As I indicated, that was a quote from the article listed above it. I did not personally say any part of that.

That being said, Book value is determined by the assets of the stock divided by the outstanding shares yes? If they buy back shares then there are less outstanding shares therefore each one is worth more from a book value standpoint? Let me know if I got that wrong.

I personally do believe alot of people are going to jump on reits because they have not yet recovered from covid AND they have the higher interest rates along with being based on real assets and not hype (tech stocks…coughteslacough) When a bunch of the average joes starts buying it’s going to push the stock price up. In the meantime draw down the dividend.

If you want a safer alternative stick with T, PRU and ENB…7% returns and long standing companies with good dividend history. T is controversial however with some folks swearing it’s going to have short term pain and possibly long term if they don’t get their act together. It’s stock price has pretty much been a flat line for decades with only minor changes but it paid it’s dividend every year and I think they will fight hard to keep their dividend aristocrat reputation.

Also to put things into perspective all the stocks mentioned add up to 10% of my retirement portfolio with the other 90% in a retirement portfolio that has alot of low cost vanguard etf’s. While it has decent capital appreciation it was hit hard by covid too before recovering which certainly influenced me to look at dividends more closely. If the process works as expected I’ll be transferring funds to the stocks from the retirement portfolio. I’m not in a rush.

That’s correct, but the slightly increased book value does not have a direct effect on the price of each share. The cash money spent on buybacks disappears into the ether. Paying out dividends returns the money directly to investors.

I do agree that buybacks may make sense when stock is obviously and significantly undervalued. I just don’t believe this to be the case with most buybacks. I have watched companies spend hundreds of millions of dollars for many years buying back shares while the prices of those shares kept decreasing. They would have been better off holding on to cash or paying out dividends.

In the case of these reits most were knocked down 60-80% when covid hit. Those are the ones I grabbed with both hands. The dividends are just gravy, I can wait a few years for them to recover if that’s what it takes or even longer as long as the keep the dividend. As one person on seeking alpha put it…think like a landlord when it comes to reits. Anyway I’ll keep folks updated on how things are going every so often. all my cd’s were 4 or 5 year ones so they will continue producing the 3.5-4% they were locked in at. The excess funds not used for everyday life will be invested…and probably the dividends until the cd’s start maturing.

I question this statement. The principle is insured, not the expected interest earnings. And they’re borrowing to buy the notes - so that interest expense means they still lose money with every default. And it’s quite unnerving to be investing in 2% mortgages; there’s very little room for their borrowing costs to move before holding a note is costing them more than it’s earning.

There’s a reason REITs have historically paid a high dividend rate, their ongoing profitability is anything but “safe”.

If anyone has a spreadsheet that will break down into monthly income (keeping in mind some stocks pay at different times/months) I’ve love a copy. No joy on googling so far. There is an android app called “Dividend Flow” that does exactly what I want but the author limits the free version to 10 stocks. If you want to do more you have to subscribe to a monthly service. Now I don’t mind paying a one time fee but i’m not paying this joker $3 a month just to be able to add more stocks. It offered other features too but only 1 really was something I cared about.

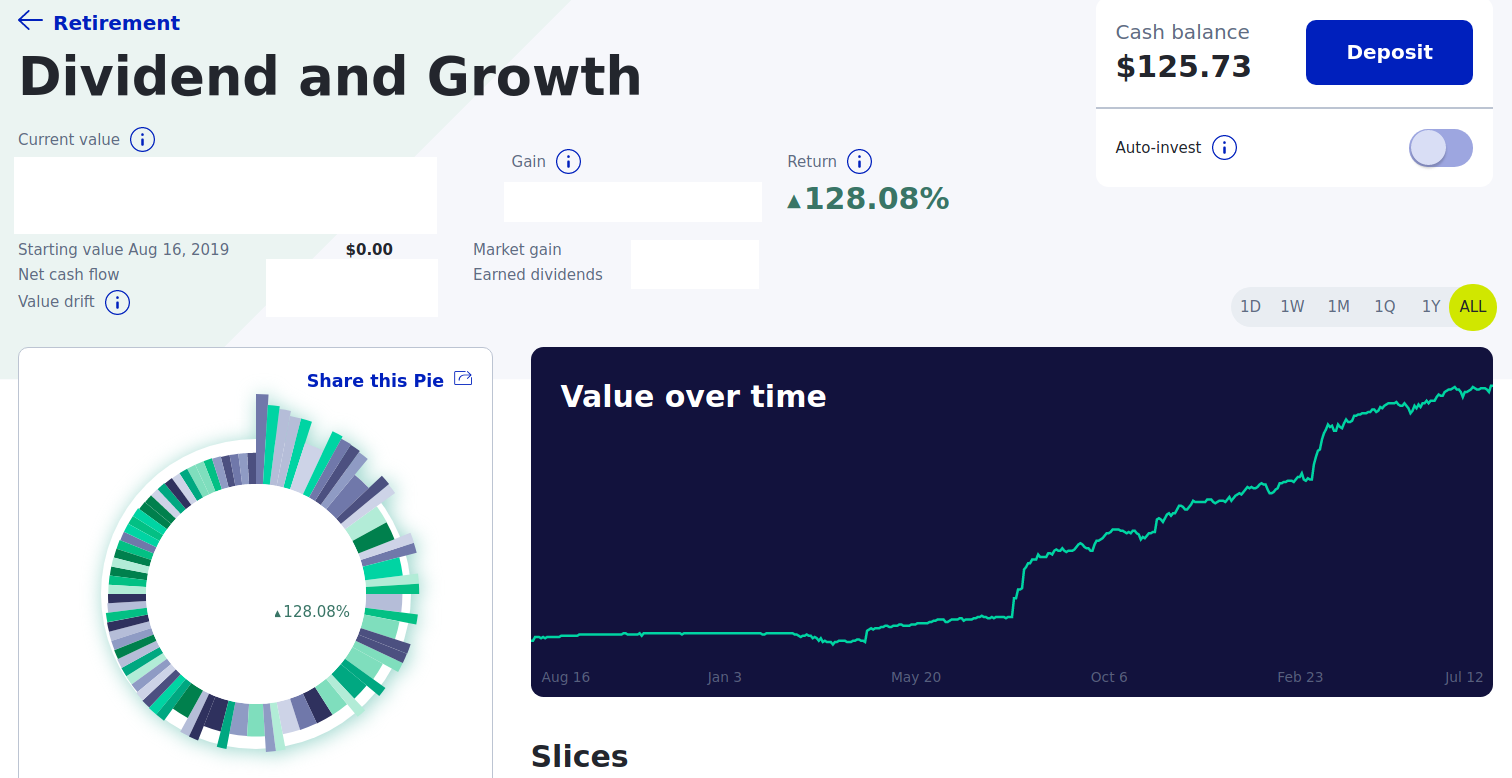

The pie/portfolio I’m using is now up to 50 stocks…most dividend payers of 5-7%. Many are reits that were down 60-80% in value and have high dividends as a result. They offer short term pain but long term gain both by value and dividend. Also some utilities that pay dividends as people always need electricity, water and natural gas…ditto visa, mastercard etc…to see all 50 stocks click the link.

As an update, that pie link should auto reflect any updates I make to it in future so I’m not going to be posting additions here. If you have questions feel free to ask me and I’ll do my best to answer. I’ve targeted dividend stocks, reits and utilities primarily with a few growth stocks. I’ve gotten the monthly income level up to where it can supplement my other income sources. The market recently took a hit but if you are looking at the long term that means it’s time to buy the undervalued stocks which is what I’m doing. I add a little here and and little there…sometimes to specific stocks or I just add to the whole pie and let m1finance’s algorithm target the stocks that are below the % I set. The stocks tracking spreadsheet I posted previously works pretty well to provide info on your portfolio.

If you want to play without investing real money try a stock market simulator and see how you would have done. Stock Market Simulators: Play Your Way to Profits I suggest you stay away from trying “day trading” as alot of people, many using robinhood have been burned. Buy quality stocks that pay a decent dividend and let the ride.

Hey, I own some mortgage REITs. I don’t object to them. But there’s a reason their yields are so high, they’re anything but safe.

You remind me of CN47 (I think?) on Fatwallet a decade+ ago. If I’m remembering correctly, he had a similar attitude and pretty much went all-in, then suddenly crashed hard.

I never gave two craps about the portfolio. I was only commenting on your declaration that this one particular stock was “very safe” because of a government guarantee. I don’t know how I could’ve been any more specific about the issue.

It could work out just fine, but it’s anything but safe.

Perhaps you should tone down your irrational exuberance a bit, since you are continuing to react to that single word of caution a month later.

There was no “continuing”. Today was the first I saw your post. I’ll do one better. I’m done posting here. Feel free to post whatever you want. Admin, please delete my account since you apparently do not provide me the method to do so.

I would have requested via email but you have not configured the forum/mail setup correctly.

Message not delivered

Your message couldn’t be delivered to admin@fragiledeal.com because the remote server is misconfigured. See technical details below for more information.

The response from the remote server was:

I know healthcare, data reits did okay but how are college reits doing okay these days with some being shut down and online only? Do they own the college campus or student housing?

Also, I like O, SPG but I don’t look much at mReits.

Moving onto the lower risk alternative topics. What do the people on here think of preferred stocks? PFF that throws off 5.5+ Div per year… it’s relatively safe and has been mostly stable…

Why is it my job to work to make an impression? I’m not getting anything from it. From April 2020 to April 2021 I made a 50% return on my money and in the end that’s the only gratification I need. I have no need to argue with people that can’t understand basic logic…the same logic Warren Bufffet and many others have followed. Warren Buffett once said that it is wise for investors to be “fearful when others are greedy, and greedy when others are fearful.” After the covid stock market crash in march 2020 you could have thrown a dart at a list of stocks and more than likely picked a winner…everything was down. I took the funds from two cd’s that expired and in a years time I made a 50% return. I could bury it in the backyard for the next 30 years and still beat the interest rates people are getting in banks now for cd’s. 7 year 2% cd? I don’t think so. I invested in non popular sector’s such as Reits and energy funds as well as some utilities. Heck I’ll even post my current shopping list from most recently mentioned by the authors I follow I consider reputable.

Stock Shopping List:

VICI

UMH

O

MPW - Fair Value in <$30 range

UVE

CWEN.A

UNIT

STAR,

BRMK

PLTR

VST

TEF

OHI,

NWE

FE

CXW*

FSK

-UNM 3.9% dividend. Serious Upside potential.

AMGN

STAG

NNN - Buy Under 55

I’m not here to restart this debate. I came back solely to remove some personal information from the thread since I was unaware fragiledeal.com is publicly viewable without being a member. I emailed the admin requesting this but got no reply.

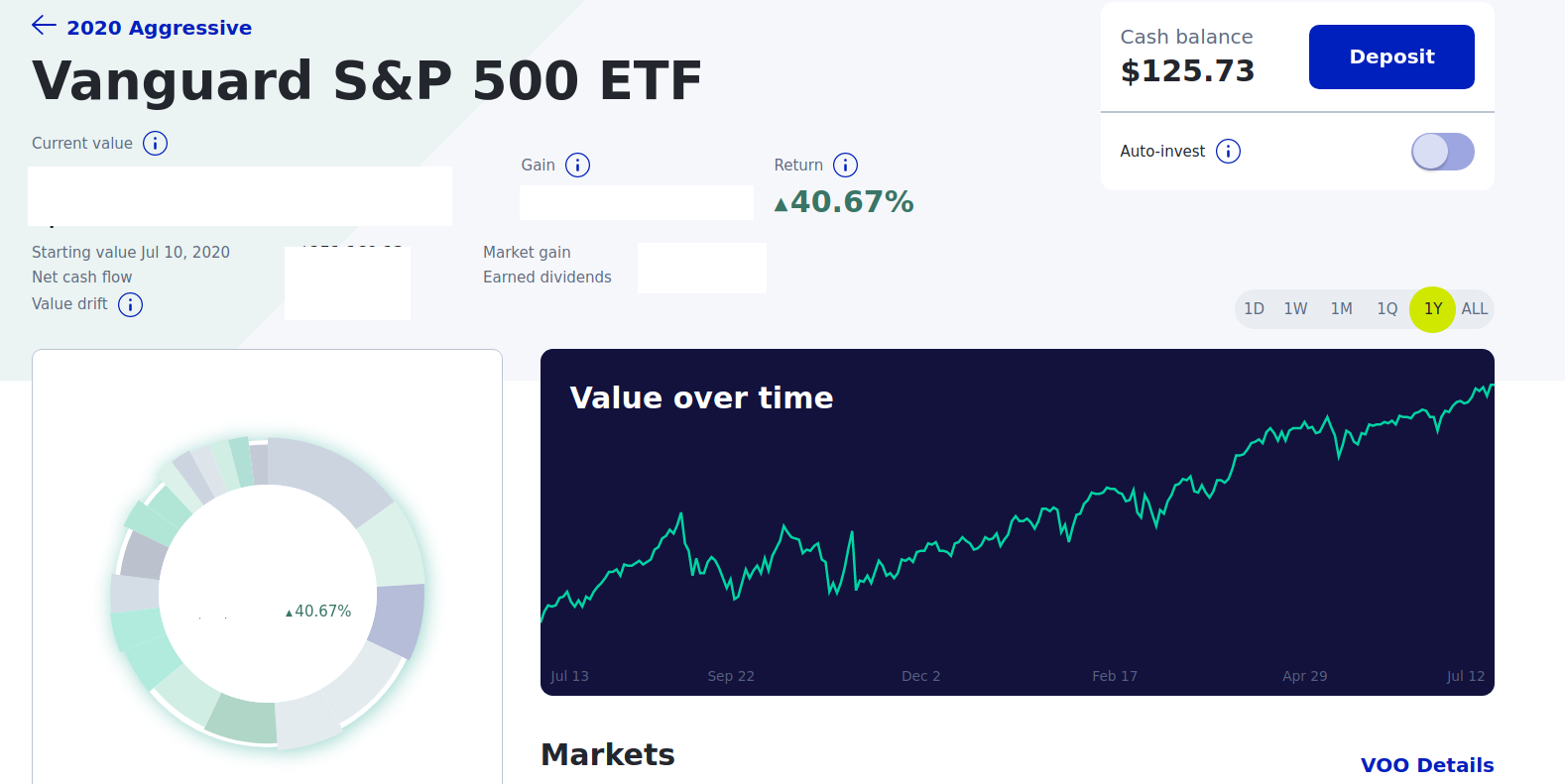

Hey Famewolf, If you just bought the SP 500 in April of 2020, I believe you would have made more than 50%. I think the number is more like 75%. Seems like a lot less work than what you did.

Try again. The percentages shown in both screenshots is a Money Weighted Return which factors in when the funds were deposited rather than assuming the whole lump sum was present day 1 like your assumption does.

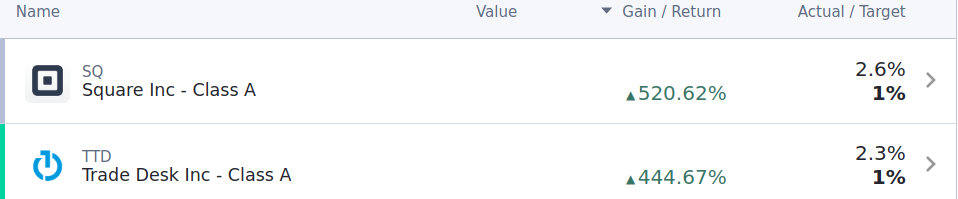

Since I don’t know when you deposited the money, it would have been impossible to replicate the return you made as compared to the SP 500, so I used April 1 2020 as a starting point (which is what your post implied). Out of curiosity, over what period of time does the 520% and the 444% return for SQ and TTD represent? I guess the point I am making is almost anyone dabbling in the market would have made a lot of money this past year. What would be more impressive is making outsized returns in a flat to down year.

Anyway, don’t get offended because I am responding to you. It’s great you made a lot of money. I am happy for you.

My own portfolio which is completely passive (because I’m lazy) gained just over 70% from April 2020 to June 2021 so I can buy that someone buying hand-picked value stocks in April 2020 could totally do north of 100% when almost all stocks were greatly undervalued. But it’s harder by now to find good value stocks after such a rally. I’m probably too lazy - again - to follow a methodology like yours but I appreciate you posting it. Just out of curiosity, how much did these stock pay in dividends?

My only interest in low-risk income alternatives to CDs is where to put my small emergency fund. I reluctantly accept low returns in exchange for some liquidity and stability in value but only currently earning 3.3% in …a 5-yr CD /sigh. But I’d love to be able to do better than something just keeping up with inflation even for emergency fund. I don’t trust P2P lending for that but curious if dividend stocks would have been satisfactory for this purpose say to last me from April 2020 to now? And if so how much would I need in them to generate about $100k income/yr?

I purchased and posted an article by the motley fool that suggested buying Tradedesk, Square and Alteryx in April 2020. The performance is from that time. At one point this year I pulled all the money I initially deposited and put it in other stocks leaving the remainder which continued to grow. If I’d left the initial amount in it would be even better but I’m hardly complaining.

@Shandril Most of the dividend stocks were 3% or better. Although I do have 6,7 and even 1 10% Unless it’s a dividend aristrocrat that’s been paying for a long time I wouldn’t try to push to much higher than 3-4% as the the risk increases. AT&T just cut their dividend and lost their Dividend Aristocrat title for example…they were paying 7%. Initially I setup my portfolio to provide dividends for income and the growth was just a bonus. I did have a few growth stocks such as TTD and SQ in the mix. After the recovery I’m still picking up some reits with solid fundamentals and have not yet had their own personal recovery for one reason or another or picking out of favor stocks (tech is now one of the out of favor ones for example). I get alot of good ideas from Motley Fool and Seeking Alpha. If you see the same stocks popping up over and over from multiple motley fool authors it gets my interest…on seeking alpha I have some fav authors I monitor that do real analysis. Their picks have been consistently good. HYL (High Yield Landlord) and HYI (High Yield Investor) are both the same group of people but the first targets reits and the second targets more general stocks.