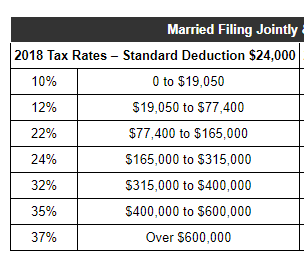

Additionally, the $2k per child tax credit starts phasing out when your income surpasses $400k, and phases out $50 for each $1k earned until your income hits $440k at which point it is completely phased out. Note that the phase out is per child, so if you have 3 children you’re actually losing $150 worth of tax credit for each $1k income. That’s effectively a 15% extra income tax on the first $40k of income above $400k. Combined with the 35% tax bracket on income > $400k and you’re looking at an effective federal marginal tax rate of 50%. Definitely not pleasant.

Now my question. So far this year we have about $397k of taxable income. The regular earnings from W2 jobs will take the total for the year to around $430k of taxable income. A very high percentage of that income will simply go to uncle Sam. I already am maxing 401k, is there anything else that can be done to avoid this large tax hit on the rest of the earned income coming in 2018?

There are a lot of these very high rate phase out sections of the tax code. AMT is another, if you get hit with that, as the AMT exemption phases out (although AMT is harder to get with the SALT limits for 2018+).

Generally you want to be under or way over these. For a regular salary job, you don’t have much flexibility to defer income besides your (and maybe your wife’s) 401k. Some companies might have deferred comp plans, which are basically like big 401ks with a bunch of extra admin and actuarial nonsense thrown in. You might have a choice for when to take your bonus, or to split it across tax years. Realizing taxable capital losses might help a little if you don’t also have more capital gains.

Bunching up income to be way over and somewhat under these phaseout income levels, vs just a little over each year, would be a gain if you can manage it. Likewise, bunching up deductions in the opposite years as your high income works similarly.

Agree with xerty. At about 500k-525k gross income, unless you and your spouse are doctors/lawyers/similar professionals, I’d be surprised if you didn’t have some sort of deferred comp arrangement available to you, though it may be too late for this year.

If you can switch to an HDHP by December and pick up the HSA deduction, you may want to do that, if you haven’t already taken advantage of that.

Just want to also point out that most credit phase-outs are based on AGI, not taxable income. I’m not specifically sure about the new child tax credit, but I’d be surprised if it was based on taxable income. You may have meant that you’re at $430k AGI, but if you’re at $430k of taxable income, you’d need to knock it down pretty far judt to get below $440k of AGI.

ETA: You may also want to look at the effects of filing separately. But if you do this, be sure to consider other repercussions, including taxes at the state level, underpayment penalties, etc.

If nothing else, shift a few donations to this year with appreciated assets(like stocks) to a charity to get just under 400k?

For example, if you’re at 50% effective marginal income tax and if you have a stock with high gains, it would work out as follows:

$100 donation (300% long term gain, $25 basis) works out to:

Deduct $100 @ 50 $35 = save $50 $35 in taxes. Avoid paying LTCG of 15%+3.8% * 75%(“gain” portion) = $14.1 saved taxes. Net cost for the $100 donation = $35.90$50.90 post-tax. Pretty good 3:12:1 return if you get value from helping others. If you also have a state tax of say, 8%, then the net cost for a $100 donation = $27.90$42.90 post-tax. I am not on a soapbox here saying to make charitable donations or not. But if you do regularly make them, you should really look into appreciated assets rather than payroll or cash deductions if you aren’t already going that route.

OT: Seems like this is how some rich people scam us all and don’t pay their taxes – They donate to a charity they control and then illegally derive benefits from that “charity” without reporting the real value of benefits received. Add that to games with fake cost basis and appraisals that recent articles have said are common in real estate, and wow! seems like really crazy “opportunity”.

Edit: as pointed out by OP, I didn’t catch that phaseout isn’t affected by the deductions. Left the appreciated donation example because it’s still better than cash donations but it doesn’t apply to having an extra “bonus” from the phaseouts since they’d still be there…

My original post had some imprecise statements which has added confusion.

The child tax credit phaseout is indeed based on AGI(well actually MAGI) as Full_Disclosure has pointed out, and that’s very difficult to do anything about. Shifting charitable contributions is not helpful in this regard.

The tax brackets are based on taxable income, and many deductions can be taken from AGI to lower this number, but again it’s not really helpful for purposes of avoiding the child tax credit phaseout which is the biggest penalty.

I expect to be around $430k AGI by end of the year. Taxable income will be lower due to various deductions(SALT, mortgage interest, charity, etc.)

This is probably pretty rare. Private foundations have very strict rules on transactions with certain parties. I think most people who set up private foundations are doing it genuinely. That’s not to say that the individual/ family doesn’t benefit, they definitely do. Donating a large sum of money, even through a private foundation, can get those individuals in rooms and conversations with people they wouldn’t otherwise have access to. This can certainly benefit them in their business pursuits, and make them even more money. But I really don’t believe that many people are skimming money from their own foundations, etc. To be sure, this does happen (art “museums” and things like that), but this isn’t really the way that the uber-wealthy decrease their taxes that people may find objectionable.

Only way out of this is lowering MAGI which is hard and depends on employer offerings too.

Make sure you max out 401k up to catch up contribution limit if over 50 or if turning 50 next year.

If applicable (you have access to decent HDHP), look to fund an HSA up to $7k (per married couple).

Even with HSA you can also setup an FSA for dental and vision expenses if you expect - or have been postponing needed dental/vision work for a while -.

If any kids are 12 and under and both parents work, you could fund up to $5k in a dependent care FSA to pay for their summer camps (not overnight ones though).

Finally, you could look at harvesting stock market losses (beyond your capital gains) to lower your MAGI by up to $3k IIRC.

But that’s about all I can think of if your income is from regular salary.

My apologies for reviving this old thread, but I thought I’d post to clarify. I know you mentioned that your AGI will be $430K by the end of the year, but are you really talking about your AGI or about your gross income?

I ask because a ton of people say “AGI” when in reality they’re referring to their gross income. When people say “I make $X,” it’d be very odd for them to be referring to their AGI, as two people with otherwise identical gross incomes can have very different AGI’s just because one of them contributes to his/her 401(k) while the other one does not.

If your gross income is $430K, then your AGI (and, from your description, it sounds like your MAGI will be the same as your AGI) will be way under the $400K childcare phaseout threshold, as the AGI is calculated post 401(k) contributions, post FSA/HSA contributions, post employer based health insurance premiums paid on a pre-tax basis, etc…

Gross income is higher and includes other income that goes towards 401k/FSA/healthcare/etc. as you stated But really there is not THAT large of a difference between gross income and AGI, $18.5k for 401(maybe * 2 people)k, $7k max if you do HSA, $1k- $2k for pre-tax health premiums. It’s very conceivable that if one did have a gross income of $430k that their AGI would still exceed $400k.

Because it doesn’t help at all to reduce AGI. The child tax credit phases out based on AGI. Charitable contributions only reduce taxable income, not AGI.

I agree that it is quite conceivable, but, assuming that both people work and have access to 401(k)/403(b)/TSP’s, etc…, this would be incredibly easy to avoid. Each person’s maxed out 401(k)/403(b)/TSP’s would alone drop the $430K gross income below the $400K AGI childcare phaseout threshold. In addition to the HSA/healthcare FSA and the healthcare premiums that you’ve mentioned, there’s also a $5K dependent care FSA, as well as any other cafe125 pre-tax payroll deductions that you may be able to take advantage of. Some employers may also set up various forms of pre-tax profit sharing, etc…

Hence, depending on the particulars, the difference between your gross income and the AGI could be in the six figure range. In your situation, however, if your AGI/MAGI, as opposed to your gross income, is actually $430K and you have no ability to defer any portion of that income until next year, there’s probably nothing that you can do to avoid the phaseout.

The phaseout is working differently(better) than I had expected it to when I took a quick glance at the worksheet in turbotax last night. With 3 kids, I should expect the full $6k credit if income <$400k, and was expecting $0 if income > $440k. However, that’s not how the worksheet tells you how to calculate it. The 3x$2k child credits do not phase out simultaneously. Only the first $2k credit phases out between $400k - $440k, the second child’s $2k credit phases out with income between $440k - $480k, and the 3rd child’s $2k credit phases out with income between $480k - $520k.