I’ve written about the right of set off before , and why I prefer to keep my larger deposit accounts at different banks than my credit card and loan accounts .

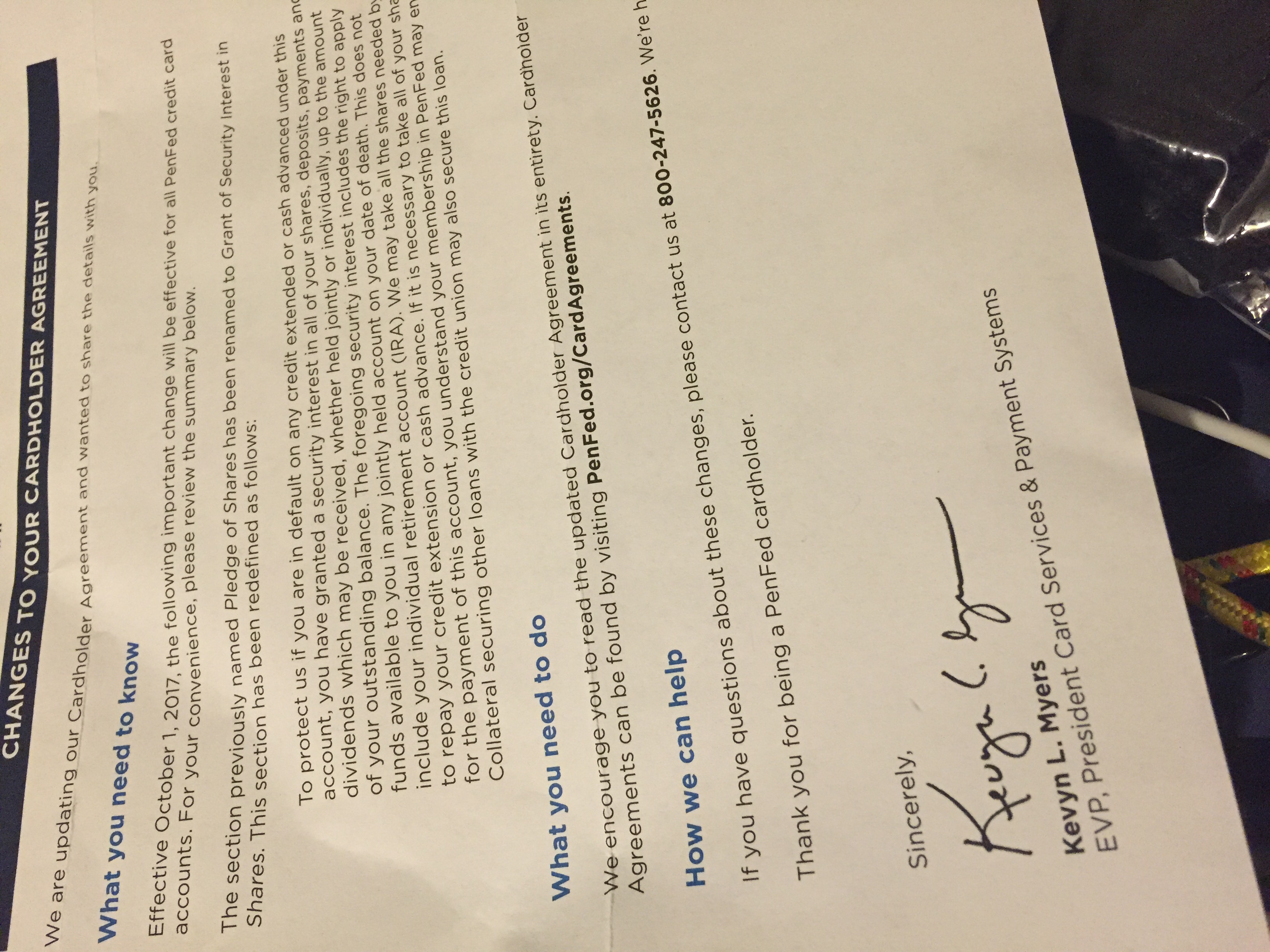

Well penfed just sent this letter making it even Clearer thst your penfed CC isn’t really an unsecured card. It’s a secured card and they can take any deposits you have with them if you default - even if you are a joint account holder, they can take funds from a joint account .

Now maybe you’re thinking "ok I’m not a deadbeat I’m not going to default " - well they also make it clear that If you die, and you have a joint account , say with your husband or wife , they will help themselves to the balance in your deposit accounts to pay off your cc , without asking and without going through the probate process . Funds your spouse might desperately need when you die .

Just a heads up - not all lenders and cc issuers do this , but many do .

Not Ron Jeremy - oops ! My bad ! Just got my letter today from penfed and wanted to post it

Well I guess this thread can be specifically about penfed so readers see the specific warning in the title , and we can use tripleB post to talk about the strategy in general not to keep large deposit accounts at the same banks where your credit accounts are located

Dave I absolutely agree with you about accurate and descriptive titles , and you nailed exactly what I was trying to convey . Thanks !

Dang it just feels good posting back and forth like this again !

@slappycakes - I agree with your post but I’ll keep my card open and in use for the CB at the pump. I also prefer physical statements to make my payments, but why does it take 10 min/mo to manage? I can billpay in less than 1 min per mo per card.

I got my letter in the mail today as well. Fortunately I don’t keep any funds at PENFED, otherwise I’d move them elsewhere.

[quote=“SIS, post:4, topic:693”]

Dave I absolutely agree with you about accurate and descriptive titles , and you nailed exactly what I was trying to convey . Thanks !

Dang it just feels good posting back and forth like this again ![/quote]

I completely agree. Feels like FWF circa 2000-2006.

Thanks for the warning about joint accounts in the event of death. I am not planning on defaulting or dying any time soon, but there’s a free option to have your CC debt die with you and it would be a shame to waste it.

I’m not with PenFed, so I have no stake in this, but what state laws apply here?

Are you allowed to title deposit accounts as Tenancy by the Entirety there? If so, that would protect the surviving spouse from this.

Otherwise, what would stop the surviving spouse from opening an account elsewhere, depositing the funds from PenFed into the new account, and calling it a day?

the living account holder can do whatever they like with funds in a joint account , but usually when someone dies , the first thing on the grieving persons mind isn’t “I need to rush to withdraw funds from the joint penfed account” as they have other things to take care of

I’m not sure what account titles penfed allows, I’ve only had individual , joint or POD accounts, and with the latter two your funds are at risk of being used to satisfy any penfed loans

Most financing Institutions subscribe to a list of all deceased SSN , and also credit report triggers when someone is noted as deceased , so while they won’t know instantly , they will find out even if you don’t tell them

I’m very surprised that this is not more widely known. I think almost every CU I’ve been a member of has language like this for their unsecured products.

Part of taking care of things is applying for any benefits due the surviving spouse and getting funds into their name alone. In my experiences helping settle affairs with family, these things can take place quickly.

Financial institutions can be slow to move to recover debt, if they even try at all. A family member took out a second mortgage with the bank that had his checking and savings accounts. He died, still owing a large balance on the mortgage. The bank had every right to seize all the funds in his accounts. The money wound up going to the state as unclaimed funds where they were subsequently recovered. This didn’t make sense, but it happened.

Agree that they will find out, but sometimes they don’t take the expected action.

The pen fed terms also say that they can use any collateral , so it’s not just deposit accounts . So If you have a penfed car loan or a penfed mortgage, they can use your home or car as collateral for your penfed credit card

You can set it up to automatically pay the statement balance each month. I have the 5% cash rewards (no points) and it is worth it for me to carry a separate credit card only for gas purchases

Did they ever 1099 him for cancellation of debt income ? Most banks will 1099 an uncollected account after several years , and once they cancel the debt they can’t go back and collect it

)

) Feels like FWF circa 2000-2006.

Feels like FWF circa 2000-2006.