Funny, I just finished noodling around the internet trying to locate something which might help you. Decided in the end it was beyond me, did not want to embarass myself, and saw your post after abandoning my efforts. However:

We both would agree time is of the essence in this matter. And when it comes to completing Form 8962 there is a WHOLE LOT of material out there, on the net, which could help you. It’s just beyond me, but most likely not beyond you. Were I in your situation, and time being of the essence, I would devote at least an hour or two to reviewing internet help websites for Form 8962. There are many of them. Some are just BS as you would anticipate. But one might just help you out. It is possible others might have encountered your problem and posted a solution.

Sorry I’m not able to be of assistance. Good luck!

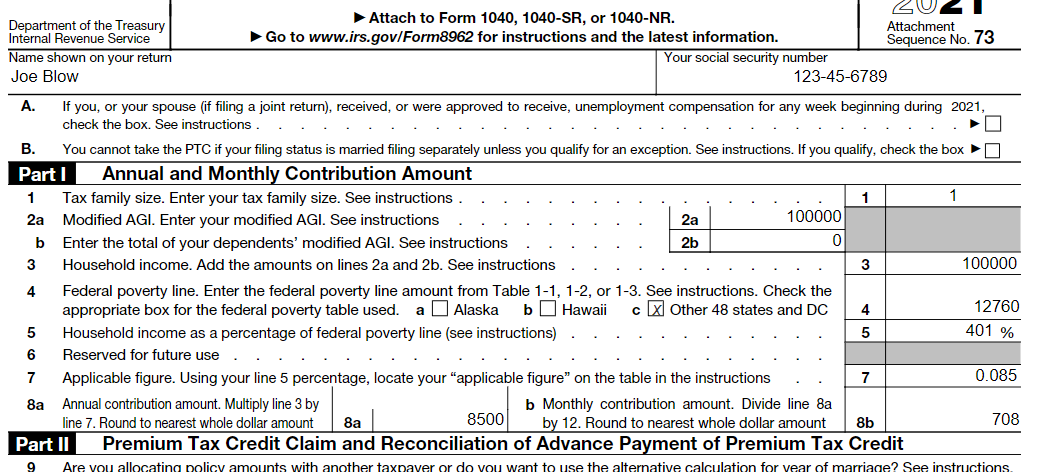

I doubt this helps, but here’s what the top half of that form looks like from my tax prep software if I just use a family of 1 and an income of $100,000. My only guess would be to use “401” and let the freefillableforms software fill in the “%”.

I have a max of 3 digits I can enter on line 5, and it only accepts digits, no decimal or percent sign.

I tried leaving the % blank, and it was also rejected - but threw 3 other errors as well. So maybe that’ll break up whatever is blocking it.

If not, the next try will be putting a 0 on line 2b, which is currently left blank. Maybe it being blank is causing some ambiguity in line 3, which affects how the IRS divides to get line 5.

I want to try other percentages (under 400%), but if it does get accepted it’ll be an incorrect form.

I have no idea if it will help, but if you think it will and want me to try and input your actual details to spit out a form like the one above from my software, just PM me your details.

The form itself fine, its the IRS that is rejecting it when e-filed. I could print and snail-mail it and [I assume] it would be fine. I’ve been trying to work around whatever the IRS system isnt liking, without success. But the ‘trying’ requires submitting the return and hoping the form is finally accepted.

Issue : Business Rule F8962-006-01 - If Form 8962, Line 1 TotalExemptionsCnt has a non-zero value, then Line 5 FederalPovertyLevelPct must be equal to Line 3 HouseholdIncomeAmt divided by Line 4 PovertyLevelAmt.

In your sample form, line 5 would calculate to 7.8369. I’ve tried 401% (the correct answer per the instructions), 783%, 784%, and 400%. Why the form doesnt just do the math itself rather than making me enter the number, I dont know.

It’s a rejection issue that google finds various reports of, but nothing related to freefillableforms specifically and with no work-arounds suggested.

After a week a countless attempts, and exactly the amount of help expected from FreeFillableForms (not even a response, despite their 2-day promise), I gave up and just mailed in my printed return. Maybe I get lucky (or maybe the luck will be getting it processed before the following rate change in November), but for $3k in bonds it wasnt worth worrying about too much.

But I thank you again, Shinobi - had you not noticed that form 8888 didnt print with your full return, I probably wouldnt have thought twice about it. But I was able to print the form separately and include it with the rest of the return.

Bad if you are counting on the refund to pay rent. But if I wasnt trying to use my return to buy ibonds, I’d happily let them take as long as they want and collect the 3% interest indefinitely.

Very sad that you have been reduced to paper filing. I was thinking maybe there might be a way for you to file without that damnable form in order to get your I bonds. Then, once the I bonds were safely in hand, file an amended (paper) return which would include the balky form.

Those darn I bonds today are, more and more, looking like solid gold. It’s tough to miss out because of an IRS computer foul up on a single form.

Course look at me talking. This year was my first to snag the extra five grand in I bonds. I stupidly have been missing out for YEARS. So I’m in no position even to be commenting on this.

I considered that. But deleting that form would’ve increased my refund by over $3,000. So I would’ve then been facing a April 15 deadline to get the refund processed, then send the amended return and repay what was due. It would’ve let me get the full $5k in bonds, but for only $5k in bonds it wasnt worth all the involved hassle.

Now there’s new guidance from the Internal Revenue Service on required withdrawals for heirs of these accounts. The proposed regulations, issued in late February, would speed up required payouts and add paperwork for many heirs of traditional IRAs but not for heirs of Roth IRAs. They also won’t affect most spouses who inherit retirement accounts.

The new IRS rules fill in details of the Secure Act, a law Congress passed in 2019 that revised rules for retirement plans. One of its changes greatly sped up required withdrawals for many retirement-plan heirs, enraging IRA owners who had made estate plans based on prior law. The faster money has to come out of retirement accounts, the less tax-deferred growth there is.

The IRS is accepting comments on the proposed rules through May 25 and will issue final guidance later. In the meantime, retirement-account specialist Ed Slott advises holding off on missed 2021 payouts for years one through nine until the IRS issues a clarification on retroactivity, which he hopes will come by the end of 2022.

For many individuals, the most significant change made by the SECURE Act was the introduction of the 10-Year Rule, under which most non-spouse beneficiaries are required to distribute the entirety of their inherited retirement accounts by the end of the tenth year after the decedent’s death. But while the general consensus among practitioners was that such Non-Eligible Designated Beneficiaries would be allowed to distribute the entire account as a lump sum at the end of the 10th year instead of taking annual distributions to empty the account, the new Proposed Regulations seek to implement a system that would require Non-Eligible Designated Beneficiaries inheriting from retirement account owners who died on or after their Required Beginning Date to comply with the 10-year distribution requirement in addition to taking annual RMDs during that period.

More or less, this works out in most cases to forcing an inheritor of an IRA to take RMDs based on their life expectancy for 9 years and then empty the whole account by year 10. There are some exceptions for minors or disabled inheritors or those close in age to the deceased, etc.

the new IRS guidance would require heirs subject to the 10-year rule to take annual withdrawals from the accounts during that period if the original owner died on or after his or her “required beginning date” for payouts. Under current law, that’s April 1 after the year in which the IRA owner turns 72.

For example, say that a 50-year-old inherits a traditional IRA from her 77-year-old mother, who died early this year. According to the new rules, this heir must take annual IRA payouts based on her life expectancy as prescribed in IRS Pub. 590-B. Then she must withdraw the remainder when she’s 60. (She could, of course, take larger withdrawals earlier.)

IRS still no accountability for the Democratic hit job on the Evil Rich. The person responsible has been promoted.

the private tax files of “thousands” of Americans – covering a period of 15 years — had been stolen and given to a progressive news organization. The IRS and the Biden administration immediately vowed to investigate and prosecute.

Yet here we are nine months later with no answers from the government, while Democrats push for even more power for the IRS.

No disrespect intended . . . but no shock, either:

It’s almost ten years later, Lois Lerner remains a free woman, nobody is surprised, the mainstream media is silent on her outrageous infractions, and I have your explanation:

Sweet Lois is a Democrat. Period. That is all you need to know. But, but, she pleaded the fifth you protest!! Shut up. I already told you all you need to know.

Even worse, fast forward to today, Lois is retired and free as a bird, but the Democrats are still at it:

Looks like Build Back Bigger isn’t quite dead, and they’re trying a reboot that Manchin’s not obviously opposed to centered around a new version of taxing unrealized stock profits as a one-time revenue boost. This description is care of WashPo so many of the assertions on legality or consequences are just lies, but you get the general idea of where they’re aiming with this.

The White House plan would mandate billionaires to pay a tax rate of at least 20 percent on their full income, or the combination of traditional forms of wage income and whatever they may have made in unrealized gains, such as higher stock prices.

“Government’s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.”

I’m not sure how they think it would work on billionaires who have barely any income due to borrowing against appreciated assets. Unless they’d seriously warp the definition of annual income to become annual change in net worth. For some, considering the nature of the assets (say they own sports teams, or many real estate properties), that’d require annual appraisals. Maybe it’s doable if you’re talking a very tiny number of taxpayers but it also sounds like it’d open a large can of worms.

Yes, it’s a huge mess to try to tax illiquid assets, or even liquid ones, on transient mark to market gains. But that’s what they’re going to try, and probably set the timelines so they can pretend this is ongoing revenue when it’s really a one time proposed confiscation of 20% of all of the Evil Rich’s paper profits.

That’s another thing I don’t follow. Why would it only be a one-time event? Should it not be an annual thing? What if their net worth drops next year? Won’t they be able to carry forward losses? The whole thing seems half-assed (actually a lot less than half). So I’d be surprised if it goes anywhere beyond feel good PR for the Dems base.

The amount of pork in that omnibus is beyond shambolic. Dems have nobody to point to but themselves for repealing the 2011 moratorium on these earmarks in appropriation bills. It’s just disgraceful all around. Instead of restoring earmarks, they should have banned them permanently like some GOP senators proposed. Really a shame that proposal did not go anywhere. Instead, welcome back to the bad old days of free spending spree on pet project favoring my (donating) buddies.