With the updates from mortgage lenders to suspend payments for 90-days, and perhaps longer, does it make any sense to utilize this option even if one still has a job and ‘for now’ steady income? Everyone is eligible regardless of how much money they make.

1 Like

This is an automatically-generated Wiki post for this new topic. Any member can edit this post and use it as a summary of the topic’s highlights.

Is your bank offering this? I’m not seeing a general mandate that morgages are on hold. Or is this specific to your state of residence ?

I thought the CARES act only offers mortgage forbearance if you’re financially impacted by COVID19

2 Likes

“Financially impacted” is still a bit of a grey line that needs better interpretation IMO.

I have a side online sales business that is arguably impacted. The IRS does a decent job of defining what is impacted but for many businesses, nearly ALL businesses can make the claim that they are financially impacted if you have reduced staffing or cut back hours or reallocate employees to do deep cleaning. What if you have a delay in shipments, that cost you potential or real money, etc?

I’m curious if states or IRS will require any proof of these claims or have the capacity to audit any of them. Or in this case of this thread, banks asking for proof?

They may ask for some kind of proof that your income has dried up. Easy if you have your own business to show that it was non-essential and thus you had to close. Or if you were furloughed - like a neighbor whose son was working at the DMV -, you’d have a letter from your employer that you could provide the bank.

But yes, in most cases, it should not be too hard to find even a small way in which your business was financially impacted. Whether that’ll qualify for forebearance, that’s another question. IRS may give guidance to the banks but they’ll ultimately decide whether to grant it or not.

But for me, there’s also the issue of civic and ethical responsibility. Personally, I’ve been blessed to be very minimally impacted financially (and don’t anticipate any change in the next 6 months) so I’d consider it wrong to ask for being granted 90 day forebearance. To go through the paperwork just to float an extra $5k for 3 months at 1.5% APY to make $20 while others experience tremendous health and financial hardships? Plus what if my application for forebearance slows the system down and delays someone who really needs it? Doesn’t seem worth it for me but it depends on everyone’s circumstances and ethical line in the sand.

8 Likes

I found that US Bank at least wants :

"* A brief explanation of your situation.

- A detailed list of your household expenses.

- Proof of household income (recent pay stubs, tax returns or profit-and-loss statements)."

That may raise more questions than it answers though… If say someone loses their job. THeres no income to provide proof of at that point. Would the “brief explanation of your sitation” simply cover it by saying “I lost my job”. Then “proof of income” is “none”. ?? beats me

In any case they do ask some questions and its not just automatic for the asking.

2 Likes

Makes sense. They’re not going to make it a drive-thru painless process otherwise everybody would go for it regardless of actual need.

1 Like

So how does forbearance work?

So you miss 3 payments, do they then capitalize the interest and tell you this is your new monthly payment?

What about unrealized stock market losses? That’s a financial impact…

Or ordering delivered groceries – that costs more than it did to just go in the store and buy them yourself. That’s a financial impact in itself.

1 Like

Blah… blah… blah… PYBD

6 Likes

I may have been kind of wrong.

THis is interesting if all correct:

What I’m reading there is that the request for forebearance is supposed to be approved without requirement or proof.

So while they might be asking you questions that doesn’t stop it and you don’t have to give them proof.

I assume its costing the bank money to approve you so they stall it with questions.

But it seemss that while you may be required to tell them you have financial hardship as the reason but apparently they don’t require anything else and can’t deny you legally.

Its also saying hat banks are giving 90 day forbearance and acting like thats all thats available. However the mortgage holder can ask for another 90 days at the end of the first and string it on for up to the full 1 year.

Of course things may change in 90 days (lets all hope) and maybe they won’t be required to continue to extend it if things are settled later. But that might actually require an act of congress (literally) since the law as written allows us 1 year forbearance for the asking.

4 Likes

Nice work digging up the details. So basically the banks are dragging their feet. Should have known that if there was a way to comply with the law and make it as painful as possible, they’d zero in on the way very quickly.

Makes me wonder how many banks will “forget” to notify borrowers 3 months later that their payments are due again unless they re-request another 90-day forebearance…

2 Likes

Thanks for the article. Sent to my co-worker. His brother just bought a house very recently and is now furloughed. He is very appreciative.

1 Like

I was just furloughed.

I assume I will be eligible for the generous unemployment benefits that were just approved. I signed up for that and I am waiting for my state unemployment agency to mail me a PIN number. That plus the state benefits will put me at about 85% of my old pay.

I have over 1 year of household expenses in liquid cash.

I have job skills that in a normal market would find me highly employable. (CPA license and internal audit experience)

However, I have worked in government for the past 12 years and all state and local agencies are now on a hiring freeze here. I actually applied for 4 jobs before this all happened, had 2 interviews scheduled with state agencies the other 2 with city agencies waiting. Then s**t hit the fan and 1 postponed indefinitely. 1 went well and they brought me in for a 2nd interview. The next day, my County furloughed me. Good to know that I had the right idea to leave. I was expecting to hear from the state agency that interviewed me soon but the governor announced the freeze literally today.

My wife is a stay at home mom. I’m wondering which programs (like this and other) I should be taking advantage of. Part of me says all of them because there is no timetable for a return to normalcy. The other part says not to bother because of my savings and the unemployment. My only debt is my mortgage. Everything else is just household expenses.

Thoughts?

3 Likes

All of them. I don’t see the point in making mortgage payments if you don’t have to.

Also I think they’re seriously underestimating the number of people who are going to take advantage of this. I just refi’d and my first payments aren’t due until 5/1, I just need to figure out if they’re federally backed… and if these new rules apply to investment property loans or only primary residence.

2 Likes

Sorry to hear about your situation. I suspect you are in much better shape than most given your knack for keeping your finances in shape.

Heck, why not take advantage of this program if you can? I am sure that $2T stimulus bill has others you can discover and use to help you through this.

My wife works for a city government here in WA, and they are still hiring (although, to be fair, they are dysfunctional and had over a dozen open heads before this all went down). I’m sure you’ll find something soon given your skill set.

3 Likes

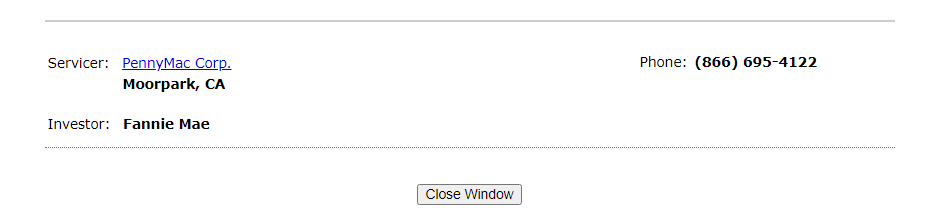

Look up your mortgage in MERS. Your paperwork will have a MERS rider with a MERS number in it. Use the MERS number on https://mers-servicerid.org. The tool will tell you the investor - if it says “Fannie Mae” or “Freddie Mac” you’re good to go.

For instance, ours looks like this:

Otherwise, your loan might not have been sold yet. If you have the standard Fannie/Freddie paperwork in your mortgage docs, you’ll be sold to Fannie/Freddie eventually. You’ll just need to wait (and see if the rules require the mortgage to have been originated before a certain date… otherwise you may be SOL).

4 Likes

I didn’t realize at first this was for federally backed mortgages only. Nothing on the MERS site about Fannie or Freddie for my address. Just my servicer. Oh well, guess I’m out.

The investor will always be listed. Make sure you click through to look at that information - there’s a link at the bottom which states " If you are a borrower on this loan, you can [click here] to enter additional information and display the Investor name."

3 Likes

Oh cool. Thanks. Mine is Fannie Mae. Phew!

1 Like