There is actually stuff in ACA about trying to improve healthcare outcomes. There were whole chunks (mostly ignored) on quality and health system performance, wellness, prevention. thats all targeted at outcomes and overall healthcare system improvements.

Its been a while but last time I gave a homeless person food they were pretty thankful.

How often have you done it and what were your results?

2 Likes

I hate to burst your bubble, the rising suicides, prescription drug overdoses, and rising alcoholic liver disease preceded the ACA.

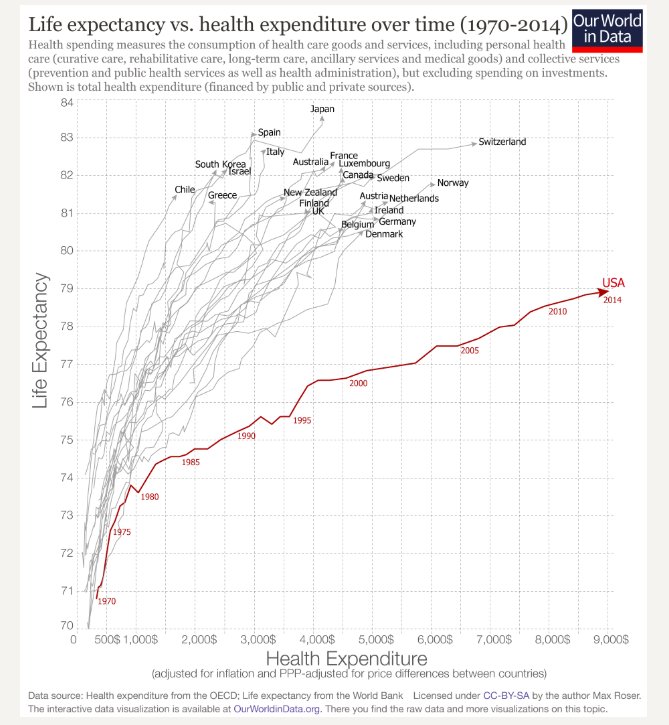

Yep. I wanted to mention yesterday that the ACA wasn’t just about additional coverage (or “political”), but about higher quality and efficiencies and prevention and bending the national healthcare cost curve downward, but I didn’t have the time.

Um no.

CA and OR are among the lowest death rates for drug overdoses and both are super blue gung ho on medicaid.

TX, CA, OR, MS, ND all have similarly low death rates and are all across the political spectrum and a mix of medicaid expansion and not.

Mixed results. The truly homeless accept food. The New Orleans / SF hippie traveler kids just want money for weed. I think the “they’ll just spend it in drugs” mentality hurts the homeless more than it helps. They’re not all on drugs.

Having said that, I give so little that I’m hardly an authority on it, and this is kind of off topic anyway.

1 Like

Perhaps you misread the statistics I posted - not that Medicaid states have higher OD rates, which is variable as you say. Rather, the rate of increase in OD rates has been higher / faster in Medicaid states than non-Medicaid ones, which is a fact during the ACA period and it’s just of question to what cause you want to attribute that effect.

Yes, the ACA had lots of new rules and regulations. since then, costs are up, premiums are up, and mortality rates are up. Maybe we should have agreed three years ago on the criteria for “success” so we don’t end up in one of those “if only we had taxed and spent 3x as much, it might have worked” arguments after the fact.

You’re right, that you were talking about rate of increase and I quoted the death rates.

But its not at all proven that medicaid expansion has anything to do with a higher rate of increase.

Look at your source (some random guys blog) and what they fail to say about California and Oregon and examine the graphic map showing the rate of increase by state.

OR and CA and WA all have lower increase rates. 15% of the US population.

All 3 are gung ho medicaid expansion. Oregon was expanding medicaid 20 years before ACA.

Inflation-adjusted national healthcare costs are DOWN, premiums are DOWN relative to where they would have been if they had kept increasing at the double-digit rates present prior to the ACA (and adjusting for real comprehensive coverage instead of fake coverage), and mortality rates started up prior to the ACA.

Otherwise…

1 Like

It’s getting to be the time of year where insurers will submit their 2019 rates, and ballparks are looking like +30% and fewer choices, but it’s a bit soon to say for sure. Here’s some coverage on the topic:

There are four major factors driving the trend towards higher Obamacare premiums for next year:

-

2019 will be the first year with no penalty going without insurance. Healthier individuals will want to consider this option, especially in the light of rising prices. Some states are individually talking about state level penalties, but those are likely to be very unpopular and seem unlikely to be actually passed.

-

No insurance company bailout. insurance companies had been lobbying for a large national reinsurance pool to be added to the omnibus budget bill, but in the end that was unsuccessful. This would have injected additional taxpayer money to subsidize ongoing losses on Obamacare plans, which would allow them to be priced more cheaply than otherwise.

-

No CSR funding. As was the case for 2018, these subsidies are not being paid by the federal government, nor was a compromise reached to reinstate them earlier this year or in the budget (Democrats seem to have decided the impact of higher Silver plan prices was net good for their constituents via higher premium credits/subsides, so they didn’t care about this issue), so the costs are passed on to the individual. Obviously this matters a lot more if you aren’t getting a premium subsidy, but it may depend on how your state decided to allocate these costs across the ACA marketplace.

-

Push towards offering more short-term, non-ACA alternatives. The Trump administration has favored offering more flexible short term and ACA-exempt policies. This is in contrast to the additional restrictions the Obama administration implemented towards the end of their time to try to remove these as practical alternatives for healthier individuals. As such, combined with the lack of individual mandate, this change will allow healthier individuals to seek insurance elsewhere, leaving higher costs and higher uncertainty about the risk pool that remains covered via the ACA exchanges.

In short, all factors point towards yet another year of double digit increases in unsubsidized premiums. While a few individual states are considering their own mandates to require insurance or their own toxic reinsurance pools to subsidize their domestic ACA markets, it seems broadly unlikely that these proposed measures will be implemented due to their high cost, political unpopularity, and tight time frame for legistlative action.

1 Like

Along with all the pre-ACA horrors, like charging lots more for pre-existing conditions, allowing recessionary rip-offs, discriminatory pricing, and on and on.

As a nation, we’ve been there, done that.

2 Likes

But that’s what they want, because you know, open market fixes everything you can’t tell me what to do yada yada yada. Even when it’s proven that HC is about as non-open as you can get, and it’s perfectly ok to force peeps to buy auto insurance etc.

2 Likes

You may recall Centene was one of the few insurers making money selling Obamacare, using cut rate very limited plans that are funded primarily by taxpayer subsidies for the poor rather than the recipients.

Apparently selling insurance to the poor under Obamacare and other government funded programs like Medicaid, is such good business, that the NY governor decided he wanted a $2B cut of the action.

https://www.wsj.com/articles/cuomo-loots-a-catholic-charity-1523315215

Fidelis plans were nothing to write home about (very much in the “clinics for the poor” category fitting with Centene’s business), but I know a shakedown when I see one.

We’ll end up trying every system that doesn’t work first.

It makes no sense to me why the cash price is often a lot less than UCR (usual and customary). I think this is an artifact of virtually all plans having coinsurance now. It wasn’t so long ago that plans that paid 100% after a low-ish deductible were fairly common, and the out of pocket maximum wasn’t really an issue.

This seems, at a much lower scale than for surgeries, to be especially true for prescription drugs. Almost every drug I’ve purchased recently was significantly cheaper for cash than using my BlueCross negotiated rate. It would make you wonder if the insurers are getting rebates on it.

I thought this was all a side effect of how insurance is billed. My understanding is that it works out as follows (I’m paraphrasing roughly) :

Your typical doctor takes lots and lots of different insurance plans.

Those insurance plans effectively fix the rates and tell the doctor what they will be paid. So one plan might pay $150 for a visit, another $170 another $200 and medicare pays $100. (made up numbers for example sake).

The doctor has to cite a single rate to the customers so they pick the highest possible rate for insurances and they charge $225. If they picked a lower number like $150 they’d get less money because the plans that pay $170 and $200 would then just pay the $150. But if they cite $225 as the rate then the insurers each pay the rates listed above individually. So a patient with insurance that pays $150 gets the $225 bill then the insurer pays $150, but another patient with insurance that pays $200 gets the $225 bill and pays $200.

For cash only the doctor knows what they’ll actually get paid so they can easily just cite the $100 or the $150 and get what they expect and deem reasonable. Plus of course cash only patients have no insurance bureaucracy for the doctor office to deal with so its cheaper to take cash paying customers.

in short: doctors basically simply pick the highest possible payment rate and cite that to all insurance companies

Now I don’t know if the actual doctors are sitting down and figuring this out to “game it” or if its just “how the system works” and medical billing services for doctors do it or if its just common knowledge for doctors or what.

If theres a doctor here they can possibly shed light on it past my crude paraphrase of something I read once.

2 Likes

Maybe another way to look at it, I would always expect cash rates to be cheaper since the UCR includes the ~20% we pay to insurance companies for all the great things they do.

Yeah, but if that’s true, why would they seek to limit utilization of services at all by narrowing networks, requiring pre-authorization, etc? Although with unlimited utilization included, the premium would be so high that nobody would buy it, I guess.

We may see singnifant improvement in the short term policies offered as an alternative to Obamacare. Trump has asked HHS to expand “short term” insurance by relaxing the increasingly strict Obama-era rules, both by allowing 12 month policies as the ACA originally intended (rather than just 3 months currently, which was cut by Obama part way through to reduce the attractiveness of ACA alternatives), and by allowing a guaranteed renewal rider to allow the short term policies to extended into more useful multiyear guaranteed coverage.

https://www.wsj.com/articles/a-chance-to-overcome-obamacare-1527517284

The need for action is clear, as ObamaCare premiums keep skyrocketing. Rate hikes as high as 91% will hit many consumers just before Election Day. Maryland insurance commissioner Al Redmer warns ObamaCare is in “a death spiral.”

So-called short-term health plans, exempt from ObamaCare’s extensive regulations, are providing relief. Such plans often cost 70% less, offer a broader choice of providers, and free consumers to enroll anytime and purchase only the coverage they need.

HHS’s nonpartisan chief actuary estimates 12-month terms would provide year-round coverage for an average $342 a month, vs. $619 for ObamaCare plan…