass reconciliation rules. Their only purpose is to bypass the wise limitation to not have tax laws that induce budget deficits. You only need to look at the current policy vs. current law nonsense that was pulled to pass this latest Bloated Bullshit Bill to guess how the next tax reform is gonna play out.

If you should be around there, the marginal tax rates increase by a fair bit as you start to lose 30% of your SALT for every $1 over $500k. They give various examples with dividends, income, CGs, etc.

UK in financial trouble, eyes wealth tax but of course wealth taxes like socialism haven’t worked anywhere they’ve been tried. But this time could be… yet another cautionary example if they go through with it.

More than half of UK millionaires in a survey signaled they’d be more likely to leave the country if the Labour government introduces a new wealth tax.

That may be at least partially because the UK doesn’t tax their expats the way the US does. If the US implemented a federal wealth tax, you’d be unlikely to escape it by just living abroad. Anyway, I also imagine a new UK wealth tax would be accompanied by a comprehensive exit tax like the US has.

Either way, it’ll be interesting to see how they solve this one. Maybe they can just do like the US does which is printing more money and letting the deficits continue…

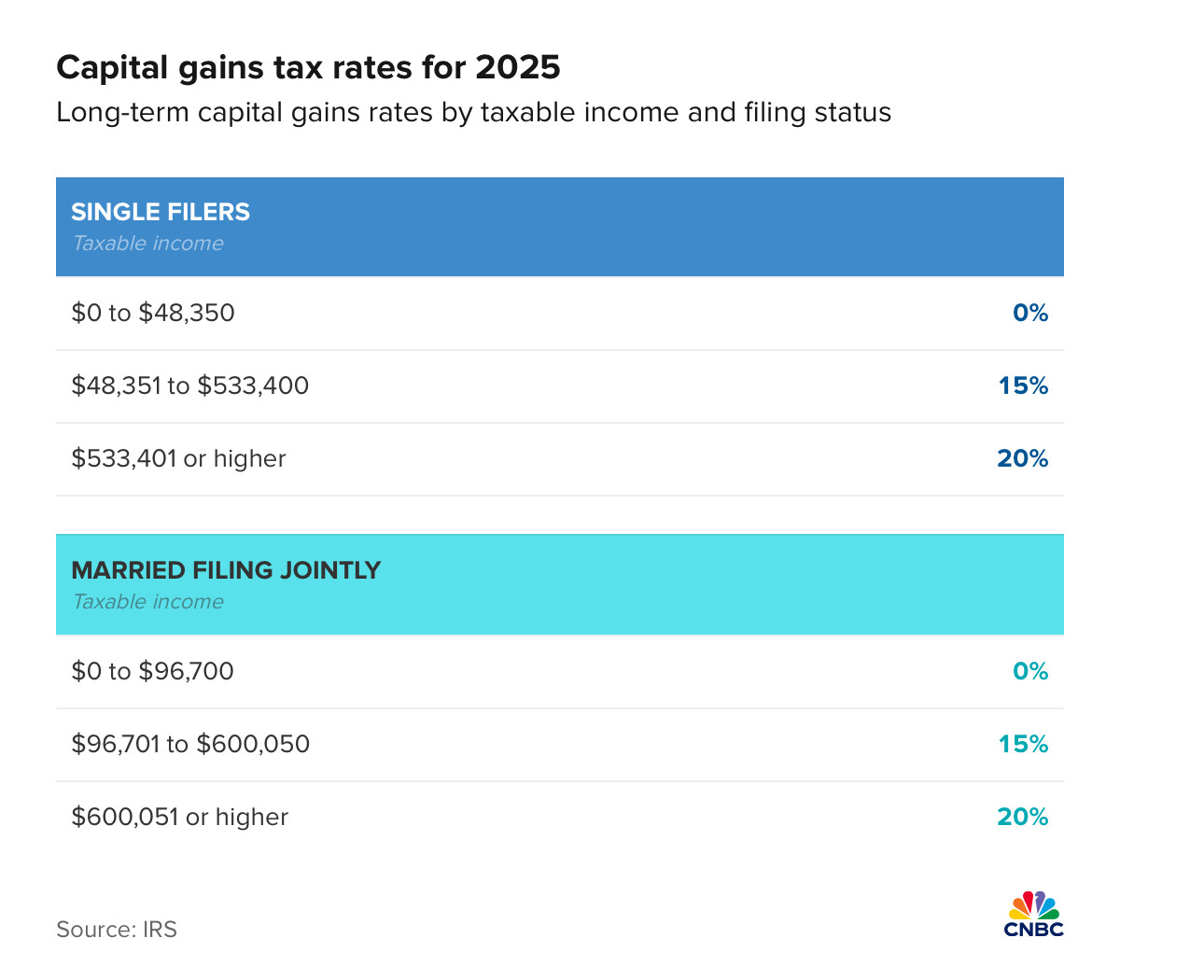

For 2025, you’re eligible for the 0% long-term capital gains rate with taxable income of $48,350 or less for single filers, or $96,700 or less for married couples filing jointly.

Woohoo the CNBC “experts” just found out about tax gain harvesting.

But that’s nothing new from the BBB though. The brackets have been increased for inflation each year since the TJCA of 2017. Before that, the 0% rate on long term capital gains was up to the 25% bracket.

In 2023: $44.6k (single) / $89.2k (MFJ).

In 2024: $47k (single) / $94k (MFJ).

In 2025: $48.3k (single) / $96.7k (MFJ).

Not that it’s not a great opportunity. I’m planning to use it for a few years while delaying taking social security along with Roth conversions up to the standard deduction (and extra $6k if still available when I’m 65). But the article making it sounds like an extraordinary opportunity afforded by the new tax law is a bit misleading (or misinformed).

In general, I’d think it takes some special circumstances to have income significantly under $50k and have investments large enough to produce significant capital gains. I’ve been able to benefit from it a few years, but it was with whopping 2- and 3-figure gains. Once I grew to having thousands of dollars of capital gains, my income was too high to qualify.

I am kind of curious how many taxpayers do get to benefit from the 0% rate?

A typical scenario would be retired people who are not yet collecting social security. All it takes is long-held index ETFs to build 6-figure amounts of long-term capital gains in taxable account. Once retired, you can withdraw 100k of gains (+ cost basis) of these ETFs (without risk of wash sale if you reinvest portion of them), and pay 0% tax on the withdrawal. That’s my scenario retiring soon where I’ll delay SS payments until age 70. Including cost basis and after standard deduction, I’d be looking at about $150k/yr withdrawal from brokerage account on which I would not be taxed a penny.

That I don’t know. Probably not that many. Outside of the scenario I highlighted, maybe people with very inconsistent incomes. Either way, I’d bet the answer has a strong correlation with the use of financial planner or financial planning software.

Definition of compliance may also be generous there. Without cost basis reported by a third party, it’ll be hard for IRS’s automated tool to flag under-compliance. One could report their cost basis as if they purchased their crypto in Dec 2024 since transactions before that were not reported on 1099-DA. Or simply transfer crypto to another exchange. So for people trading coins directly, I’m not sure it’ll increase compliance massively since there will still be many loophole to under-report.

I think the main bump in compliance is gonna come from ETFs.

Here is what the grok AI says about the news that three democrat states are refusing to pass along tax reductions in the OBBBA. I am surprised that my home state of Taxifornia is not included.

**Colorado, Illinois, and New York are refusing to conform to the federal “no tax on tips” and “no tax on overtime” provisions** introduced in the 2025 One Big Beautiful Bill Act (OBBBA). This federal law allows deductions for qualified tips (up to $25,000) and overtime pay (the premium portion, up to $12,500 single/$25,000 joint) from federal taxable income for 2025–2028.

These states are decoupling from the federal changes to protect their budgets from significant revenue losses, meaning residents must still pay state income tax on tips and overtime income (or at least the overtime portion in Colorado’s case).

Here’s a breakdown:

- **Colorado** — Decoupled specifically from the federal overtime deduction (via a law passed earlier in 2025). Taxpayers must add back any federally deducted overtime amount on their state return (e.g., a new line for “Excess federal deduction for overtime pay”). It appears to conform to the tips deduction.

- **Illinois** — Has not adopted the federal exemptions for either tips or overtime. The state is expected to update its Schedule M to require taxpayers to add back federally exempt tip and overtime income, so it remains fully taxable at the state level.

- **New York** — Explicitly refuses both exemptions. It added new codes to Form IT-225 for “Add-back of exempt tip income” and “Add-back of exempt overtime pay,” forcing taxpayers to report and tax these amounts on their state return.

This is part of a broader trend where some states (especially Democratic-led ones) are not conforming to the federal changes to avoid budget shortfalls, while others automatically follow or have passed their own exemptions. Residents in these states will see federal tax savings but not state-level ones. For the most accurate filing, check the latest state tax forms and instructions for 2025.

Aside from out of state munis, I cannot think of any other income that is exempt from federal taxes but subject to state tax. So I think it’s fair to highlight the states in which these types of income are still taxed as exceptions, especially when there are relatively few.

That said, each State taxes whatever they want to balance their revenues. Nobody’s pointing fingers over - effectively more impactful - differences in sales tax, property tax, or estate taxes between States or vs. federal level. Why not complain that most States have a VAT tax whereas the federal government does not (outside of Trump tariffs that is).

More interesting/revealing question for me would be whether the use of Grok AI was significant in getting this type of summary vs. using another LLM… Or to what extent loading the prompt with terms containing an implied bias does dictate what answer you’ll receive from a LLM and/or the tone of the answer.