We just closed a refinance with American Neighborhood Mortgage Acceptance Company (AnnieMac) and it wasn’t too bad of an experience. It was a little frustrating working around the holidays, but that was my fault for waiting until mid-November to finally pull the trigger on the refinance. They were a little slow in processing some things, but they had the best overall rate and negative points for our situation. I found them on Zillow.

I contacted a bunch of companies/banks and several would not do negative points or they were just more expensive overall. We finally got 2.875% on a $210,000 loan with a computer appraisal of $300,000 in TN. For that rate, we got -1.8 points which covered the closing costs and $500 of our prepaid taxes. Our lowest credit score was 793. Got rid of PMI after two years and dropped our rate by 1.125% so overall we are happy with it.

This is probably a stupid question, but I refinanced about 3 months ago @ 2.875% and the same broker I used is offering 2.5% now. Is there a timeline on when I could kickoff another re-fi? Is there a section in the seemingly 500 page closing package I got that would spell it out? I was under the impression you could do it “anytime” but other folks are saying 6 months…

Did you ask the broker? My understanding is that if you refi sooner than 6 months, then somebody (the last broker or lender) will incur a penalty, so nobody does it. But I’ve also read that 6 months only applies to cashout refi’s.

The 6 months count starts either from the closing date or the first due date, I’m not sure. Last time I was asked if I’d made 6 payments (which means it could be 7 months after prior closing if it included almost a month of prepaid interest and you “skipped” a mortgage payment). If the 6-mo count is from closing, then you can start the refi process at 5 month with a 30-day lock, or at 4 months with a 60-day lock (that way it closes at the 6 months mark).

4 years ago when I last refinanced (I still need to do it again now…), was similar and 6 payments is what they wanted. Not that it delayed things. But I was refinancing with the same lender. With my approval they extended the lock to 90 days (at their cost) to avoid incurring a penalty on the old origination.

I’m gonna bump this because I am again seeing pretty decent rates.

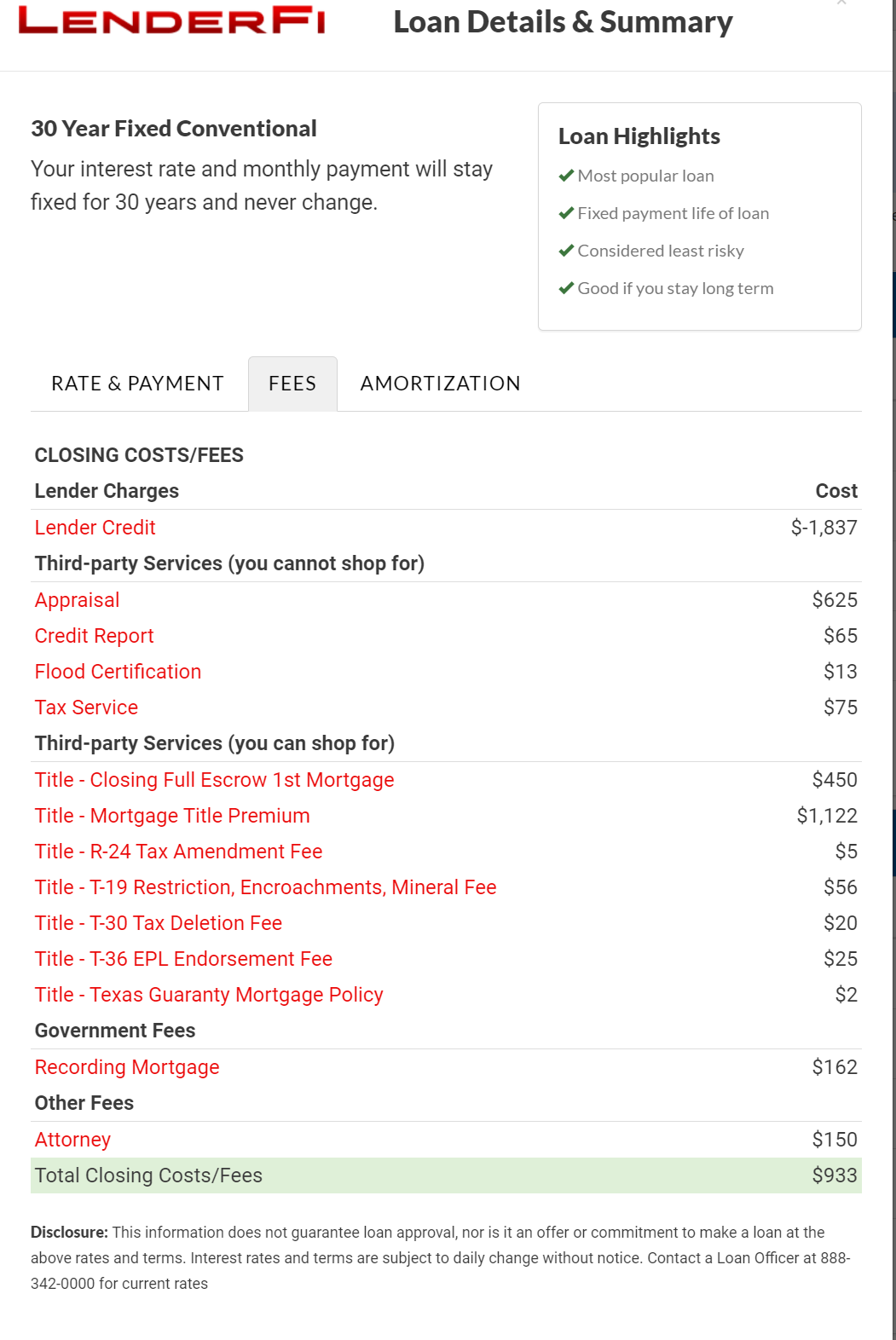

After some negotiating on the phone, Lenderfi is giving me 1.99% on a 15 with about $100 in closing costs. He ate the escrow waiver fee which was a nice bonus. I was thinking of going down to 1.875 with slightly higher costs but that loan wasn’t as “profitable” for him so he wasn’t willing to go that low and waive impounds.

I dawdled and didn’t refi in Dec/Jan, and rates came all the way back up to where they were 5 years ago when I last refi’d. Also have been noticing them creep back down.

I could refi to 3.375% 30yr and shave off .375% now.

Again I am amazed at Lenderfi’s process. Applied late afternoon on Thursday, April 22. Was asked for an ID, insurance declarations, and latest mortgage statement on Friday, April 23. Signed the tax transcript request at that time as well.

We’ve been underwritten, closing disclosure issued, and cleared to close today, Tuesday April 27. I didn’t need to provide bank statements, W2s, or any of that. I have absolutely no idea how they do this so quickly, with so little uploading of any financial data. At 1.99 I doubt we will ever refi again, but geez, this is less painful than going grocery shopping with the wife.

I got an appraisal waiver, yes. I dickered a bit over the phone with Ryan (the owner) who waived escrow without a quarter point charge.

Pricing for junk fees and things like escrow and title was identical to the quote on the website, aside from a $75 verification fee to Ellie Mae. That was disclosed in the initial loan estimate.

That rate sounds really nice. Is your loan rate only 1.99% or did I miss something along the way?

I haven’t had a loan in many years, but that is almost money in your pocket.

Yup Patty, it’s the rate. Mortgages are unbelievably cheap nowadays.

My parents are cut from the “debt is bad” cloth, and as they say, the apple doesn’t fall far from the tree, but it’s hard to argue that 1.99% on a 360k in a rising real estate market isn’t an example of good debt.

How do I get a lender (lenderfi or anyone else) down to the rate you see quoted here:

Specifically the 15 year fixed rate to 2.25% without upfront costs. I have no problem negotiating over the phone, but what do I need to do or say to get them to that? I have excellent credit (over 800) and I’m looking for a $110,000 refi on a house worth more than twice that.

Ask for things that other lenders offer. In my case, I asked for a free escrow waiver and used that as leverage. If you have a loan estimate from someone else, that helps too. If the Bogleheads thread is to be believed, LenderFi, Better, and Loan Depot are the three lenders that seem most deal-happy on the phone.

But, in your case, $110k is the hurdle. It’s a low amount relative to what you could take out, and so their ability to move the needle on deals is smaller as their margin is smaller (these correspondents and brokers earn a percentage back of the loan amount). Our principal balance is 359k on a house worth at least 900k in the crazy Seattle market. Lenders lick their chops at that because it’s a low LTV and it’s in the upper half of Fannie’s conventional loan limits.

I wouldn’t write it off completely. I can’t see your estimates from that link above, but if you see something you like there (e.g. a no cost loan that cuts your rate), why not go for it?

You might not be able to get as good a deal as some others, but if it’s better than what you currently have, it’s still worth it.

I’ll definitely be going for it. Anything right now will be an improvement, but I’ve just been putting it off. Your post reminded me that I shouldn’t. It’s not that difficult a process and I need to just do it.