What do you mean? What has been reported? If they rejected you based on inquiries as you just said was the case, that isnt something your banks report.

With at least $100k, the Interoir FCU CD is better at 3.14%. I wouldnt think you’d want to split the funds with a 3% product anyways, even if you still had enough to trigger the Interior “jumbo” rate.

Dunno yet. I only just requested a copy of my Chex report this morning. It’ll take prob’ly up to ten days before I have that report in hand.

I did call Chex to be certain I was not a victim of identity theft. They were able to confirm that is not the case. But beyond that was told I must await receipt of my report. They will not release additional information over the telephone.

I have a different take. I like getting back a portion of my dough five months earlier, and do not mind at all accepting a slightly lower interest rate as payment for that benefit. Also, I want a Thrive account.

OK, here is an update for all of you Interior FCU mugglers out there:

Rep just told me rate will hold until month’s end!!

Q: Shin you are aware, are you not, just exactly how reliable the word of a single rep is?

Yeah, I know I know. But it’s nice to post a little good news

With Ken having this deal now, Interior might become swamped. But you gotta figure everyone here is a day or two ahead of the throng. So we have a chance, I think.

Important information for ACH at Interior:

You cannot use your member number when linking for ACH. You must request an account number specifically for that purpose. My member number is eight digits in length. My savings account number for ACH purposes is that same member number followed by two zeroes. So the ACH number is a ten digit number. Also:

Ok Shin, you got all this info.

I’m still waiting for another e-mail. Did you call & put in a rush to get your account #? Because I think I’m approved & they have my photo ID. What’s the holdup for me??

Nope. Nothing special. But I did upload my D/L at time of doing the application . . . at the end when asked to do so. That kept everything together . . all my documentation, I mean.

They seem to me to have a good process. I think you will be fine provided, as I wrote up thread, the special lasts until month’s end.

And the FOMC today having held rates steady mitigates in favor of the special enduring. A rate cut today would not have been a good thing for our prospects of getting any of the ongoing CD deals.

I assume a rate cut is already priced in to the currently available CD deals.

Interesting that you found there’s a need for additional account digits for ACH transfers. The document I received lists “account number” and “routing number” together, strongly implying those two numbers work together. I already initiated an external link to Interior, so I guess I’ll know why it failed if it fails.

Well Shin, I don’t what I did different than you with Hanscom but they are accepting me.

That application was very complete right down to payment info right on the spot. The max is $50K right out of my Alliant CU checking acct. Now I suppose if a person wanted another 19 mo 3% CD, you might be able to ACH transfer later. (really not sure)

Very strange! Actually I just wanted to apply with Hanscom to see what would happen. After reading your experience, getting a 3% CD really wasn’t that terrific…

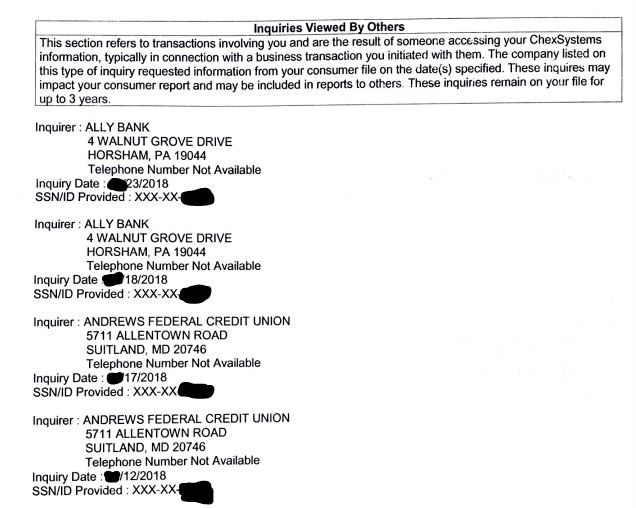

Looking at my own ChexSystems report, I concur that this appears to be accurate. I suspect Shin’s downfall was a track record of numerous account inquiries in a short time.

I believe that is correct, but will not know for certain until my report arrives.

Online research I have done says ChexSystems data includes only negative things . . bad things . . about bank customers or CU members. This includes things like: bounced checks, accounts closed for cause by the bank or CU, outright fraud perpetrated against the financial institution, and so forth. You do something bad at a bank or CU, rest assured a report of your misdeed is likely to be shared with ChexSystems.

But I never have been guilty of ANY of that stuff . . . nothing even close! Yet ChexSystems is receiving reports about me. I need to find out why. Hope once the report arrives I will understand better what is going on.

One other thing:

According to my research, ChexSystems data does not reflect or contain inquiries per se. Not the way a credit report, for example, would. Instead a ChexSystems report is the accumulation of reports submitted to ChexSystems by the various financial institutions where you do business. And those institutions are only supposed to report to ChexSystems if you misbehave.

Your research led you to an incorrect conclusion. When you get your ChexSystems report, you will see that there is an inquiry each time you open an account. If you open three CDs, there could be three inquiries reported from the same bank.

Gotcha. OK, if that’s the case then that is the root of my dilemma. When I had my hustle going full strength I was opening accounts like crazy!! All were on the up and up, obviously. But there was no way I could “spend” money without opening accounts. And I was “spending” money to earn rewards.

I will know more when my report arrives. But it now appears I might have been hustling myself into a dilemma . . . at least at Hanscom. Thank goodness Interior FCU did not hold this against me.

No, with every account you open, the bank runs a ChexSys inquiry. Most do it for new customers, some do it for every account applied for even with an existing relationship.

Those inquiries are tabulated as part of the report that is provided. And some banks/CUs don’t like people who have various banks constantly checking up on them, be it for opening new accounts or whatever other reason (there is no context as to why each inquiry was made).

And I’m going to bet that when you get your report, your reaction is going to be “Wow!”. It can be rather impressive, inquiry activity similar to the “soft pull” section of your credit report, but with the individual details spelled out inquiry after inquiry. Yours may be too thick to be folded into a standard first class envelope …

I have opened literally hundreds of CD accounts. All were great money makers. But it never occurred to me each might individually be being reported to ChexSystems. For God’s sake . . . there was no wrongdoing!! But I will concede this, something I have realized only recently:

When I was young mom taught me to avoid both “evil and the appearance of evil”. That is how she used to put it.

I succeeded in the former. There was no evil or wrongdoing; no cheating. All was out in the open.

However, third party bankers seeing so darn much reported activity can be forgiven for wondering what the heck was going on. I failed to avoid the appearance of evil . . . even though there was none . . . I’m sure especially for anyone with a suspicious mind. Better, they would think, to play safe and keep me away since what I was doing was at best highly unusual. I never saw this coming.

We must all admit that we often do move from bank to bank (credit union). To gain the better deal is our strategy. Is it wrong… I don’t think so!

After reading all this good info, makes me wish I hadn’t gone for that Hanscom deal yesterday. It will only add to my record now… Maybe when a Real Good promo comes along they will look at my record & say…do we really need this gal…

Not to worry, pattyb53. I think you will easily be OK. And you are now eligible for one of those great Trend accounts at 5% APY!!

I wish I had had better luck at Hanscom. It is a great CU which has offered desirable CD deals for a number of years. I very nearly sought to join any number of times in the past. Wish I had applied back then. Now it is too late.

Anyway, cheer up pattyb53. You are in the tall alfalfa.

Unrelated observation:

Looking at Ken’s blog, anybody who wants 3+% on a five year CD has several places they can go to get that rate of interest. It’s not difficult or a big deal.

The rub comes when you are seeking 3%, or possibly a little more, and you do not wish to make a five year commitment, which is a long commitment with a lot of unknowns out there. It is in that shorter arena that USPSFCU, Interior FCU, and Hanscom FCU all get the job done, offering you 3% or a little more without the five year lockup.