I imagine the decision does not happen in a vacuum either. Most people have an amount that they’re comfortable with for their monthly housing payment, whether that’s rent or a mortgage.

Although a lot of people aren’t financial robots and prefer purchasing for non-financial reasons. The “renting is throwing your money away” crowd, lol.

Interesting. In my experience, getting prequalified involved punching in a number I want for a loan into an online form, and then providing some financial information, maybe uploading paystubs and statements, and then the bank pulls my credit and tells me if I qualify or not, very low touch. No lender or loan officer pushing or telling me the maximum of what I can afford. I think Better mortgage was the only company that gave an upper bound.

Getting prequalified is cursory and non-committal and doesn’t usually require all that info. If you provided all the info, you probably got preapproved.

The most you can afford depends on the loan program. The government-backed Fannie Mae and Freddie Mac have the best terms (lowest rates), and they have their own loan limits and rules for how much you can borrow, based on the maximum front-end and back-end debt-to-income ratios. Lenders that don’t sell to Fannie/Freddie (or if you exceed the maximum allowed by Fannie/Freddie) have their own rules. The broker should be able to tell you the maximum you could borrow under any programs available to them, they just need to know your income and debt. Even the most basic online calculators will tell you approximately how much you can borrow given your income, debt, and the interest rate.

Most people, over 23, used to think that way. Over the past couple of decades, many people have bought into (or for the mod folks, “leaned into”) buy the most house you can afford. That was not bad advice for most folks, until the past couple of months. They haven’t really been harmed, so to speak. In about six months, I expect to start hearing an increasing number of calls for “mortgage forgiveness”. One can only hope that Joe “student loan forgiveness” Biden is too distracted to calculate the payoff of that opportunity.

I don’t know that “most” people ever thought that way.

Its also not a new thing with Gen Z.

The housing bubble built up like 15 years ago now and that was fueled by a LOT of people buying more house then they can really afford. Those people are in their 40s at least now.

I think “most” people in the USA aren’t really great with their finances, often live pay check to paycheck even though they make enough to save, don’t make a ton of money and can barely afford houses and/or some combination of all / some of those things. So I think “most” people are more likely to just buy the house they want if the bank says yes even if its more than they ought to spend.

Yes, I don’t recall who I was thinking about with that number. Maybe most people never thought that way. Maybe the people that I knew did, but lots of others did not.

I don’t know about most people not being good with their finances, but there is significant percentage of people who aren’t. Although retirement savings stats aren’t the end-all-be-all that some people claim, it does provide support to your comment.

As for living paycheck to paycheck while making enough to save, you are absolutely right. I’m not sure if it’s ignorance, selfishness, or what, but lots of people who don’t have savings could easily have savings.

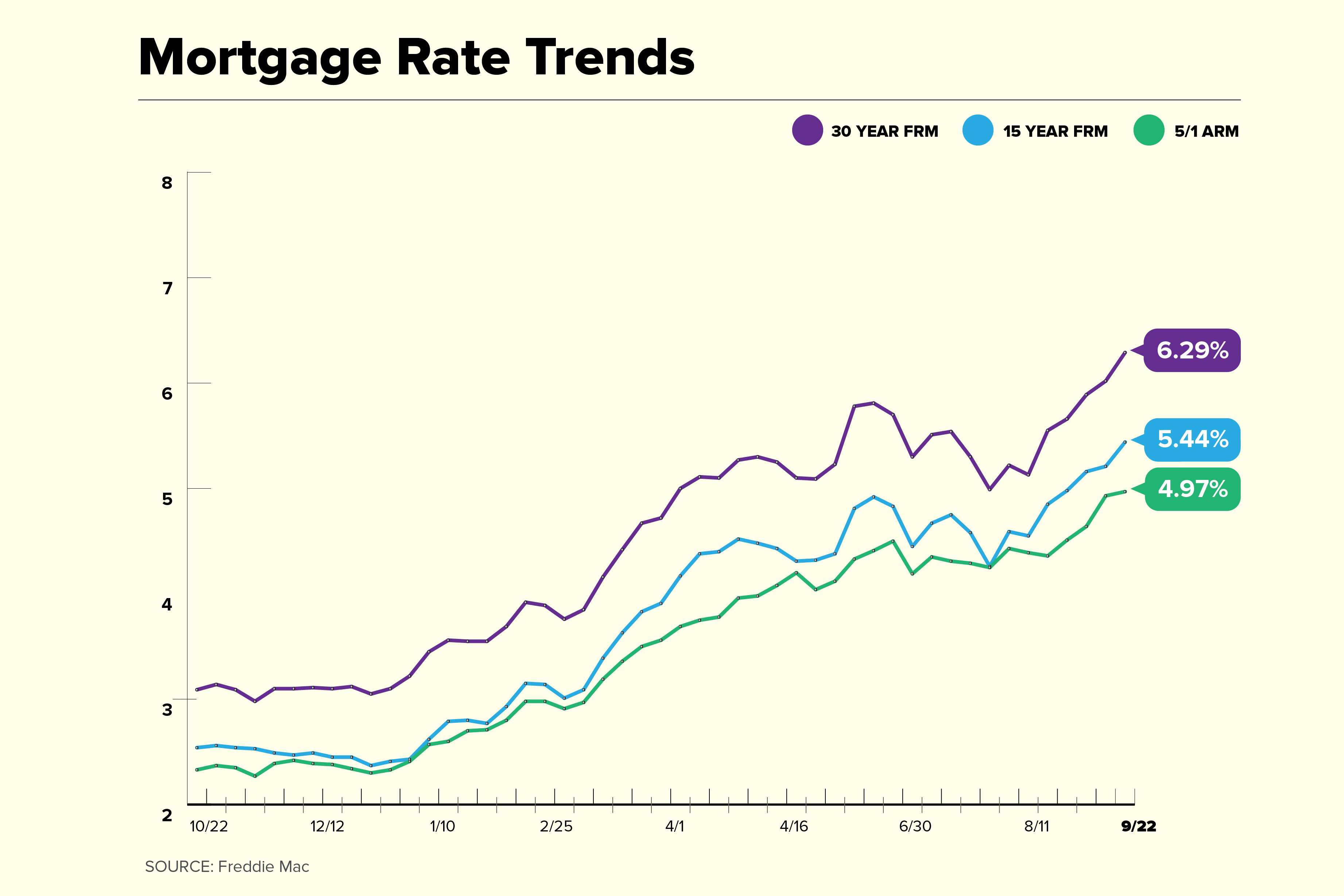

"The housing market is sending clearer signals that the pandemic-driven housing frenzy is coming to an end. Nearly one in five (19.1%) home sellers dropped their price during the four week period ending May 22—the highest level since October 2019–The picture of a softening housing market is becoming more clear, especially to home sellers who are increasingly turning to price drops as buyers become more cost-conscious under higher mortgage rates.” - Redfin (RDFN) Chief Economist Daryl Fairweather.

“While demand is still solid, over the past month, it has moderated from the unprecedented pace of the past 2 years as buyers adapt to higher mortgage rates and other macroeconomic conditions. The substantial rise in home prices, the steep increase in mortgage rates since January, inflation concerns, and stock market volatility are all having an impact on buyer sentiment, and we anticipate that some buyers may remain cautious through seasonally slower summer months” - Toll Brothers (TOL) CEO Douglas Yearley

Rising interest rates are a headwind

“Mortgage rates have quickly gone from being a massive tailwind to the housing market to a massive headwind,” - Moody’s (MCO) Chief Economist Mark Zandi

“…those rising mortgage interest rates will put pressure on potential homebuyers on affordability and that will knock some people out of the market, we can already see that a little bit. Searches on Google for homes for sale were down year over year over the last couple of weeks by 10% plus so it already seems like, from a homebuyer standpoint, some of that cooling has probably started to happen. But then there is this other dynamic that we see. Feel and see quite clearly and that’s just that there’s not enough housing stock in the U S for the number of people who want to own a home and so inventory levels remain very low at this point homes are selling quickly off the market and as a result of home prices are up year over year.” - Redfin (RDFN) CFO Chris Nielsen

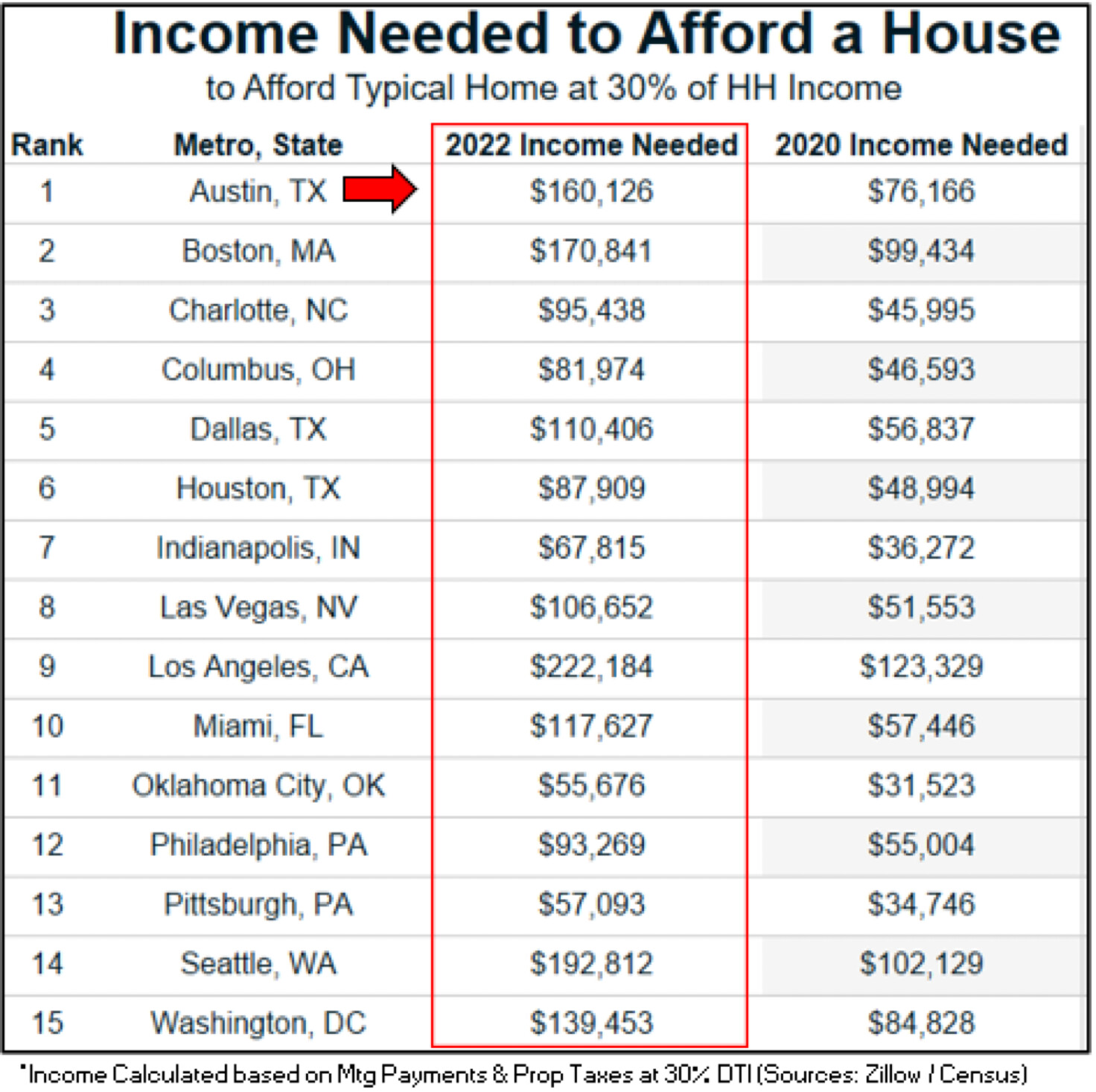

This infographic seems crazy. The 2020 numbers make no sense. How could someone have afforded a typical home in oklahoma city or pittsburgh two years ago making less than $35,000? Or look at one on the higher side. How could someone afford a typical home in DC in 2020 making only $84k? If you would have asked anyone in DC two years ago if they could buy a house that anyone would WANT to live in on an $85k salary, they would have laughed at you.

Pretty crazy data shows how broken the housing market is. The median income in Los Angeles is $65,290. Either housing prices will have to come down rapidly or entire generations will never be able to afford a house again.

Median home price in OKC was still under $200,000 in 2020. Mortgage rates were down around 3% 2 years ago.

Assume 20% down. Thats a $180k mortgage at 3% gives monthly payments just around $760 for the mortgage.

30% of $35k income is $875 per month.

You’d have to pay insurance and taxes too.

For DC a home 2 years ago was around $640k. 20% down and 3% loan gives payments about $2160. Thats about 30% of $86k. Close enough to what they’ve got. Don’t now where they got the “typical” home price figures.

I’m not familiar with the OKC or DC markets so I don’t know which homes people would laugh at. But the ‘typical home’ value is probably the median for the city as a whole. so no, its not the nice neighborhood only…

I guess by household income, they mean take home pay and not someone’s gross annual salary. I can’t see how someone could afford $875/mo (on just P&I) on $35k/year gross. Otherwise, $15/hr isn’t just a living wage, its a wage that affords you a cheaper than median house. Could someone making the “new” minimum wage actually afford a single family home two years ago in Pittsburgh?

But that infographic doesn’t factor any of that in. It’s using the basic formula @scripta is talking about, which is essentially bunk in the real world. If you’re just a single person with no dependents, you don’t get any of the things you are talking about and you actually pay some federal taxes + all FICA taxes.

I bought a foreclosure (below the median price for my area) in 2009 on a cop’s salary. My monthly P&I was right around the P&I for the $200k house in Pittsburgh with the 3% rate. I could barely afford it. I took on a roommate shortly after that. How could someone in 2020 making significantly less than what I was making in 2009 afford the same payment? All I am pointing out is those aren’t real world numbers. I knew couples in DC with double that HH income that had a hard time finding a desirable place to buy years before 2020, and it wasn’t the 1% higher interest rate that was making things hard. I bet if you found a sample of people right now in those localities who had those salaries in 2020, less than 2 out of 10 owned or bought the median priced home in their area.

That’s why I said “new” minimum wage in quotes. There are almost no jobs paying $7.25 an hour anymore, and if you are at the point where you are responsible enough to buy a house, you should pretty close to making the unofficial “fight for 15” minimum wage. These jobs of course weren’t plentiful in the middle of lockdown, but they were right before covid and were very plentiful shortly after reopening.

But maybe that’s part of the issue. It really doesn’t make sense to compare anything to 2020 because it’s such an outlier. I think it makes more sense to run that infographic against 2019. Was it harder to find a $16.83/hr job in 2019 than it is now? Yes. Would $16.83 have been considered minimum wage in 2019? No. But, could you find a job paying that in Pittsburgh in 2019 without a college degree or any sort of specific trade training and only a few years of work experience? Yes. Could a single person with no dependents and 20% down (which would be a ton of savings for someone with that salary) have afforded a turnkey house in a decent neighborhood in Pittsburgh with that salary in 2019. I think that would have been nearly impossible.

Family of 4 with $35k income w/ 2 kids under 17 and 1 income would get about $5600 tax credit from the IRS. So yes they get more than the gross work income. But as meed18 pointed out the graphic does not account for govt. aid.

Is there some way you think that getting medicaid pays for a mortgage ?

Sincere question : Why couldn’t you afford it? Mortgage on that is around $900/mo. How is that unaffordable for buying a house?

What does actual / theoretical minimum wage have to do with it??

I only had 10% down (most people making <$50k/yr will not have 20%), it was a foreclosure, so it needed work immediately, and I had to save for future work it needed (new HVAC a year later). My take home pay at the time was under $1,400 every two weeks. Jumping from $600/mo in rent with several utilities included to $1,100/mo in a mortgage payment (including PMI, taxes, & insurance) with no utilities included was a huge shock to my budget. If I had a significant car payment, it would have been completely unaffordable. I would assume the average $35k/yr worker has a car payment.

Your problem was 10% down and PMI, resulting in a higher monthly payment. But more importantly I don’t believe you bought a median home. The median home in 2009 in Pittsburgh was probably closer to $100K.

I don’t know where xerty got that chart and I can’t easily tell whether it is correct. It does not disclose all the assumptions regarding down payment and interest rates. Simply because it only mentions “Mtg Payments & Prop Taxes” I assume they used 20% down payment to avoid PMI. Obviously income alone is not enough to afford such a house, but that chart illustrates the least difference in income while assuming you can scrape 20% for a down payment.