Hi all – I’m new to the forum and I didn’t see much discussion of HELOC’s and Home Equity Loans. Yeah, rates are high which makes them unattractive, but I’m in a high marginal bracket and will be using the funds for remodeling my kitchen and 3 bathrooms, so the interest will be tax deductible for me. I figure even at a 8.50% variable rate on a HELOC, I’m looking at an effective interest rate of about 5% after deducting the interest (about what I’m earning on t-bills). I’m buying an equity stake in a business that I’m apart of (and will be taking some debt on there too – also tax deductible) and I imagine the borrowing rates will be higher than the HELOC/HELOAN rate, so it makes sense to borrow what I can for the home remodel and use more of my available cash to borrow less for the business investment. Long-story short, I think a HELOC or HELOAN makes sense for my personal finance situation.

Any recommendations on where to apply – for best rates, features, or incentives? I’ve never had a HELOC before so this is new territory for me. I obviously plan to shop around but there are A LOT of providers and would like to limit my inquiries to 3 or 4 companies, if possible. Thanks for any help!

Do you have an accountant? I would ask their advice on whether a Heloc is your best option. I’m not saying it isn’t, but they know your finances and may offer options you haven’t considered.

Sorry. I had a HELOC a decade ago, but never used it.

Are you sure about this? It’ll only be tax deductible if you itemize (and if you don’t itemize now but will itemize with this extra interest, then you’ll have to calculate the marginal value of the itemizing as it will not be 100%). Itemizing became more difficult after TCJA doubled the standard deduction (thanks Drumpf!)

That’s why I suggested he consult his accountant. That, and his comment about his investment being tax deductible. I would not count on either being certain, especially the latter.

I thought he said that the business debt would be tax-deductible. Presumably the interest on the debt is tax deductible to the business, assuming the business generates enough revenue against which such deductions could be made.

You may be correct in presuming he meant interest. I didn’t go quite that far and took him at his text - the business debt would be tax deductible. The only way that I’m aware of that being correct, in today’s tax laws, is if the business fails. That led me to believe that an accountant may be better able to explain his options.

Semi-OT: Wasn’t there a similarly named FWF member? Maybe with a number/year in the name? … or is my feeble memory getting even more feeble?

I don’t recall, my memory may be even more feeble.

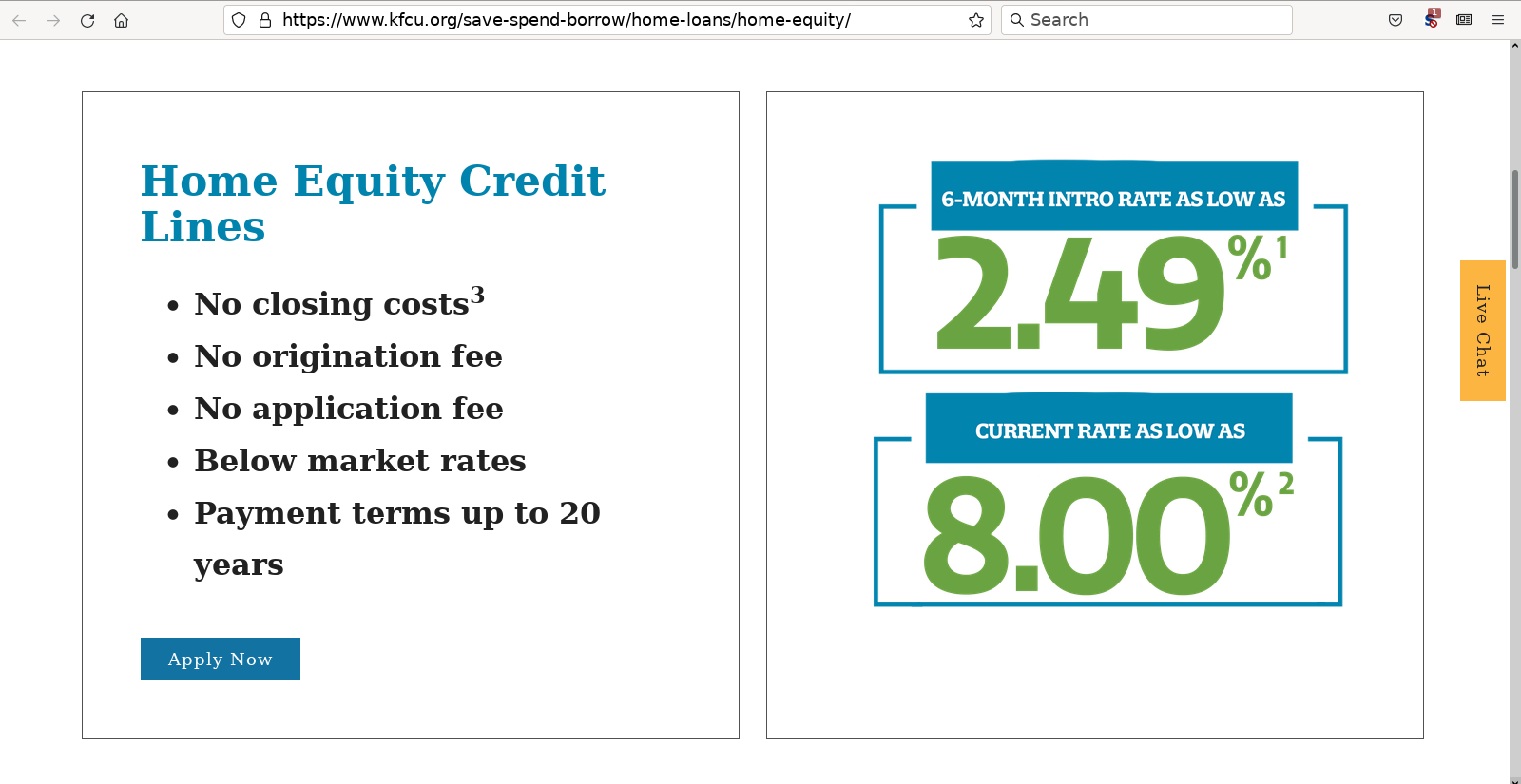

Back to the subject at hand though, I do think it’s a valid topic. I did some searching only to find out that some major banks like Chase, Citi and Discover have stopped offering HELOCs entirely. There’s an article on this at investopedia. I recall that a few years ago Alliant had one of the best HELOC offers and they still advertise one:

Variable APR starting at 8.5%. This is basically Prime+0.25% for those with best credit

10-year interest-only draw period followed by a repayment period up to 20 years

No closing costs or appraisal fees for up to $250,000 line of credit

Don’t know how these terms compare to other HELOCs.

Aren’t HELOCs always variable? HEL(oan)s are fixed, because the amount is drawn in advance, but with HELOCs you can draw at any time within the draw period. Would be bad for the bank to make it fixed for a long draw period. Maybe it becomes fixed after the draw down.

OP, check out Hanscom Federal Credit Union. I have had good luck with them on a few products. I believe their HEL / HELOCs are competitive but definitely compare.

Wow! Thanks, everyone for the tips and thoughtful discussion. Yes, when I said the business debt is tax deductible, I should have been clearer and said that the interest on the debt is tax deductible. In both cases, the HELOC interest and business acquisition interest will be deductible since the last couple years my itemized deductions have totaled $35K (married filing jointly). So when thinking about my after-tax effective interest rate on my debt, it will be equal to: Variable Rate X (1.00 - my marginal tax rate).

I’m in the financial advice business and do my own taxes (and find I often know more about the tax code than manyy CPAs who simply churn out tax returns), so I’m pretty comfortable with my analysis of this situation. Which leads me to wanting to find the best HELOC provider. I think I lean towards a HELOC over a HELOAN since I will automatically benefit if rates decline (although I’m clearly taking a risk should rates continue rising). I also like that I could pay down a HELOC at any time in any amount (and see my payment decline), whereas a HELOAN the payment stays the same even if I pay off a big chunk early (similar to a mortgage).

Thank you for the Alliant and Hanscom suggestions. I will check out both!

Sorry, but I don’t. They just keep sending all kinds of offers since we closed our CDs, and trimmed our share accounts to $5.02. Those CD and savings offers have been woefully inadequate.

ETA: I would expect that to be 10k+, but would get a response in writing before applying. Also, if you don’t meed their listed geographic restrictions, good luck.

You’re comparing the after-tax interest rate on the HELOC to the before-tax rate on T-Bills. That part doesn’t add up to me. Probably your T-Bills are free of state tax, but federal tax likely still applies there.

FYI, Pentagon Federal has a similar option like Hanscom to fix an amount borrowed against the HELOC. Not as important now with rates (likely) falling but a good option in other times.