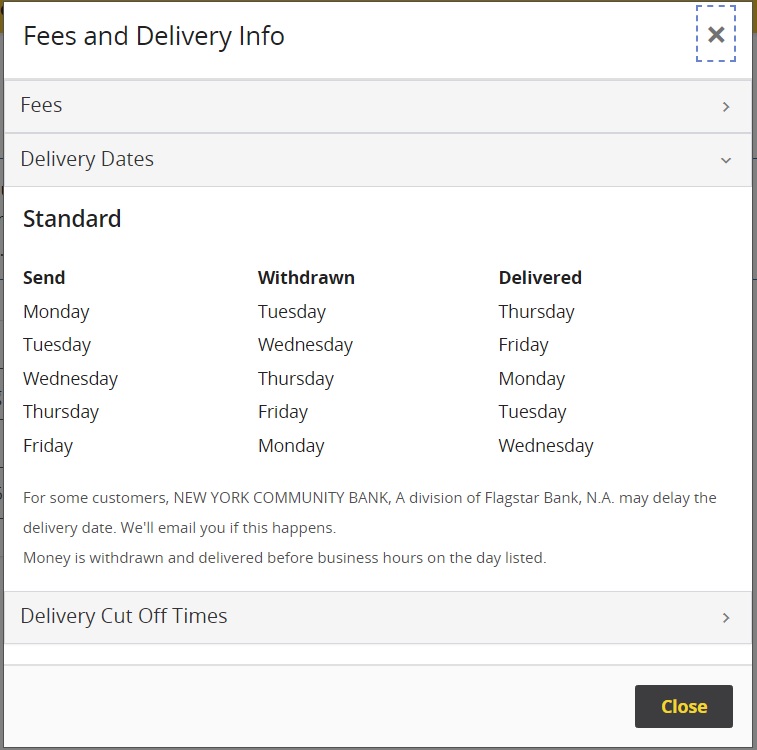

So if I read that correctly, the money is withdrawn on Tuesday and deposited 2 days later. Will I still get interest for Tuesday from the bank it’s being pulled from? Will I get interest on Thursday from the bank to where the money is going to? In other words, am I losing interest for just Wednesday only?

For example, I want to move $100,000 from a 5.25% APY account to one at 5.35% That amount earns $14.38 and $14.68 per day interest, respectively. It would take 38 days at the higher rate to break even for each day of lost interest. Seeing if this makes sense.

Seems to me that this friction is the cost of doing business. It also depends on the receiving institution. Fidelity is particularly good. They start paying interest the day they receive a notice of transfer.

Might consider wiring, but after fees, it’s probably a push or losing proposition.

Pretty much. It’s one reason why many ACH services are “free”.

But there are also banks (although fewer and fewer) who will credit ACH pulls same-day, while the funds arent withdrawn from the source account until the next day. So you double dip earning interest on the same money in both accounts, for a day.

Sounds about right although it seems to me that it’d be a bit longer once you factor in federal income tax.

Assuming 24% marginal tax rate, after tax, you’re only making respectively $10.93 and $11.14 per day in interest, so only $0.21/day after tax in extra interest. Then it’d take about 52 days (per day of lost interest) to break even. You can redo the break even calculation for your appropriate marginal rate but in general the higher your marginal rate, the longer it’ll take to break even (the 38 days calculated would be accurate if you’re not paying Fed income tax).

The new AmEx Checking account does ridiculously fast ACH’s. Like, I see outgoing in outside accounts the same day. I see incoming show up the same day.