No I didn’t get the CC.

I actually did not deposit money order often. For a while, maybe 6K / month at max. I only did it once a week, not every day

Which other banks allow mobile deposits of money order? It’s the best feature of ACU.

No I didn’t get the CC.

I actually did not deposit money order often. For a while, maybe 6K / month at max. I only did it once a week, not every day

Which other banks allow mobile deposits of money order? It’s the best feature of ACU.

US Bank allows MO deposit from their mobile app. Beware not to make the stupid mistake I did and accidentally deposit the same MO twice or it may get your account flagged amd shut down

That sucks. US Bank is unfortunately super sensitive to manufactured spending - they don’t like money orders, gift cards, etc. Lots of data points on DoC and elsewhere that they’ve shut down Altitude Reserve cardholders just for gift card purchases.

Back on the Alliant topic… outside of the interest rate, I like using them for checking. The funds availability policy is generous, I like being able to deposit cash at credit union ATMs, and every time I’ve contacted customer service (usually for wire transfers, one time while we were out of the country traveling), they’ve gone out of their way to help. The ACH push/pull limits are annoying, and the interest rate is mediocre, but unless you rate chase and are willing to sacrifice in other areas, it is hard to beat Alliant.

Remember when Alliant CU would allow both ACH push/pull limits of $100k. Yes those were the good ole days. But I do like their checking account. Once I bought a can & wrote a huge Alliant check for the purchase. At that time their savings rate was worth keeping liquid funds. So life goes on!!

Those were the good 'ol days, Patty!

Sadly it’s hard to find a bank that ticks all the boxes. For us, Alliant’s checking account ticks most of them, so we keep our business there. We have CDs and liquid savings elsewhere to maximize return, but for everyday checking to receive our paychecks and pay our bills, Alliant is hard to beat.

In the spirit of “ya gotta have fun with this stuff”:

I had money incoming into my Alliant checking this morning via ACH, and I had my customary $100 in checking already.

Double checked to be certain my Alliant savings was backing up my checking using Alliant’s free overdraft protection. It was.

Moved about $450 to PurePoint, from Alliant checking, at their website. With “instant interest” that gives me four days of PurePoint interest at 1.25%. Then moved those same funds from Alliant checking into Alliant savings. There the funds will simultaneously earn 1.20% APY for a grand total of 2.45% APY on my liquid funds for the four days.

You need big money, tens of thousands of dollars, to make something like this really pay. With my tiny amount of dough I won’t even be making two bits!! But it’s a good exercise, it keeps the mind active, and it’s fun.

Yes, but you did good! Just under the wire. ![]()

But for me I can’t see it.

You talked of moving funds to NFCU on that 3.25% add-on for just a few days interest before the CD matures. Sometimes I think it’s just to much trouble (for me). ![]()

Really that was entirely different. It was more than double the interest, for close to three weeks, on very nearly fifty grand. That was a screaming no-brainer.

This current small money thing with Alliant is just for fun; good practice, though. ![]()

Argyll, not to worry, there is nothing whatsoever amiss with your post.

I would be delighted to make an additional $46. Hope it is that much. Grocery money. In this pandemic delivered groceries are costing me a lot more than prior. $46 would help to offset some of the added cost.

Alliant Signature Visa ended the 3% rewards for one year deal in January. They also limited 2.5% to $10.000 per month.

The annual fee on the card remains the same: $0 intro for the first year, then $99. So it’s 2.5% the first year with no fee, still a very good deal.

For the second year, To break even with a 2% card with no annual fee one needs to spend an average $1650 per month or $19,800 per year on the card.

If you average the annual fee over 2 years, you are paying $49.50 annually in fees for two years, $66 fees for 3 years, $74 over 4 years. It’s $89 a year over 10 years. I’m not trying to diminish the impact of an annual fee, but noting that because of the free intro year, the average annual fee can be considerably less than $99 for a long time.

https://www.nerdwallet.com/blog/credit-cards/alliant-cashback-3percent-eliminated-rewards-capped/

Thanks, Argyll. With my little side hustle, even at the current very reduced level, I can easily reach (and well exceed) that number with just a single “purchase”. And these days there is a lot more than just side hustle buying activity hitting that card. So still a great deal for me.

Now if they reduce the $10,000 max number . . well . . that would pinch a good bit. Hope they do not do so.

shinobi & Argyll, your thoughts are ok. But, I still think my CITI dc card would break even or maybe surpass your card. I get 2% cash back on everything & no fee… ![]()

It’s not a subjective proposition. Do you spend more than $1650/ month (or $20k annually) on your Citi card? If so, the Alliant card will net you more cashback. That’s all there is to think about.

Wow, big changes coming, and they are not good. The generous funds availability policy is a big reason why they are my main bank. I just received the following notice:

Dear sullim4,

We are making changes to the Alliant Account Agreement and Disclosures (AAD), effective July 1, 2020. Sections of the AAD pertaining to the Funds Availability Policy and Deposit Account Rates are being replaced by an addendum, which you can find on the final three pages of the AAD file linked below.

We have included a brief summary of the changes below.

Funds Availability Policy

To comply with recent regulatory changes, we’ve updated our Funds Availability Policy (pages 27-29 of AAD).

Please note that “the day of deposit” means the business day that Alliant processes your deposit. After you’ve made a deposit, you can log in to Alliant online banking or the mobile banking app to check the status of your deposit and the availability of funds for withdrawal.

Deposit Account Rate Changes

The Deposit Account Rates and Fees section (page 7 of AAD) and the Truth-in-Savings Disclosure section (page 31 of AAD) are updated to reflect that savings and checking rates may be raised or lowered at any time of the month.

What so major? They raised the tiers from $200 to $225 and from $5k to $5525. That’s more “generous”, not less.

The only “major” thing is that they’re apparently considering mid-statement rate changes. If you want to stay on top of the rate, you will need to check more frequently than every month.

Funds availability generally refers to paper checks. Who uses paper checks in 2020? It’s not a big deal.

If you are new to the card you get 2.5% back on everything and no fee for the first year.

In the second year, to exceed 2% rewards with the fee you would need to spend $19,801.

.

For us, it’s a bigger deal. We average 1-2 check deposits a month. The larger deposits (> $1k) come from my wife’s employer for out-of-pocket reimbursements. They are a local city that’s… well… backwards in many ways.

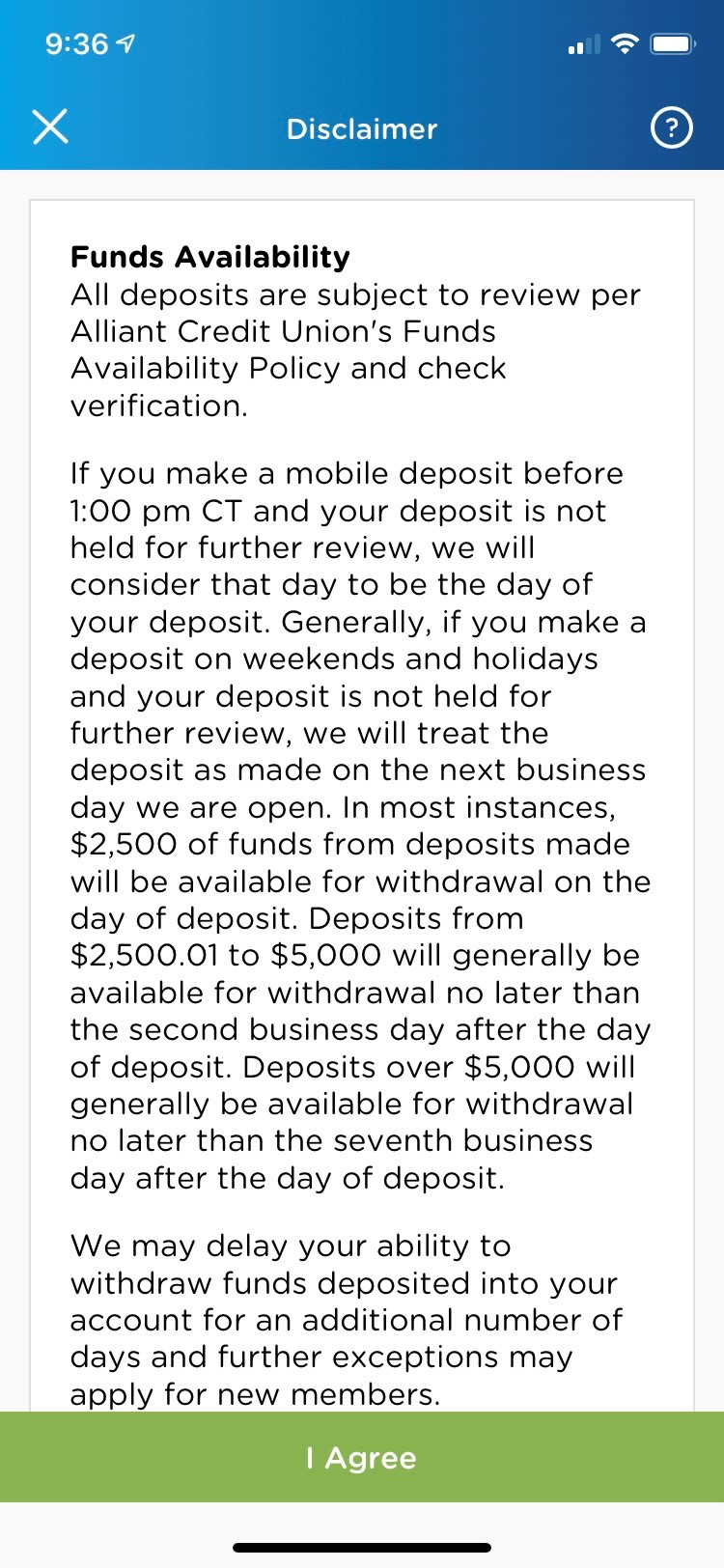

That’s not accurate despite their claim in the email. When I look at the disclaimer in the mobile app, it says, “In most instances, $2,500 of funds from deposits made will be available for withdrawal on the day of deposit.”:

I’ll have to admit that a couple years ago I applied for that signature card & was denied. ![]()

I might try again…