I still have 4 netspend accounts open. Auto transfer $5 in every month to each account and pull it plus the interest out every 12 months. The accounts were a lot better back when they paid 5% on $5k max but they dropped it down to $1k max.

Since I still have the accounts open and they take very little time to manage or add 1099’s to my return they’re a pretty easy $200/yr taxable income.

Thanks for mentioning the DCU account shinobi, and zzz for the note on the hard pull, which for me is a deal killer and probably why I never jumped on it before.

Thank you Corndogg. And thanks to scripta, as well. So I guess, as with so many other things, opinions vary and the Netspend deal works better for some persons than it does for others.

I have not done the deal personally. My role is merely to remind others that it’s out there. Gotta tell you I just took a gut punch at NBD so right now 5% on liquid dough is looking pretty juicy . . . even with the attendant warts.

But there’s a new one valid through January 5, 2021.

$700 for $50k in Priority Account Package, $1500 for $200k in CitiGold Account Package.

Yeah I was rounding up. That’s the same times I see, 60, then 90, and figuring the 60 is probably actually “2 statements”. There is a separate requirement listed to not downgrade the account before the bonus is posted (the “up to 90 days” part), as well.

Have you sit down & actually figured out the %interest on either or both of these packages? It looks like the money is only tied up for 3 months at the most. Right or wrong?

The numbers are pretty round, so it’s not that difficult. There isn’t a single answer because it relies on an assumption on how long you’ll have the funds there and how much opportunity cost the effort of transferring things around is (if that’s the plan).

1.5 is 0.75% of 200. Multiply that by 1, 2, or 4 (for a year, 6 months, or 3 months, whatever assumptions are chosen). Then add the base interest rate. There, you have the equivalent interest rate… Optionally subtract time/effort/opportunity costs.

You need to figure out the rate of return on the Citi Savings account to get the true % interest.

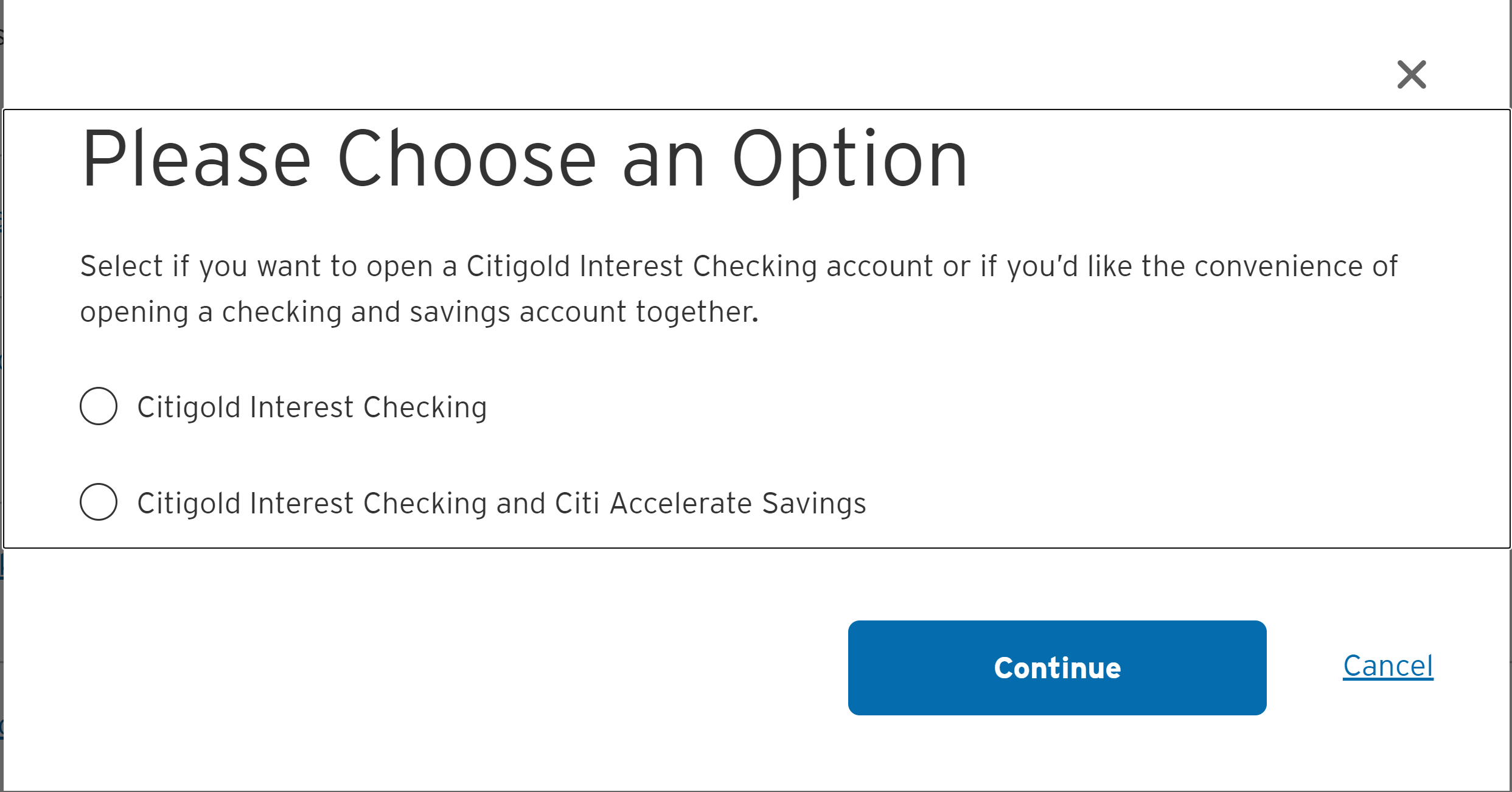

I called and to qualify for the offer, the $50k or $200k need to be in a combination of checking + citi savings. You can open a citi priority package with citi accelerate but then you won’t get the $700/1500 bonus.

You can have a citi accelerate savings account on the side but money in it does not count towards meeting the account requirements for the first 60 days. After that I guess you could transfer to a citi accelerate account (last time I checked it was yielding 1.2% but I’d assume 1% pretty soon considering the trends) and it should qualify for waiving the monthly fee of the citi package.

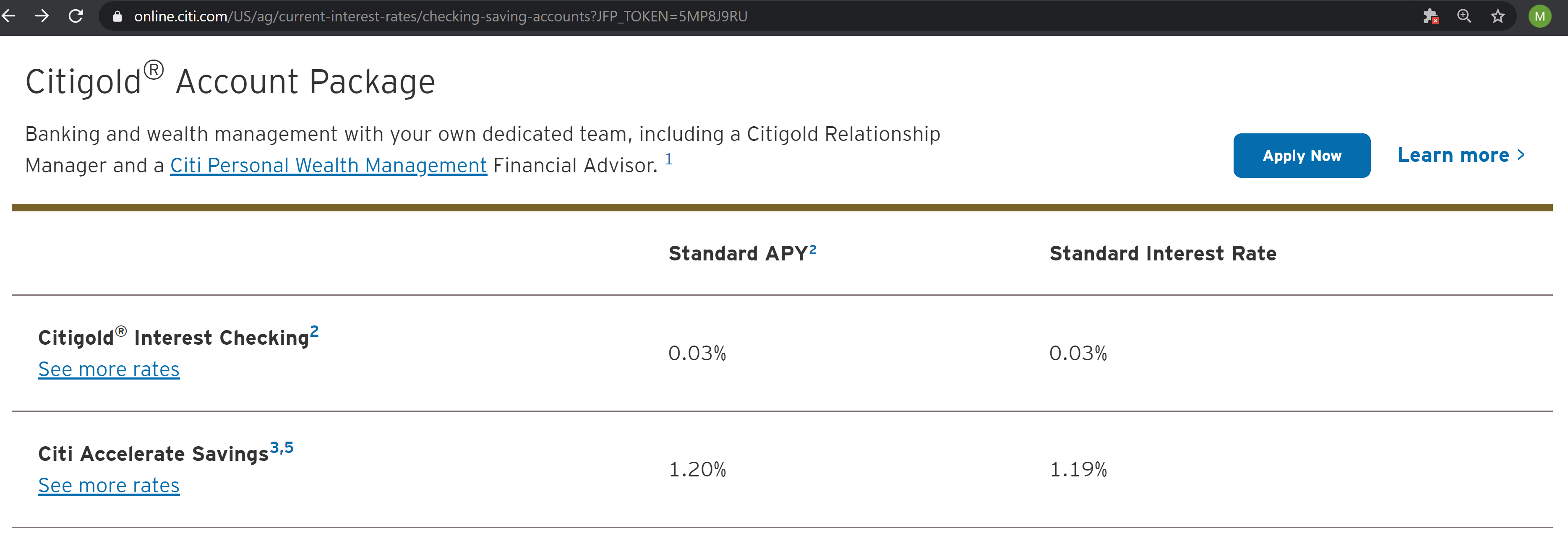

Current rate on Citi savings account is 0.03%. So assuming 60 days at 0.03% on $50k or $200k (which is not worth counting in but feel free to verify), then up to 90 days at 1%, the annualized interest comes out to be:

Citi Priority: at least 3.96% APY: (12/5){$50k x (0.01/4)] + $700}/$50k}

Citigold: at least 2.4% APY: (12/5){$200k x (0.01/4)] + $1500}/$200k}

If bonus is paid in 30 or 60 days, APY becomes 4.95% or 6.6% for citi priority and 3% or 4% for Citigold.

Potentially a good catch for a new terms restriction. See below, I think they may have actually just obsoleted the other types and the phone rep didn’t know what they were talking about.

If i remember the terms from the offer that expired yesterday, I think it had said specifically any savings account would work. Now it says eligible savings account but doesn’t define…

But it does have a line saying “APYs are accurate as of June 3, 2020 Interest Checking APY is 0.03% for Citigold and Citi Priority and 0.01% for the Citibank Account Package. Depending on balances, APYs in Citi Savings Accounts in the Citigold and Citi Priority packages range from 0.04% to 0.15%, and 0.04% to 0.13% in the Citibank Account Package.”

However, if you go straight to the “Rates” page, there is no listing for any other savings account except the accelerate savings within the citigold account package. There is no place I see where they define the account package of having any other savings account options. So, I’m only guessing here that it should still work with the sole advertised savings account… To me, it actually looks more like they removed the more descriptive terms (specifying any savings account type) because they are in the process of obsoleting (or, at least, discouraging) all other lines of Savings Account except for the “Accelerate Savings”.

Definitely should be no reason not to double dip on this if you have $100k available and two potential account holders. In fact $100k/2 accounts returns are better than $200k/1 account in citigold since you only get $100 extra for losing 1% APY on the extra $100k that could be invested elsewhere for at least 60 days.

Yes, @pattyb53 much better than expected. I will be super happy if my 2.22% rate drops to 1.75% next month. I would even be happy with 1.40%!!

For others who aren’t yet Patriot Bank customers. They did maintain their 1.40% rate and extended the rate guarantee for new customers through 8/31/20. After the rate guarantee, the terms and conditions state: “After the promotional period expires, the prevailing rate applies.” I was under the impression the prevailing rate was 1.40% but from what @pattyb53 stated, it actually may be higher for those of us who signed up earlier this year.

Well yesterday combined with today was a slaughter!

Today’s drops:

Communitywide FCU High Rate Quarterly Savings was 1.50% now 1.00%

SFGI Direct Savings was 1.36% now 1.16%

Northern Bank Direct Money Market was 1.25% now 1.00%

Simple Protected Goals Savings was 1.20% now 1.00%

Citizens Access Online Savings was 1.15% now 1.00%

Tab Bank High Yield Savings was 1.10% now 0.90%

Communitywide FCU High Rate Monthly was 1.10% now 0.70%

PenFed FCU Premium Online Savings was 1.05% now 1.00%

TIAA Bank Yield Pledge Money Market was 1.01% now 0.75%(1 year rate guarantee)

Alliant High Rate Savings was 0.90% now 0.75%

Someone may want to reach out to Alliant and ask them if they’re going to change the name of the account given how pitiful it’s become!