In my area you’ll need 250k in cash for a down payment on a decent condo/townhouse, which will include 6k/monthly in PITI. I think our HHI is barely over 6k/month net. I started working when the recession hit, so naturally I’m scared to over leverage myself, so it’s unlikely we’ll ever buy if prices are where they are.

I can’t help but see all these people buying up houses though. Do people really have 500k-1M just sitting around to buy a place? I know there’s a bunch of folks making big bucks in tech, some folks living off generational wealth (their residences were purchased 30 years ago), but what about the commoner? How does a family of 4 with two people making 100k/year each afford to buy a house?

I don’t think people are getting loans they shouldn’t, as the recession has taught lenders to be more strict and reject evidence like photos of company vehicles as proof of business ownership. But are people still over-leveraging themselves and not know/care? Or am I just too poor to understand what’s going on?

In my area, $250k in cash will buy you 99% of the housing inventory, without needing any mortgage.

A family of 4 with two people making$100k/yr would also be in the top 10%, too.

I suspect in your area, the “commoners” aren’t buying homes in the neighborhoods that require a $250k down payment. They’re buying “on the other side of the tracks”, so to speak.

And I’m sure for some, their not-so-decent home has also appreciated, so upon selling that they net enough to cover that “decent” down payment.

200k/yr should be much more than 6k/mo net, even if you max out 401k’s/FSA/HSA/etc. But you probably can’t afford 6k/mo PITI. Some markets are just cray cray.

Yeah most people can’t afford $1 million houses. Most people don’t live in those cities. No most people don’t get ineritances to buy $1m homes.

If you do live in a super expensive city then you the options are :

move away to cheaper areas everywhere else, 99% of the country isn’t that pricey

move out just 5-25 miles away to cheaper suburbs then spend all the rest of your free time commuting

rent instead

save up over years to get a downpayment then buy

In your specific area where you’re looking at those $1M homes then theres probably a mix of 3 things: people who bought those homes years ago when they were cheaper, people who make fat incomes, people who saved years for cash to buy in but also make pretty fat incomes. Find the average income for your zip code in question you might be surprized how rich it is.

…or bought any home years ago when they were cheaper, and are now trading up. When selling, that equity may not cover a new million dollar home in full, but it’ll cover most of a $250k downpayment.

From what I’ve seen, large companies make up a relatively small share of total purchasing, like single digit percentages. Investors overall make up a higher portion, but most purchases are people buying primary residences.

The OP isn’t wrong. Housing affordability is out of whack these days, especially for the lower income classes. But cities like NY/SF have always been bad. It’s just worse now

We’re seeing it pretty bad in New Orleans. Housing prices have almost doubled, with the median income more or less the same. Prices are getting pushed up by a combination of well to do remote workers moving in, second homes, and the Airbnb effect.

If this is true that builders can sell new properties at a 50% margin to investment companies, pension funds, etc. to turn them into rentals, why isn’t there a construction boom? If there’s this kind of money to be made into new construction, why do we still have a large inventory shortage? If the money to be made is so good, how come is this not correcting itself due to increased supply from builders?

Like scripta said, the pandemic has caused shortages in staff and building materials which no doubt heightened the issue but it seems to me that the inventory shortage predated the pandemic. We’re not ending up with 5M+ shortage (since 2012) just from the pandemic, are we?

I know it’s empirical and a single data point but, in my market at least, homes have been selling like hotcakes (aka at/above fast-increasing asking prices) for at least 5-8 years because there are so few on the market.

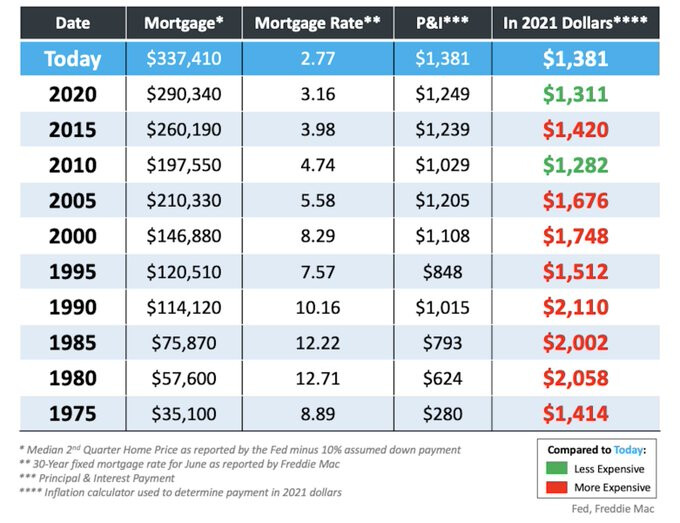

The low interest rates these days are keeping mortgages affordable. Yes those rates won’t stay low forever but they cn still go up quite a bit before they hit the 8-12 % rates many of us paid.

And yeah also it takes longer to save for a downpayments

Single family homes in 2021 increased +20% in the first 3 quarters of '21 vs '20.

I think what we’re seeing now is the long tail impact from the housing bust in 2008. That recession and bust really wiped out the homebuilding industry. They went from building like 2 million homes a year to like 500k.

Also I expect that building new houses is not something you can turn on/off quickly and it can take a long time to plan construction.

I would expect that today any home builder is building as much as they can as fast as they can without over extending.

That looks like it, but I didn’t realize it was that long ago. Time flies when you a̶r̶e̶ ̶i̶n̶ ̶a̶ ̶p̶a̶n̶d̶e̶m̶i̶c̶ can’t remember you’re in a pandemic.