and paste where it says “enter article URL”. Next delete the leading “F”, click on “create outline”, and the piece will appear.

Here is a lift from this WSJ article:

“About a fifth of American adults with FICO credit scores have an 800 or more, according to Fair Isaac Corp. , which developed them. It turns out there are few benefits for scores past the high 700s, a range that generally rewards borrowers with lower interest rates and higher credit limits.”

Not being myself within that elite group, I tip my cap to those who are and surely would like to know how you all manage it.

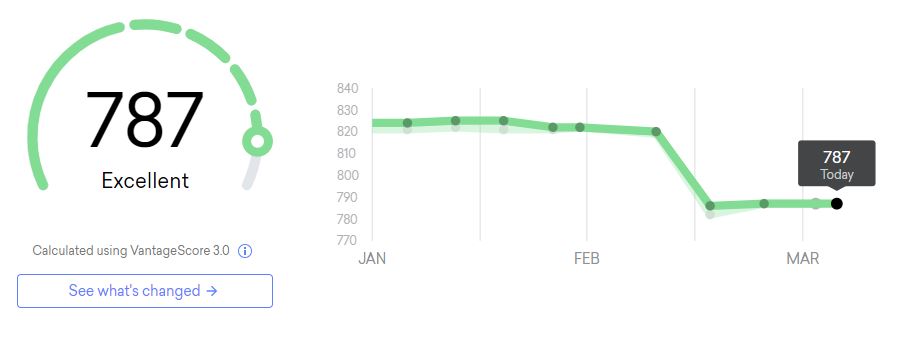

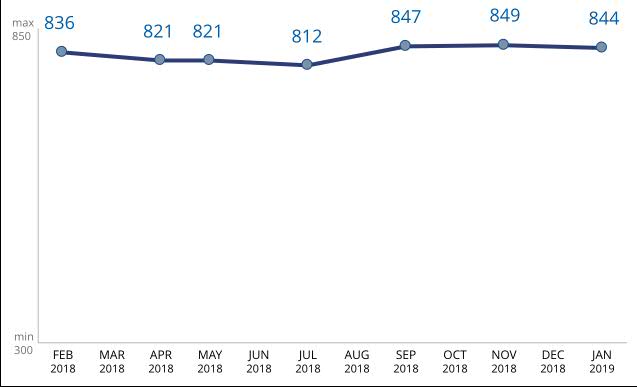

My credit score has remained above 800 for as long as I can remember, but I just took a very temporary hit as you can see below (this is Vantage 3.0). The reason for the precipitous drop is because I made an estimated tax payment in January that took ONE of my numerous credit card accounts to 60% utilization. This drop occurred even though my total credit utilization remained well under 1%! Of course this will right itself as soon as this card reports at the end of the cycle, but it shows how fickle the score can be.

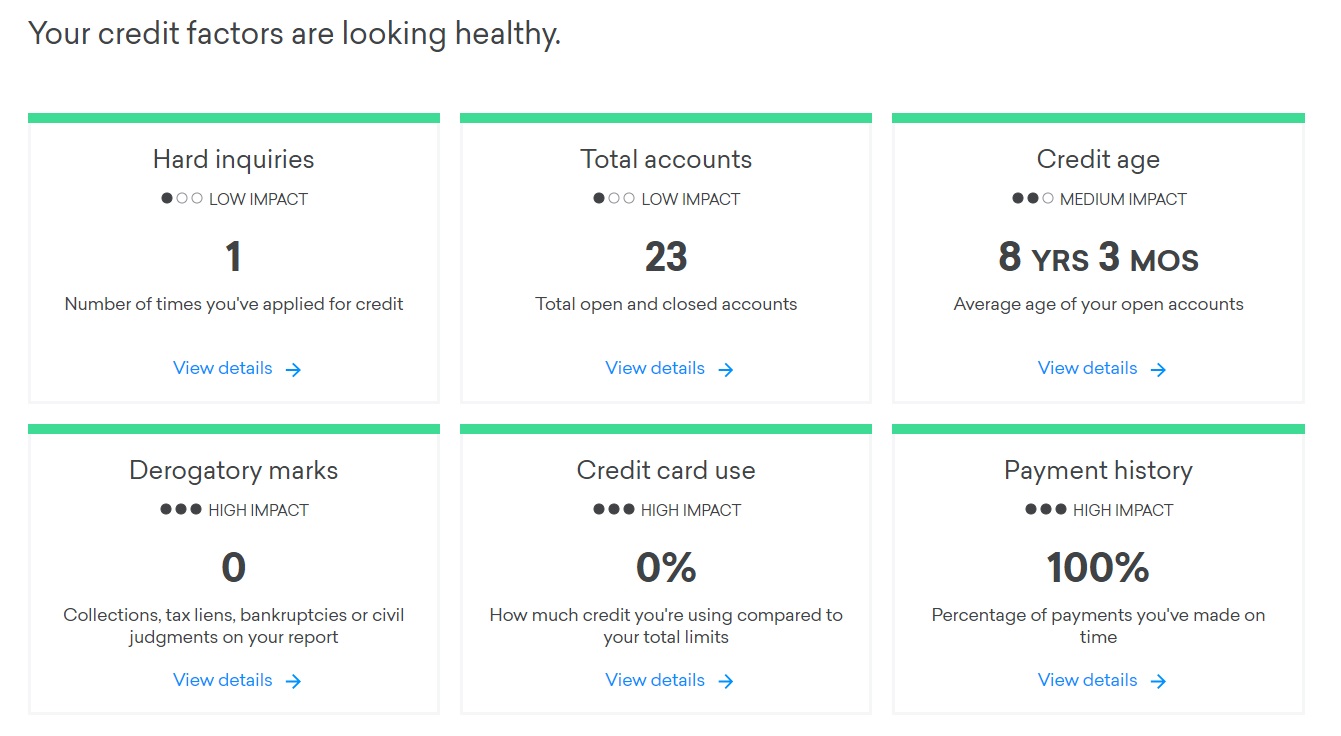

Am I concerned about the difference between 822 and 787? Not at all. There’s scarcely any difference. But keep in mind the score itself is just one factor in the credit card churning game. They are looking at specifics such as AAoA (average age of accounts), number of hard inquiries, and number of new credit cards opened recently. These things can get you denied despite having a stellar score.

I have had a score over 800 since I retired. Every time I take out an unsecured personal loan for home improvement it goes down. When I pay it back it goes up.

You have excellent credit, Steven.

can’t get it to show here, it is 830. I used the credit agency mailing list drop from credit card request offers and receive almost no new credit card offers.

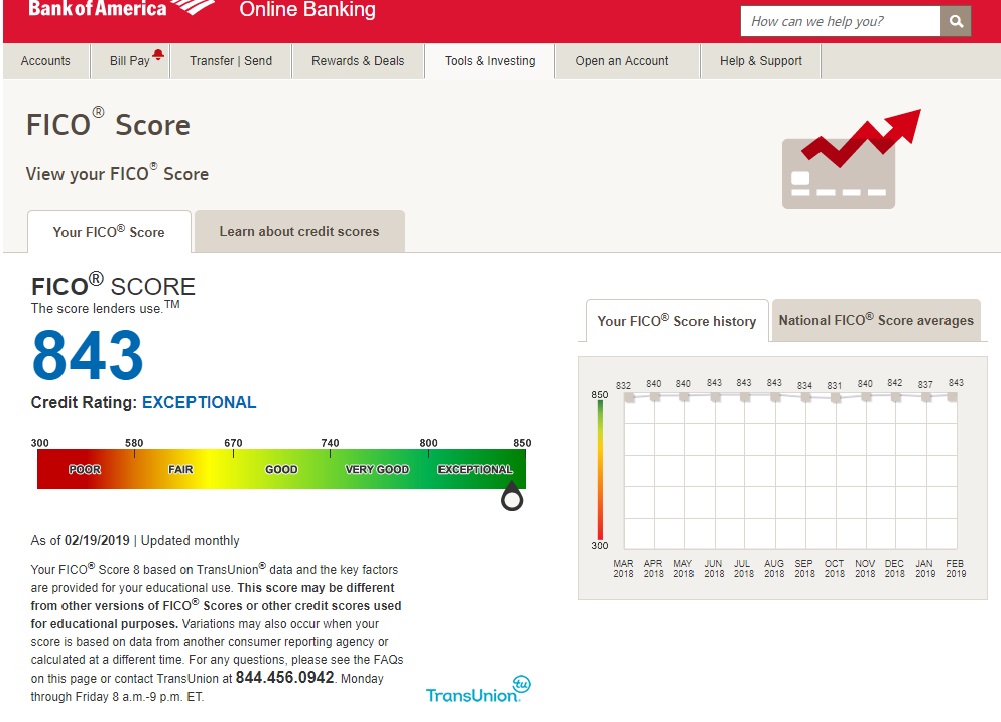

12 years ago, as a fanatical follower of FatWallet Finance, I drank the Kool-Aid® and learned how to conduct an AOR (App-O-Rama), applying online for multiple credit cards at a time. My goal was to use banks’ 0% APR balance transfer offers and stick proceeds into high-yield savings accounts to earn $$$. I did ok, but the long-term benefit was that I got on the road to high credit lines. (I did have a score of 843 about 18 months ago, so that was nice to see, but no big deal.)

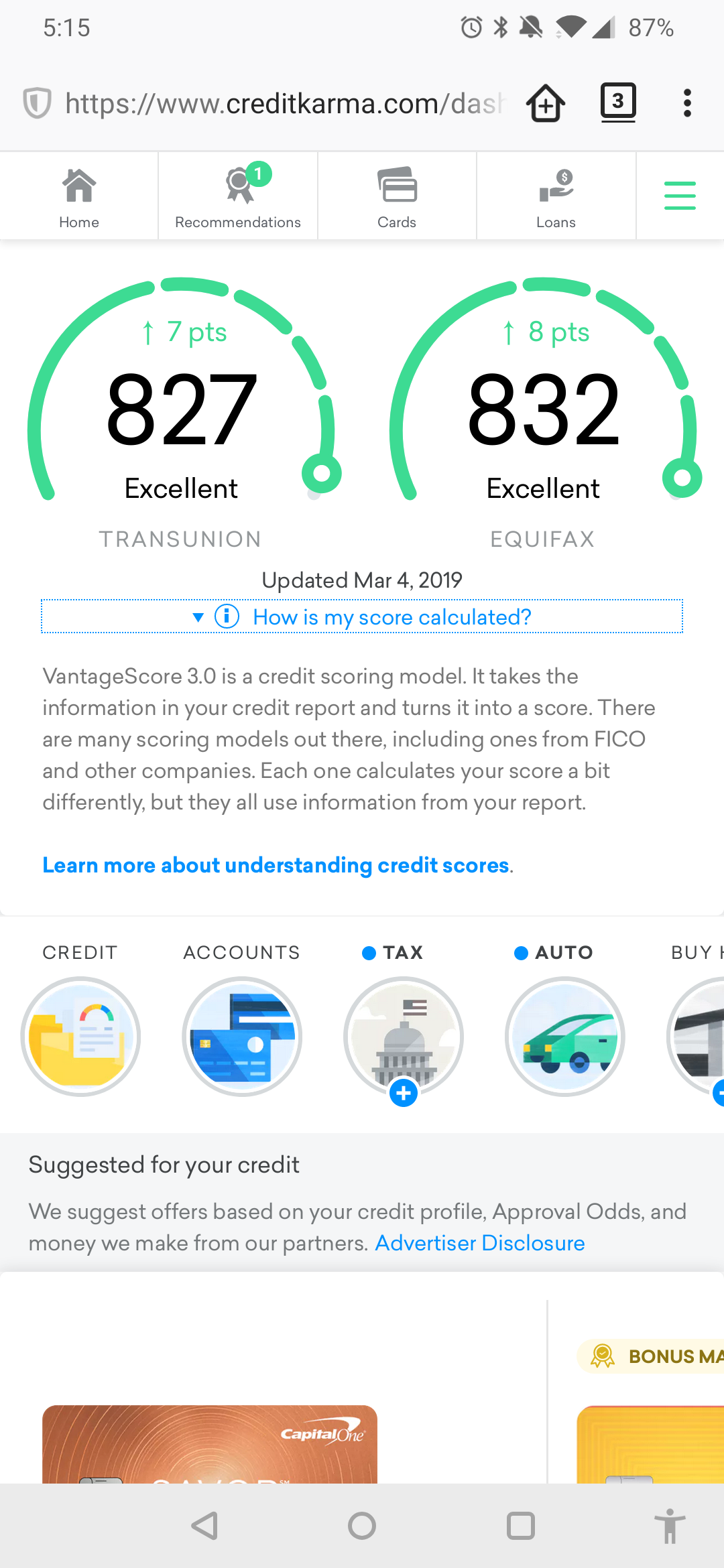

I was in my 50s when I did It is a bit of a silly game, of course, but to be under 30 with a high credit score must be a big rush. I’ll try to attach a screenshot of my CreditKarma report yesterday.

It’s not that difficult, and I’m surprised that a guru like yourself doesn’t know how to get there. There was a thread on FWF by @DaveHanson about getting and keeping high scores. I think minimum requirements for the perfect 850 is at least 8 years of history (oldest account of at least 8 years) and average account age of at least 7 years, plus the obvious: no negatives like late payments, bankruptcies, etc, and close to $0 balance on revolving accounts. The less obvious is zero hard inquiries and recent accounts. So churners could never get a perfect score without taking a 2-yr break from the hobby (well, maybe 1-yr, I don’t know).

With everything else being perfect, balances on revolving accounts (not student loans or mortgages) make the biggest difference. A few grand on one or a few credit card statements (depending on utilization) can make a difference of 50 points as StatGren shows (his shows ~30, but I’ve seen ~50 on mine).

Also the article has a few pieces of information that could lead the reader to incorrect conclusions:

There’s no need to pay the credit card every week, like some people mentioned in the article were doing. Once a month before the statement closes is enough.

Higher credit lines do not automatically produce higher credit scores by themselves. It’s all about utilization.

I also don’t see anything related to the second part of the article’s title, namely “Staying in Is Tougher”. It doesn’t talk about why it’s tough to get in (only that income doesn’t matter) or why it’s tougher to stay…

It’s nice to know that I won’t get denied for a credit card if I’m going for a bonus, but since I refuse to take out a car loan and I already have a mortgage, my high score doesn’t really benefit me that much. I don’t think I’ve ever seen it this high before. It was over 750 in my mid 20s and I think it hit 800 around the time I was 30 and I think it has been hovering there ever since. It might have jumped up this year since I’ve been putting all my spending on a business card for the past 2 months. I think my normal utilization is around 3-5%.

When I was in my early 30s, I checked my credit score and it couldn’t generate one because I had no credit history. I started with a $500 secured card. Shortly thereafter, I found Fatwallet and now I have well into 6 figures in credit lines.

As my credit score started to increase, I read that I would probably need a loan on my credit report in order to get over 800, but that’s not the case. My scores are all between 811-825, without ever having any kind of loan.

FICO’s criteria is reportedly:

35% credit history

30% utilization percentage

15% credit age

10% account mix

10% credit inquiries

You don’t need any one single factor to get over 800. Nobody knows for sure, but I suspect that the “10% account mix” requires two types of accounts for the full 10%: revolving (credit card) and installment (loan). But 10% is only 55 points ((850-300)*.1), so you probably get half the points just with one credit card. Maybe you could never exceed 825 because you don’t have any loans on your report?

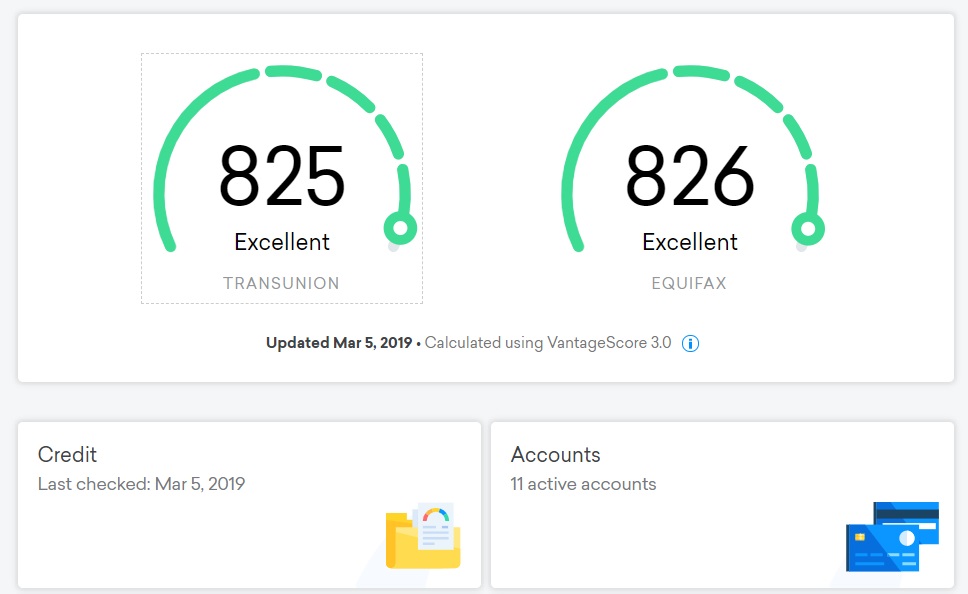

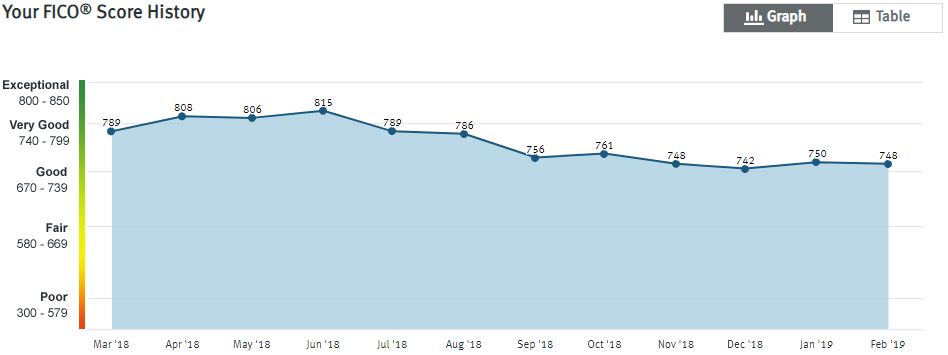

This topic got me curious, I honestly haven’t looked at my score since I was buying a new house about 18 months ago. Like others mentioned, once you get to a certain point, the actual score becomes somewhat immaterial. Looks like I almost hit the max a few months ago…

Interestingly, the of the two factors listed, the 2nd one I hadn’t seen reported before.

Proportion of balances to crdt limits is too high on bank revolving accts

Good point. I was using mine regularly for sign up bonuses to travel with until my wife got pregnant 3 years ago. Ever since, it does nothing for me. I guess I should be doing the smaller cash bonuses now that travelling is so difficult. I won’t need a good rate on anything anytime soon, so it doesn’t matter if my score drops. Plus I have plenty of cushion. I guess my only concern should be Chase’s 5/24 rule.

Agreed. Smart post. Not that I ever had an 850 score. I never had that. But I used to be up above 800.

Then I sort of got the same thought you posted and I decided to monetize my score with a modest side hustle. It was in process of implementing that monetization that my score descended into the high 700’s, where it regrettably has remained. So I no longer have a sweet credit score. But I do have more money. That said:

Either within a couple of months, or within a year plus a couple of months, I have hope my score will recover some of its former lustre. I opened a bunch of credit cards last spring too fast for the preferences of the FICO gods, falling thereby into disfavor. But I’ve been a good boy more recently, to the point I hope where eventually their forgiving nature will assert itself. Until then all I can do is admire and envy the credit scores of other posters here.

My wife’s credit score averages 20 points higher than mine most months. We have very similar profiles. This has led me to the firm, scientific conclusion that the FICO AI robot is female.

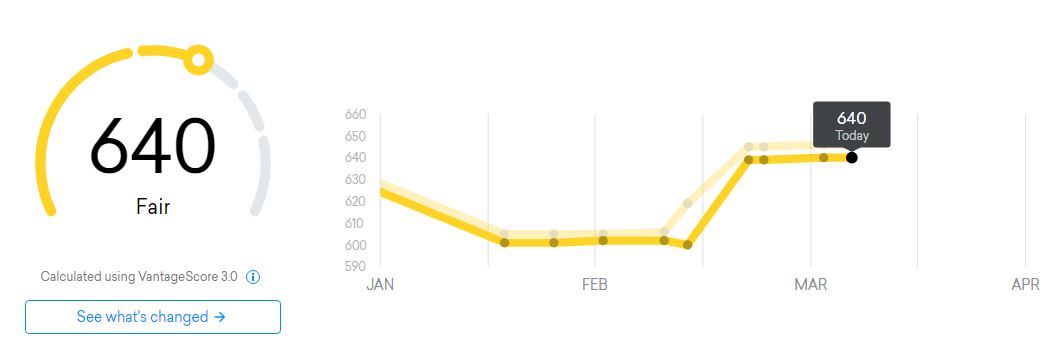

I used to be above 800 too until I started to write some balance transfer checks for low interest money. Now my FAKO is around 640 (“needs improvement”) but my FICO is still in the mid 700’s, despite four cards with over 80% utilization.