Excessive deficits, money printing, unfunded liabilities, weakening rule of law, arbitrary and highly politicized economic decision making; these are all Emerging Markets traits.

The gilts market collapse should have been a wake-up for everyone, except most investors assumed it was just a UK thing. What if DM markets are now living with EM rules? What if the US is now an Emerging Market but we don’t realize it yet??

The Strategic Midterm Re-election Reserve is half empty, but Dear Leader is planning further dumping in the next weeks before November.

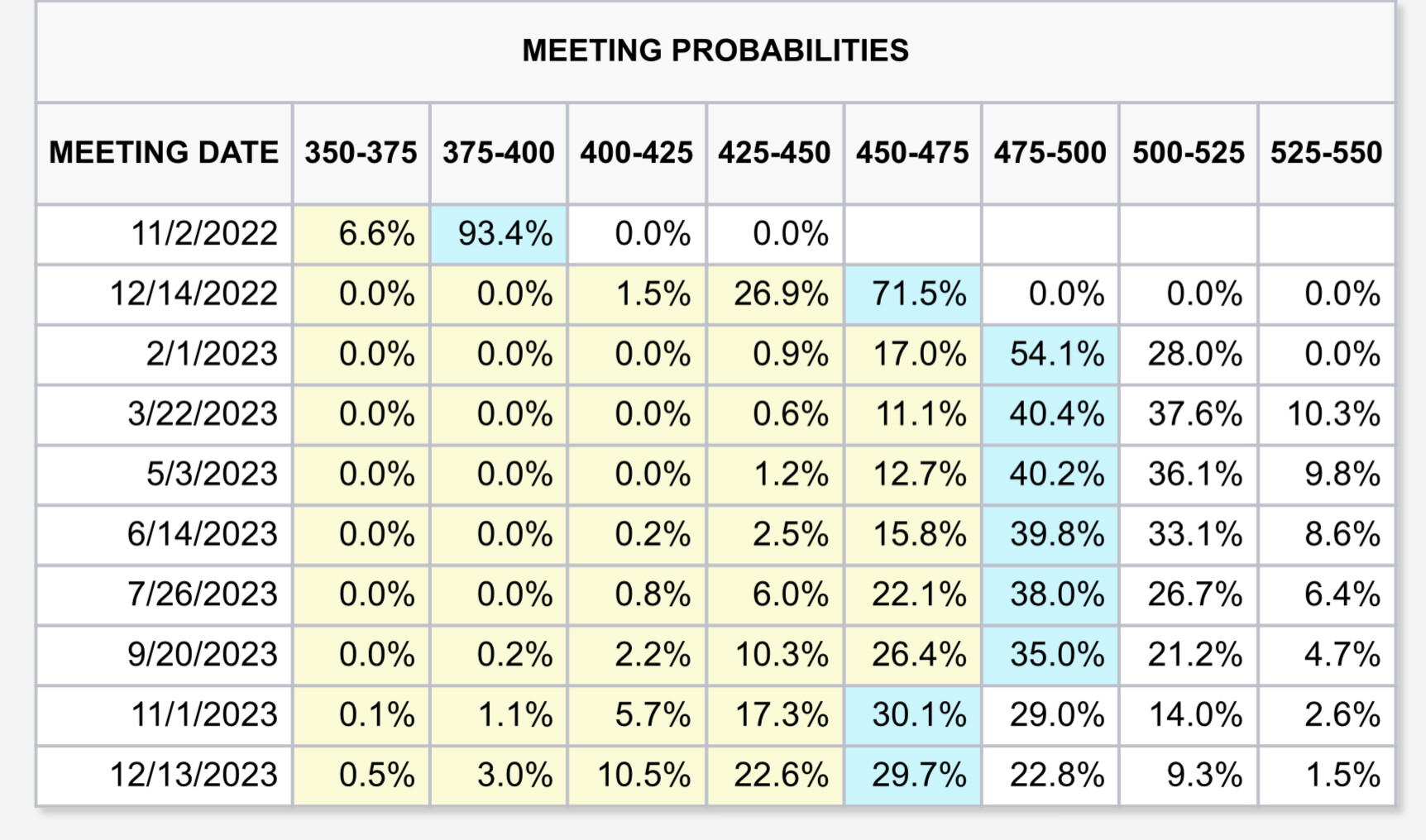

Meanwhile, the market is expecting a +75bp hike at the Nov Fed meeting, as well as another +75bp in Dec, with outside chances of a little less. At 3% now, that will put us at 4.5% before EOY.

The markets are anticipating that. I just bought a six month Tbill with a 4.398% yield. Edit. That is a 4.85% taxable equivalent yield for the 9.3% California income tax rate.

The taxable equivalent yield depends not only on your state income tax rate, but also on your federal income tax rate. The multiplier is (1-fed)/(1-fed-state). For example, with 24% federal and 9.3% state, the taxable equivalent yield is 0.04398*(1-0.24)/(1-0.24-0.093) = 0.05011 (=5.011%). If your state income tax could be itemized, the formula would be closer to (1-fed)/(1-fed-state*(1-fed)).

Edit. I should’ve been more precise and said that was the state taxable equivalent yield. After all, both CDs and Tbills have to pay federal income tax

I was assuming that because of the SALT limitation you do not get the benefit of deducting most of your California income tax. State property taxes are so high that they can easily use up all of the limitation. For example, the house across the street from mine recently sold for $1.75 million. Their property tax is easily $18,000 per year.

Edit. I do not live in an expensive town like Atherton. Just a middle-class neighborhood in the Silicon Valley burbs.

I think this is true for most people, but I can still envision a scenario where a single filer who bought their home a long time ago (or inherited) and cash-out refinanced could have enough mortgage interest or other items to exceed the standard deduction, and extremely low property tax (prop13), which leaves plenty of room for the state income tax within the SALT limit.

I agree it could happen. Everything in taxes is complex. But as a general rule in comparing interest on CDs and tBills, I adjust by my state marginal income tax rate.

On a related topic, as has been discussed here multiple times, if the interest rate on the national debt increases to a 5% fed funds rate, The interest expense to the treasury will be 5% of $31 trillion, or $1.55 trillion per year.

Yes, it has also been discussed here, like every time, that the entire $31 trillion worth of debt doesn’t rotate instantly – it takes time. So if the FED funds rate goes and stays at 5% for a few years, then yes, that’ll be the case. But if the rate comes back down, then the expense won’t be that high.

White House director on the hot seat over putting politics of oil / SPR ahead of American national security. Short video clip. Nice to see a media still willing to ask hard questions, and repeatedly when they aren’t answered.

“Today, my administration announced that this year, the deficits fell by $1.4 trillion,” Biden said, calling it, “the largest one year drop in American history.”

Compared to the massive covid stimulus, you managed to spend less? check, but your deficit was still (also) $1.4T, 50% higher than any pre-covid deficit ever. You can see them all here, 2019 was under $1T.

Biden Says GOP Plans Would Add to Deficit, Make Inflation Worse

You mean your Inflation Reduction Act isnt working, but someone else would be worse. Hard to see that, but maybe we need some turnover not just in the White House, but also in the Treasury and the Congress to get on a more sustainable path.

Except neither Republicans nor Democrats are capable of creating a “more sustainable path” for federal government spending. We need ranked-choice voting in all elections in all states to have any chance, and independent candidates who are actually fiscally responsible, not in-name-only.

Ranked-choice won’t do the trick either. That assumes the electorate as a whole, or the majority of the electorate will have the best interest of the country’s finances in mind. Reality is that people from both sides, i.e. the majority of voters, have no problem with the increasing debt as long as they benefit somehow.