Billionaire tax details. It’s a mess, but basically stocks get hit on paper gains at the max cap gain rate, while illiquid stuff gets charged some “interest” and then gets taxed on sale /transfer / death, including to a spouse.

I’m just thinking. This thing has a “multiplier” effect. Suppose Elon Musk has to pay a $10b tax bill from this new tax on unrealized capital gains. Now unless he already has $10b sitting in cash, he would have to sell his stock to raise money to pay for the tax. Selling his stock would force him to realize capital gains. If the marginal tax rate is 24% (as in the article), then he would have to sell 10/(1-0.24) = $13.2b of his stocks. So the tax bill for him would be $13.2b and not $10b (“multiplier” effect).

“Eventually, they run out of other people’s money and then they come for you.”

Musk is selling later this year anyway, that’s why he moved to Texas at the end of last year and sold his CA property. But yeah, it can force business owners for very successful companies to sell off their stock once its public thereby limiting their gains and depressing the stock price.

Exactly. Specially because the money will be used to fund social welfare programs which can’t be cancelled later on. The tax pot will need to be replenished with more taxes from other people.

None of this would happen. He’ll just get a loan against his assets to pay the $10B tax. Say he gets 2% APR loan, interest on $10B would cost him $0.2B/yr. Much better than the immediate loss of $3.2B in realized capital gains tax.

That said, if his tax bill is $10B in unrealized capital gains, I’m not sure I’d feel terribly sorry for his financial situation… That’d mean having what $50B/yr in capital gains?

Oh yes, that “loan” argument. But it might be that simple because the loan amount will grow to be a significant fraction.

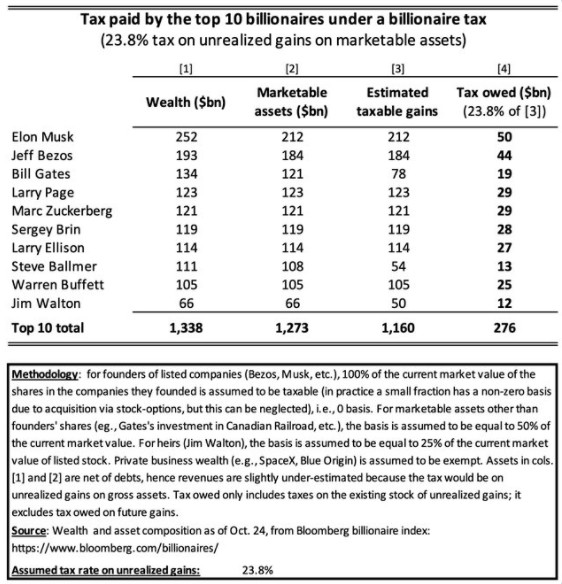

The way the proposal works is to apply a 23.8% on the capital gains of the assets (see xerty’s link). For Musk’s case, the estimated gains is $212b. At 23.8%, the tax is about $50.5b. He then gets the chance to spread the payment over 5 years. That why it ends up with $10b in tax for the first year.

After the first year, the tax would be on the gains beyond the $212b. So it is not $50b/yr in capital gains.

That’s 10 of them only though. If the measure is supposed to be on the top 700, the revenues could be higher than that. But it’s also misleading because it’d be a one-time catch up amount. After that, they’d only be taxed on incremental annual gains so nowhere near as high revenues.

On the flip side, I’m not sure you can trust any estimate since nobody has an accurate picture of what unrealized gains people have and in what accounts. At this point, probably not all their assets are in stock of company they founded. And if some assets are in tax-deferred accounts or tax-exempt accounts like Roth IRAs, they probably will be exempt.

One thing jumped at me. So if you own a very successful company that’s not publicly traded, what’s your incentive to do an IPO which would see you suddenly taxed on the value of the company?

One reason is because the stock / IPO market is hot, and OTOH, you know what it’s actually worth and it might not be positive! Better companies stay private much longer these days, with plenty of private equity happy to fund their capital needs if they’re doing well.

SALT cap might be back on the table as a handout to the rich Democrat consistency in the latest round of haggling.

This would actually be a tax cut for many, since the Trump tax cuts were about breakeven when the top rate was lowered to 37% even for those who lost significant state tax deductions, while the latest proposals have the old 39.6% rate kicking in at $10M or something but the deductions coming back for everyone (or at least higher limits).

I agree. I just think it may make them wait longer before going public due to the massive tax hit the founders would take by doing so vs. staying private.

Not sure this is a big argument for bringing Manchin around considering his state is not one to benefit from removal of SALT deductions cap.

Sarbanes Oxley with the liability for executives and huge compliance costs was already a deterrent to being public. This triggered a round of value small caps being taken private, either by the owners or PE firms several years back.

These days you never see a microcap cap IPO of a profitable business - they’re all risky biotechs or early stage cash burning “story” stocks that hope to cash in on the hype and need the public markets to raise capital from suckers investors and the investors have been more than accommodating with all the Fed trillions sloshing around.

Instead of a ridiculously complicated tax code that would leave someone with different tax liabilities depending on who prepared the returns, how about simplifying it so you wouldn’t need audits. The last thing you want is a comprehensive audit that takes an inordinate amount of time, energy and money to respond to. Trust me, most people would gladly subject themselves to a rectal probe before going through an IRS audit. The tax code is so crazy, even the the IRS agents don’t understand many of its permutations and combinations. The best IRS is a defanged IRS.

While I certainly agree that simplifying the tax code would be great, that’s apparently difficult to impossible. The previous president promised and actually tried that, but the end result, at least for me, was more half-empty pages used than full pages before, and nothing was simplified.

My personal return is, I believe, relatively complicated (with schedules A-E, H). I do it myself and don’t find anything ambiguous (not after digging into the instructions anyway). I think the only complications I’m missing are partnerships and non-sole-prop business related. This leads me to believe that if you get different liabilities from different preparers using the same source data, then some of those prepares are incompetent or dishonest – you can claim and get away with a lot and for a long time, it’ll only end when / if you are audited.

That make no sense, as that’s just bound to cause an increase in cheating / non-compliance.

With all due respect, you are extremely naive. Any return with rental income, passive losses, K-1’s, partnerships, capital gains/losses or as you said non-sole prop business related returns can be extremely complicated.

I’ll tell you what: You give your source info for your tax returns to three competent tax preparers. Let them prepare the returns and I would bet you a considerable sum of money they don’t have the same tax liability for you.

Our tax system is extremely screwed up. Hiring thousands of people off the streets to become IRS revenue agents is a recipe for disaster.

I have rental income with passive losses, and I’ve had capital gains/losses. None of it is “that” complicated. I’m not familiar with the other things since I haven’t had to go through those, yet.

I wouldn’t take the bet as it’s possible that the tax prepares would come up with different results. My bet would be on the fact that there’s exactly one correct (or perhaps ideal) way to prepare my return, and anyone who deviates from that is wrong, unethical, or didn’t ask me what I want to do when there’s a choice.

For example, I know I could save a bunch if I claimed to be a real estate professional. And I could probably get away with it, but I won’t do that because I don’t qualify under the written rules.

Another thing I can think of that is not illegal / unethical is something like the home office deduction. I could probably take it and save a few bucks today, but it’d make my return more likely to be audited, and any savings would get recaptured when/if I sell my house, which might put me in a higher bracket and be disadvantageous in the long run. A similar scenario applies to I-Bond interest – I can elect to pay taxes every year or pay them at maturity/sale. But these rules are not ambiguous, they just give the taxpayer a choice.